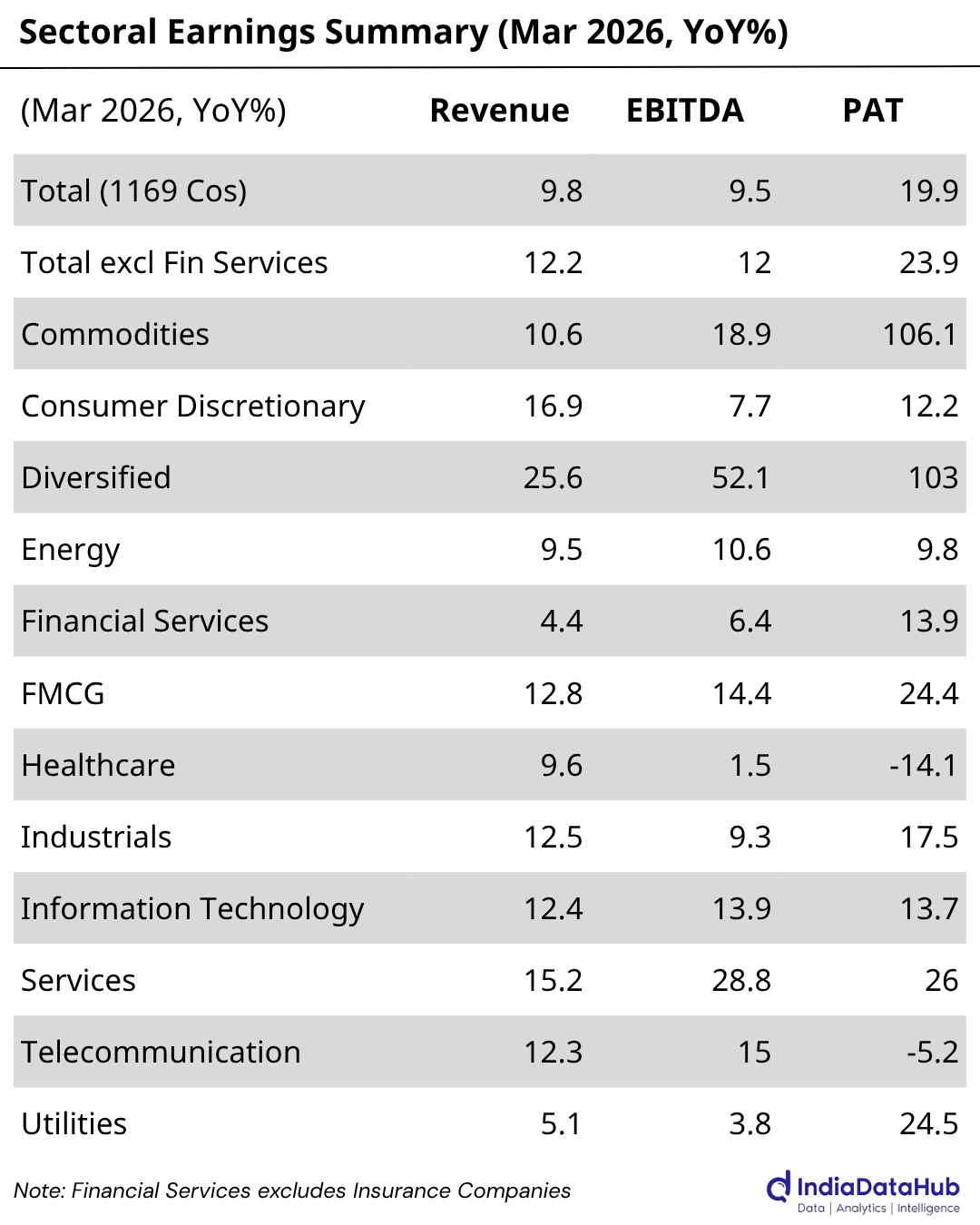

Welcome back to This Week in Earnings. The Q4 FY26 results season is well underway, with 1,169 companies reporting so far for the March 2026 quarter.

The aggregate picture shows a step-up in earnings momentum. Revenue is up ~10% YoY, EBITDA up ~9.5%, and profits have surged nearly 20%, a meaningful acceleration at the bottom line. Excluding financial services, the numbers are stronger still: revenue and EBITDA both up ~12%, with profits up nearly 24%.

This newsletter is structured into two sections:

The first section tracks aggregate and sectoral trends, highlighting what’s propelling growth this week.

The second dives into standout company results shaping those numbers.

Want to dig deeper? Download the extended edition for full sector-wise company data and detailed performance notes

.

This Week’s Summary

The headline PAT acceleration so far needs some unpacking. Across several sectors, reported profit growth is running well ahead of operating performance, shaped less by demand strength and more by exceptional items, base effects, deferred-tax credits, and provisioning relief. The gap between EBITDA and PAT, and what explains it, is where most of the interesting analysis is so far this quarter.

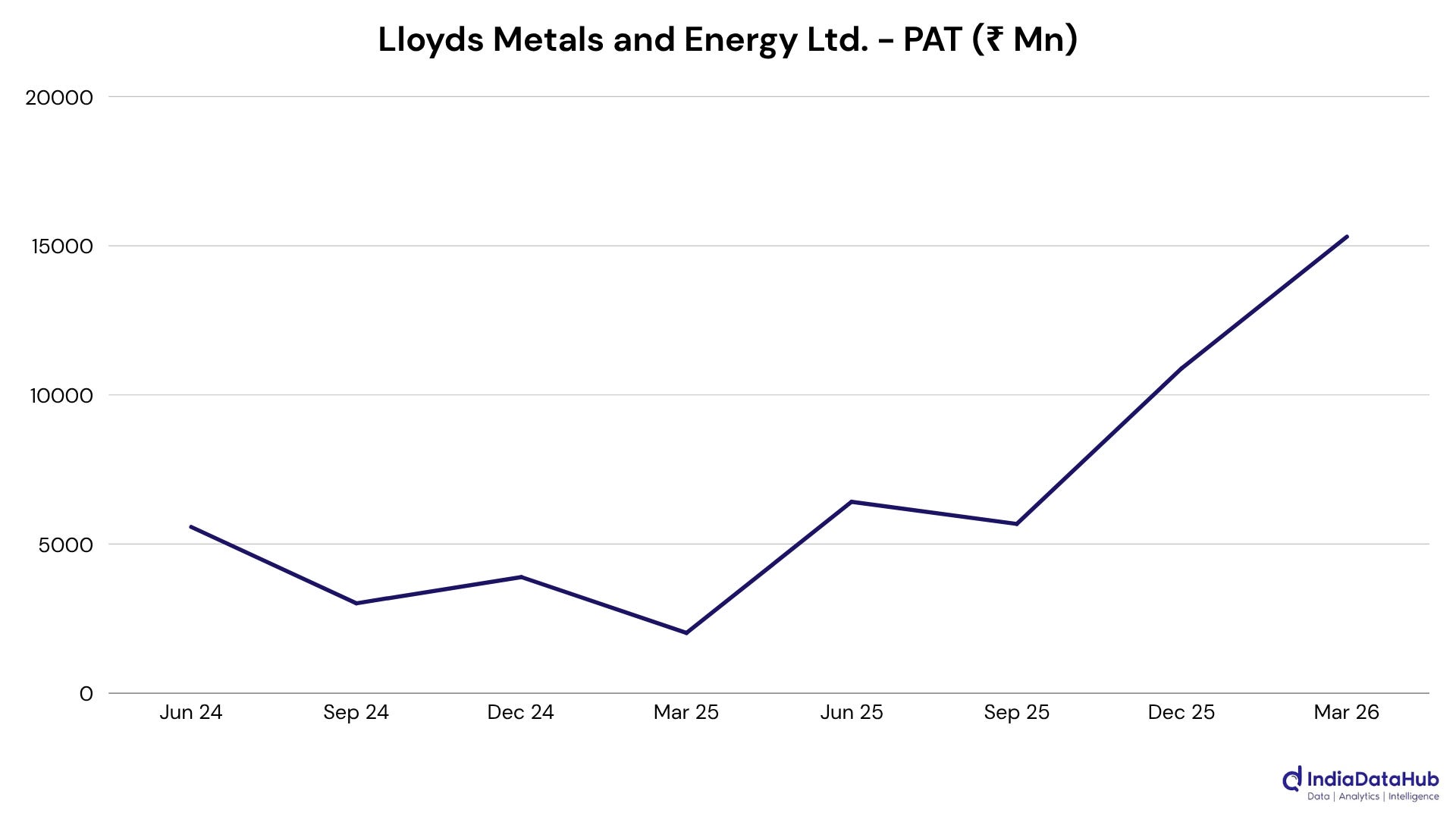

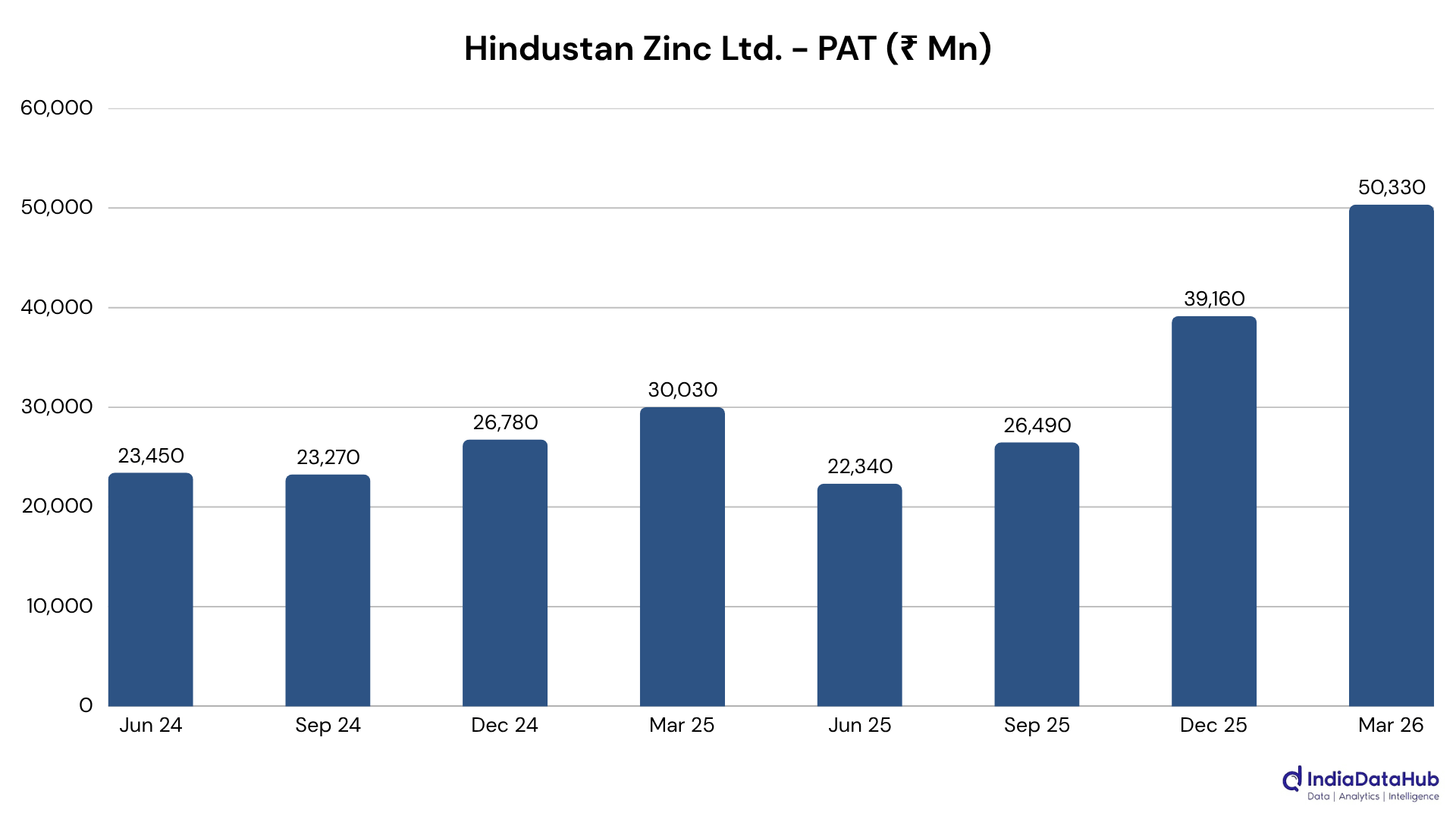

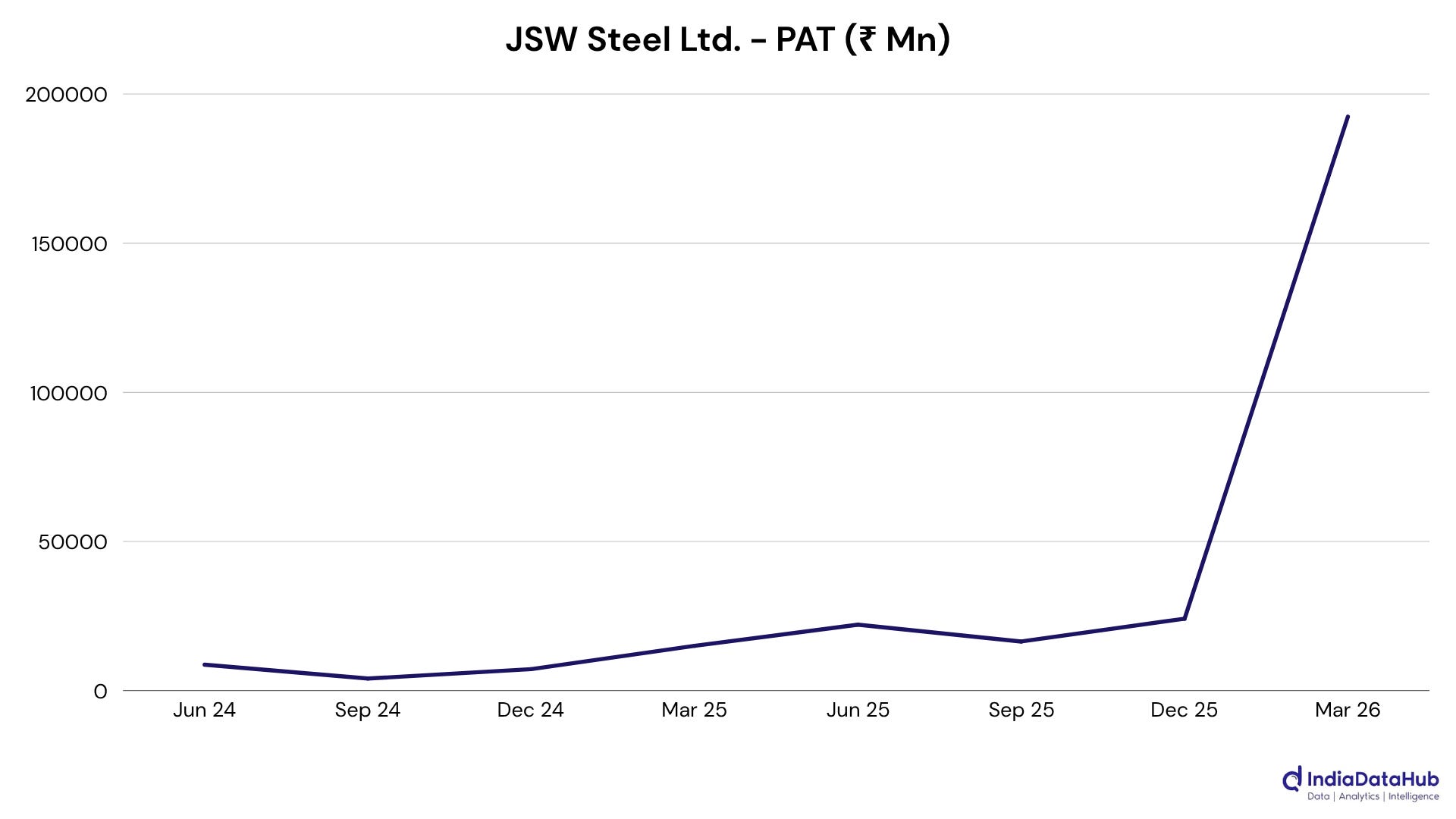

Commodities is the most dramatic illustration. Revenue grew a modest ~11%, but profits have more than doubled, making it the largest contributor to aggregate PAT outperformance. The story varies within the sector. Tata Steel and Jindal Steel both delivered operating recoveries through record domestic volumes, wider EBITDA per tonne, and lower finance costs. Hindustan Zinc posted one of the cleanest results of the quarter as zinc production costs fell to record lows on domestic coal and better ore grades, silver prices surged, and profit growth required no exceptional support. Lloyds Metals has a different kind of story, with less commodity upcycle and more structural shift, as LSIL consolidation and captive iron ore integration pushed margins into a new range. JSW Steel’s headline profit jump, meanwhile, carries an asterisk: a one-time BPSL exceptional gain flatters the PAT line, though the underlying steel business (record volumes, firmer domestic prices) was strong in its own right. Cement within the sector had more mixed results: UltraTech and ACC both reported record volumes, but ACC’s profits fell sharply as fuel and packaging costs outpaced realisations, while UltraTech delivered cleaner operating leverage.

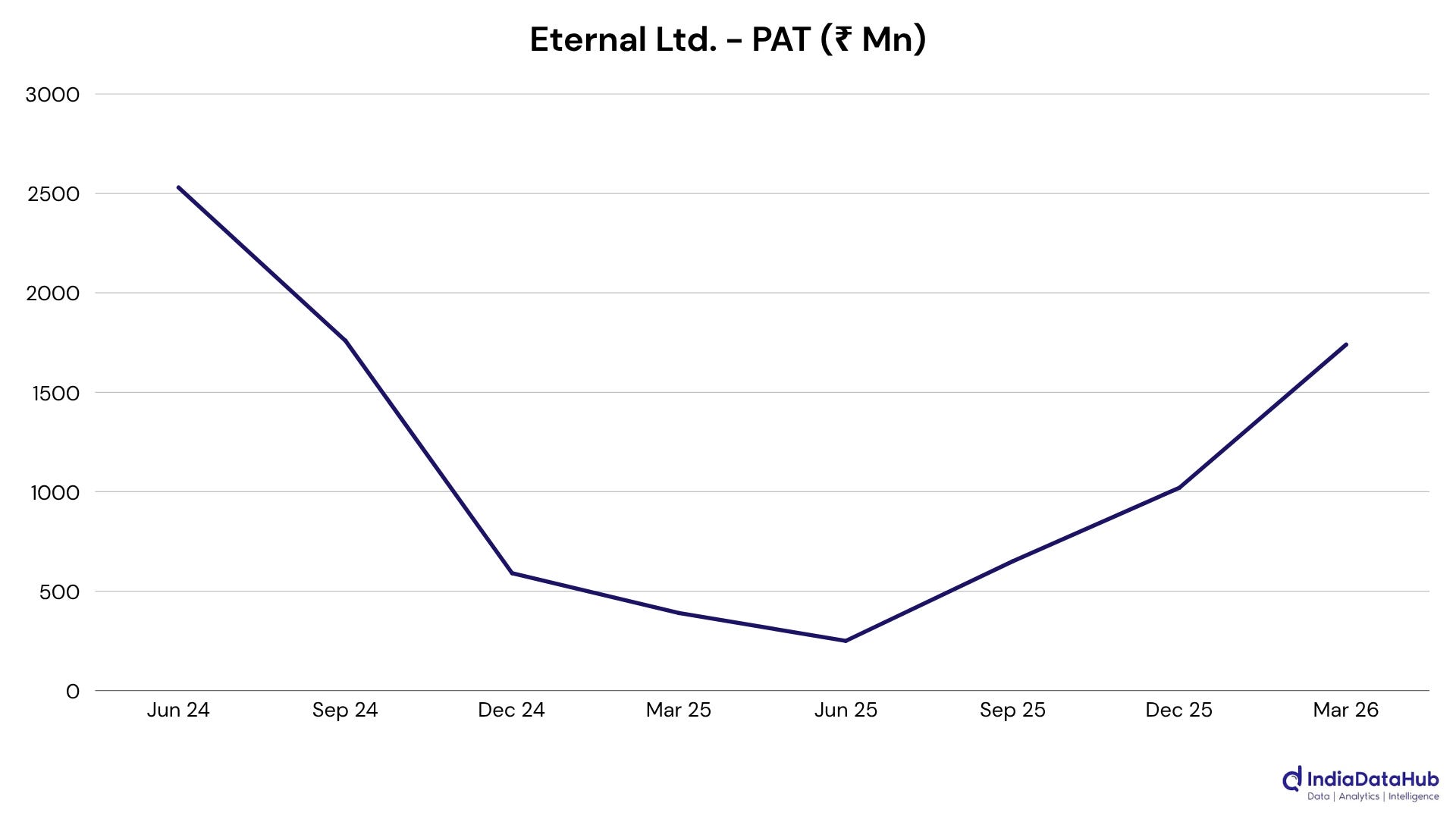

Consumer Discretionary presents a more nuanced picture than the sector-level numbers suggest. Revenue growth of ~17% looks healthy, but EBITDA growth of ~8% and PAT growth of ~12% point to meaningful margin pressure beneath the topline. Within that, the stories diverge. Mahindra & Mahindra delivered a clean quarter, with SUV, tractor, and EV volumes all strong and operating leverage flowing through to profit. Maruti and Hero MotoCorp both set records in revenue and operating profit, with PAT distorted by mark-to-market losses and tax items rather than by operational weakness. Titan’s revenue surged on high gold prices and Damas consolidation, but margin mix shifted as consumers gravitated toward lower-margin gold formats. At the other end, Tata Motors’ consolidated result was weighed down by JLR’s exposure to tariffs, China weakness, and cyberattack disruption, even as the India PV business held its ground.

FMCG is a strong sector so far this quarter, with revenue up ~13%, EBITDA up ~14%, and profits up ~24% and growth is broad-based across companies. Unlike some sectors where PAT growth reflects one-offs, FMCG’s bottom-line acceleration has operating content. Edible oil margin recovery at AWL, premiumisation at Radico Khaitan, commodity cost relief at Nestle and Varun Beverages, and HUL’s strongest volume growth in several quarters all point to a sector where demand and margin recovery are working in the same direction.

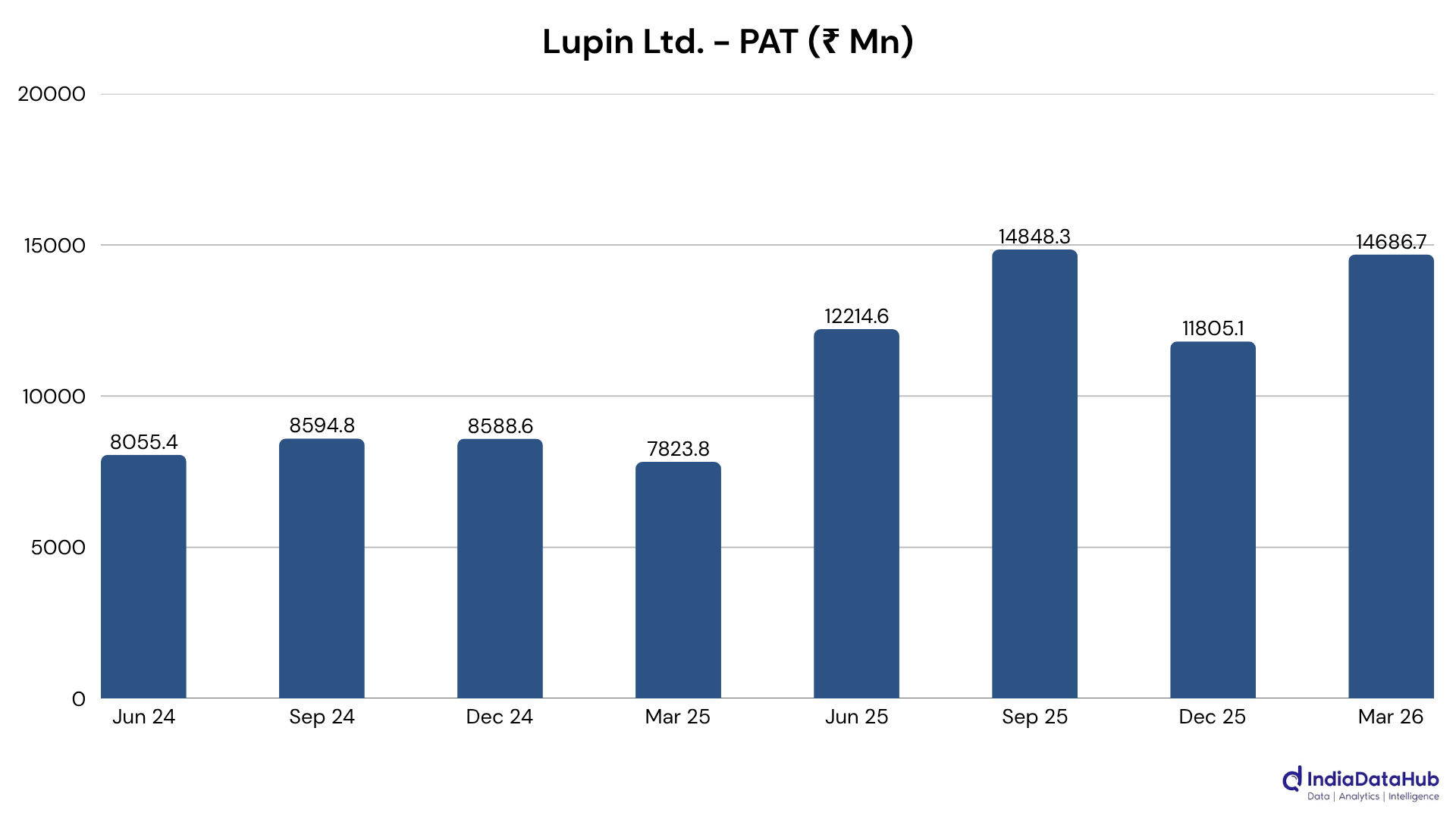

Healthcare has shown the sharpest reversal as of yet. Revenue grew ~10%, but profits fell 14%, a sector-level PAT decline that stands out amid an otherwise broadly positive aggregate. The explanation is concentrated. Cipla and Dr. Reddy’s both saw North America profits crater as lenalidomide sales normalised and shelf-stock adjustments hit earnings, making this less a structural story and more a US generics product-cycle reset. Lupin, by contrast, had one of its strongest quarters; its complex generics and new launches drove a sharp recovery in revenue and profits.

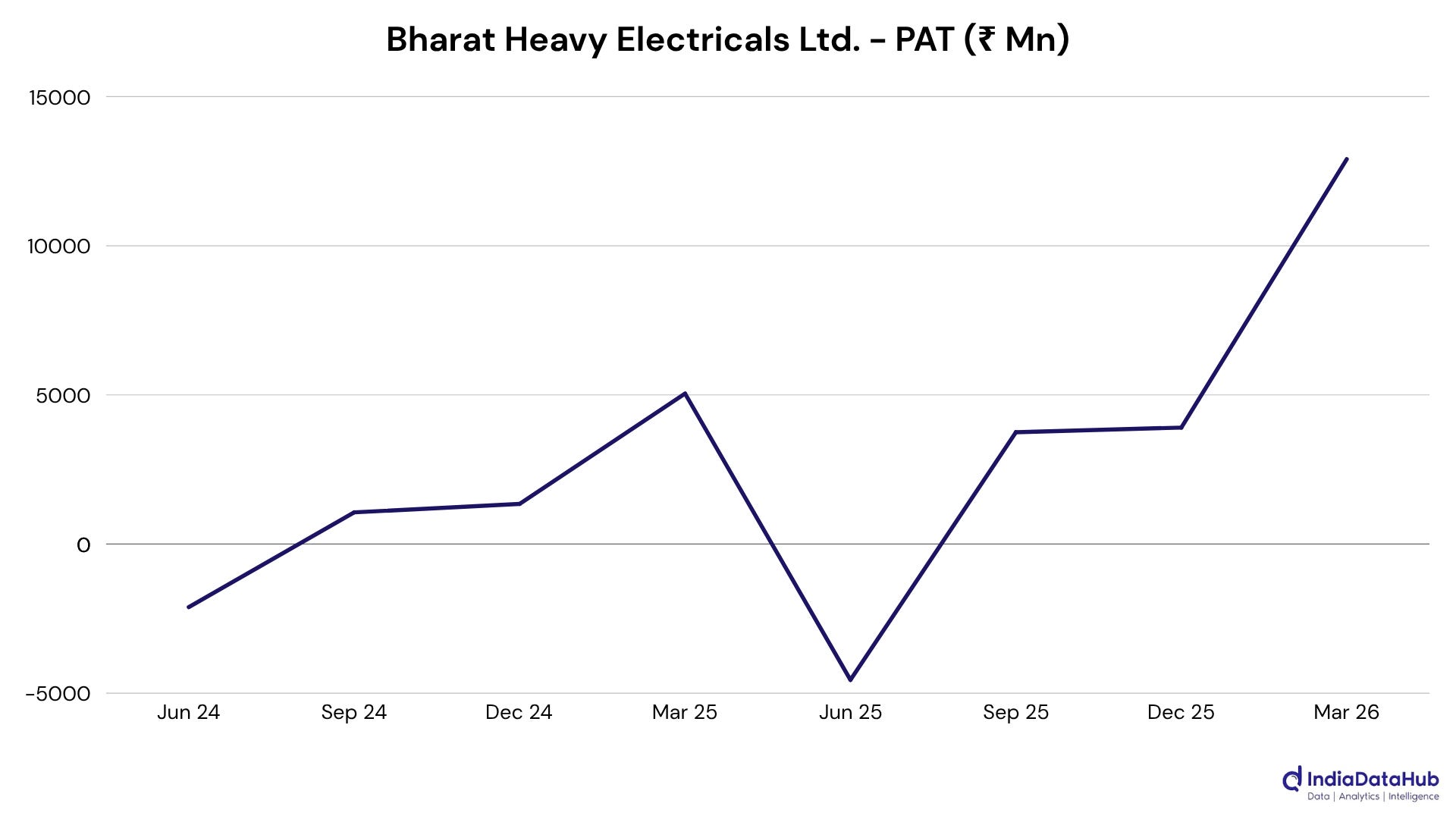

Industrials delivered solid but uneven results, with revenue up ~12.5% and profits up ~17.5%. Larsen & Toubro’s profit dipped because last year’s base included an exceptional gain, masking an otherwise steady execution quarter. BHEL delivered one of the sector’s cleanest beats; its power-sector execution accelerated, margins expanded sharply, and operating leverage amplified the gains. Waaree Energies more than doubled revenue as module production scaled.

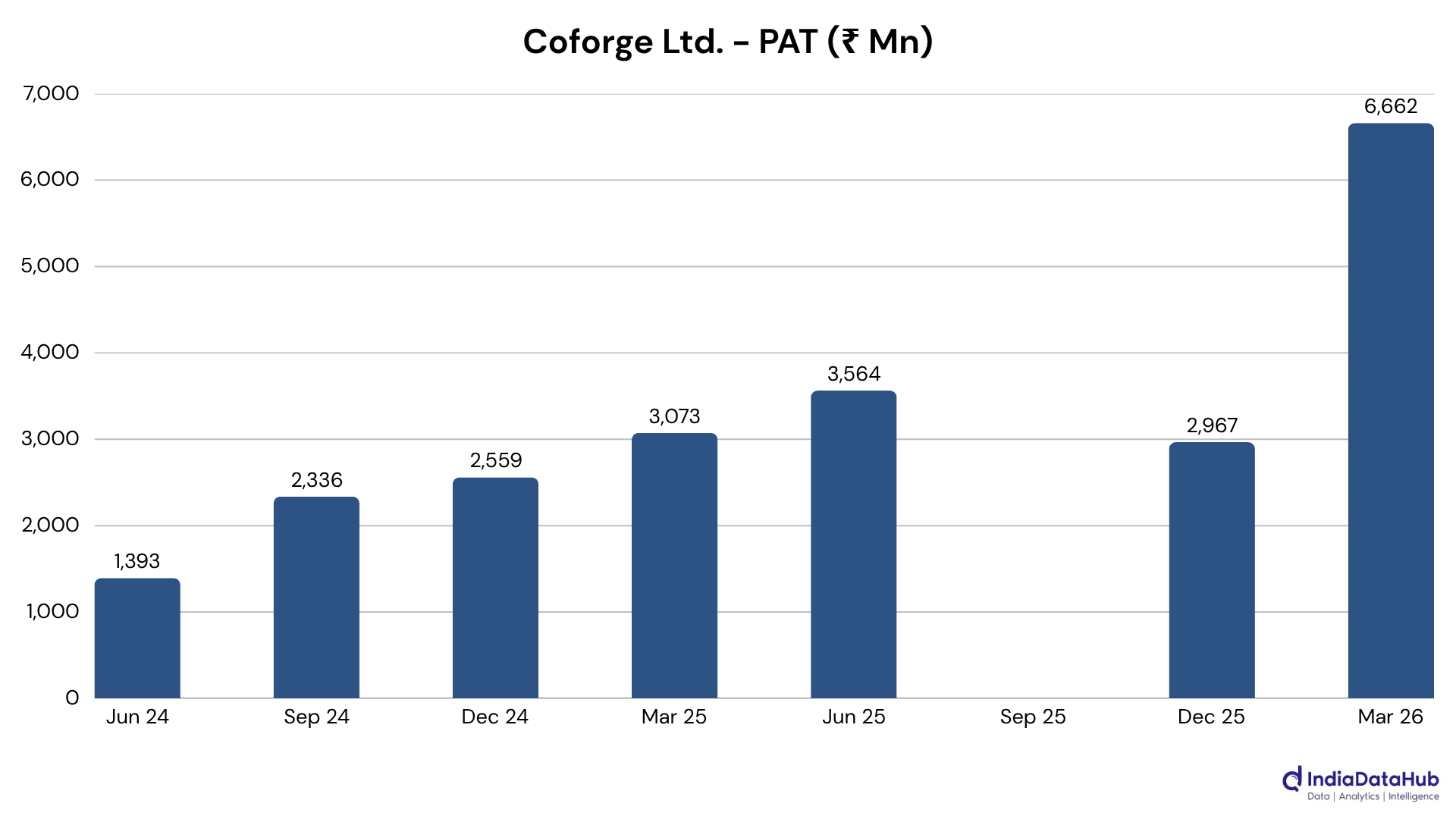

Information Technology returned to cleaner growth this quarter (revenue up ~12%, EBITDA up ~14%, profits up ~14%) with the sector narrative shifting from cost-driven margin defence to more genuine demand recovery. TCS reported record deal wins and margin improvement. Persistent Systems continued its run of above-average sequential growth. Tech Mahindra’s quarter was more about turnaround execution than broad demand, with sharp margin expansion doing the work that topline growth hasn’t yet delivered.

Services has an improved narrative this quarter. Revenue up ~15%, EBITDA up ~29%, and profits up ~26% make it one of the strongest operating performers in the dataset, a sharp contrast to prior quarters where operating growth failed to translate to the bottom line. Adani Ports crossed 500 MMT in annual cargo, with ports, logistics, and international operations all scaling.

Telecommunications is a clear example of a sector where operating strength and reported profitability have fully decoupled. Revenue and EBITDA grew ~12-15%, but profits fell ~5% as heavy 5G depreciation and statutory costs absorbed the gains. Bharti Airtel’s quarter captured this precisely. ARPU gains, subscriber upgrades, and Africa momentum drove strong operating performance, while exceptional charges, a prior-year tax benefit rolling off, and accelerating depreciation pulled reported PAT lower.

Utilities so far has had a quiet but positive quarter overall—revenue up ~5%, profits up ~24.5%—though the profit outperformance is largely accounting-driven. Deferred-tax credits at Adani Power and Power Grid contributed materially to reported PAT, while underlying EBITDA growth was more modest. NLC India was the exception, where operating leverage genuinely drove the profit surge on record coal output and power generation.

Overall, the March 2026 quarter’s headline earnings growth as of yet looks impressive but requires considerable disaggregation. The ~20% aggregate PAT growth is there, but across multiple sectors, the distance between operating momentum and reported profit is being bridged by tax reversals, exceptional gains, base effects, and provisioning relief rather than demand acceleration. The sectors where those two things are genuinely aligned (FMCG, select Commodities names, Services) stand out precisely because of their relative scarcity this quarter.

Company Spotlights

Lloyds Metals and Energy Ltd. (Commodities): Revenue and profit surged after LSIL consolidation added a large steel-manufacturing stream to the business, while the standalone mining and sponge iron operations also scaled sharply. The bigger story is margin expansion: captive iron ore integration appears to have lowered input dependence meaningfully, pushing EBITDA margins far above last year’s level. This looks less like a normal commodity upcycle and more like a structural scale-shift.

Hindustan Zinc Ltd. (Commodities): Revenue jumped as silver prices surged, zinc realisations improved, and by-product sales became meaningful. Profit grew even faster because zinc production costs fell to record lows, aided by domestic coal, better grades, and scale benefits. With no major one-off support, this looks like a clean commodity upcycle quarter where pricing and cost efficiency worked together.

Eternal Ltd. (Consumer Discretionary): Reported growth looks dramatic, but the year-on-year comparison is heavily distorted by Blinkit’s consolidation, so the headline numbers need care. The cleaner read is that quick commerce is scaling fast, food delivery remains healthy, and Q4 profit improved sequentially. Still, full-year PAT fell despite revenue nearly tripling, showing Eternal is firmly in investment-first mode.

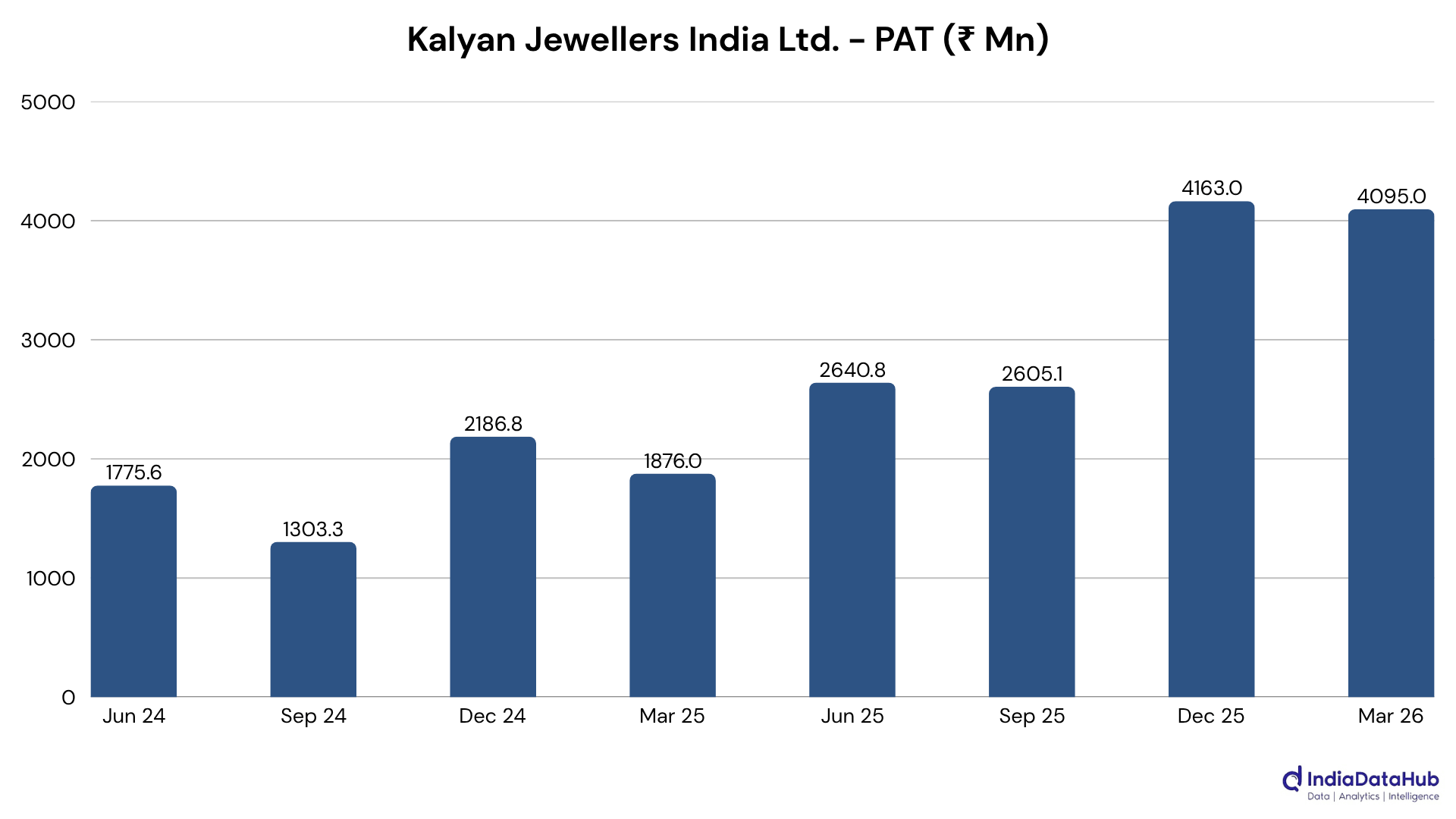

Kalyan Jewellers India Ltd. (Consumer Discretionary): Revenue jumped as high gold prices lifted ticket sizes and festive demand stayed strong. Profit more than doubled, helped by operating leverage, international growth, and Candere turning profitable, even after a one-time labour-code charge.

JSW Steel Ltd. (Commodities): The headline profit jump needs a large asterisk: it was heavily boosted by the one-time BPSL exceptional gain. Strip that out, and the quarter still looks strong, with record sales volumes, firmer domestic steel prices, and better margins driving a healthier operating print. So the result has two layers: an accounting surge on top, and a genuinely improved steel business underneath.

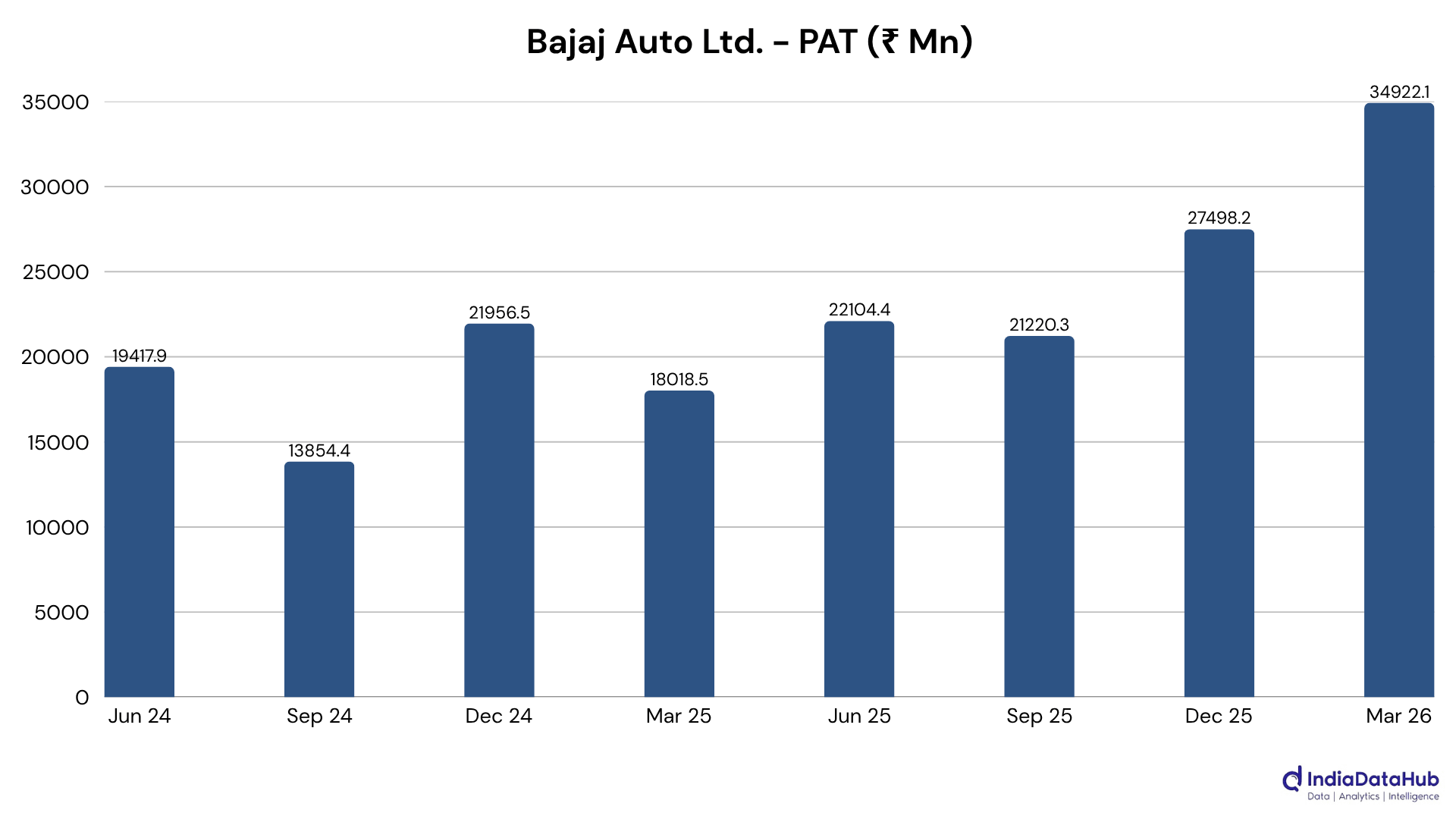

Bajaj Auto Ltd. (Consumer Discretionary): Revenue hit a record as volumes rose across domestic and export markets, with KTM consolidation adding to the topline. Profit more than doubled, though a large KTM-related exceptional gain flattered the headline; standalone growth still looked strong.

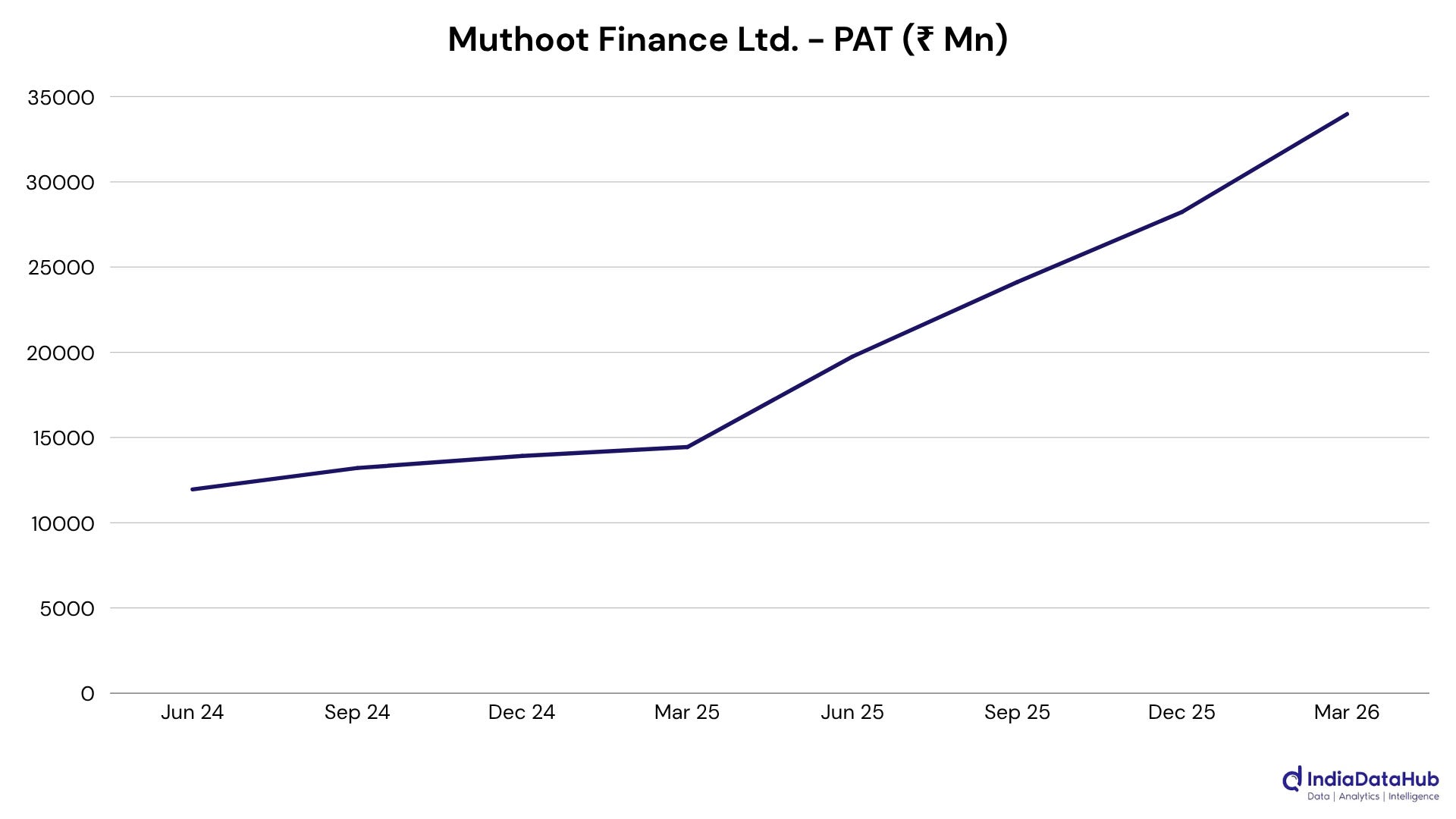

Muthoot Finance Ltd. (Financial Services): Profit more than doubled as gold loan AUM swelled with higher collateral values and strong demand for secured credit. The pace looks impressive, though gold-price-led growth and softer tonnage make sustainability worth watching.

Lupin Ltd. (Healthcare): Revenue surged on a strong US performance, led by complex generics and new launches, while India formulations also grew well. Profit nearly doubled as a richer product mix, operating leverage, forex benefits, and exceptional income lifted margins sharply.

Bharat Heavy Electricals Ltd. (Industrials): Revenue jumped as power-sector execution accelerated, led by thermal project work and a large order book. Profit rose far faster, helped by sharply better Power segment margins, provision reversals, higher other income, and operating leverage.

Coforge Ltd. (Information Technology): Revenue grew far ahead of larger IT peers, helped by Cigniti consolidation and strong deal wins across BFS, insurance, travel, and healthcare. Profit more than doubled, though a deferred-tax reversal boosted the headline number materially.

That’s it for this edition. The majority of the companies are yet to report their earnings, so stay tuned as we explore this season in the coming weeks. See you soon!