A billion internet users, Data consumption, Exports and more...

This Week In Data #140

In this edition of This Week In Data we discuss:

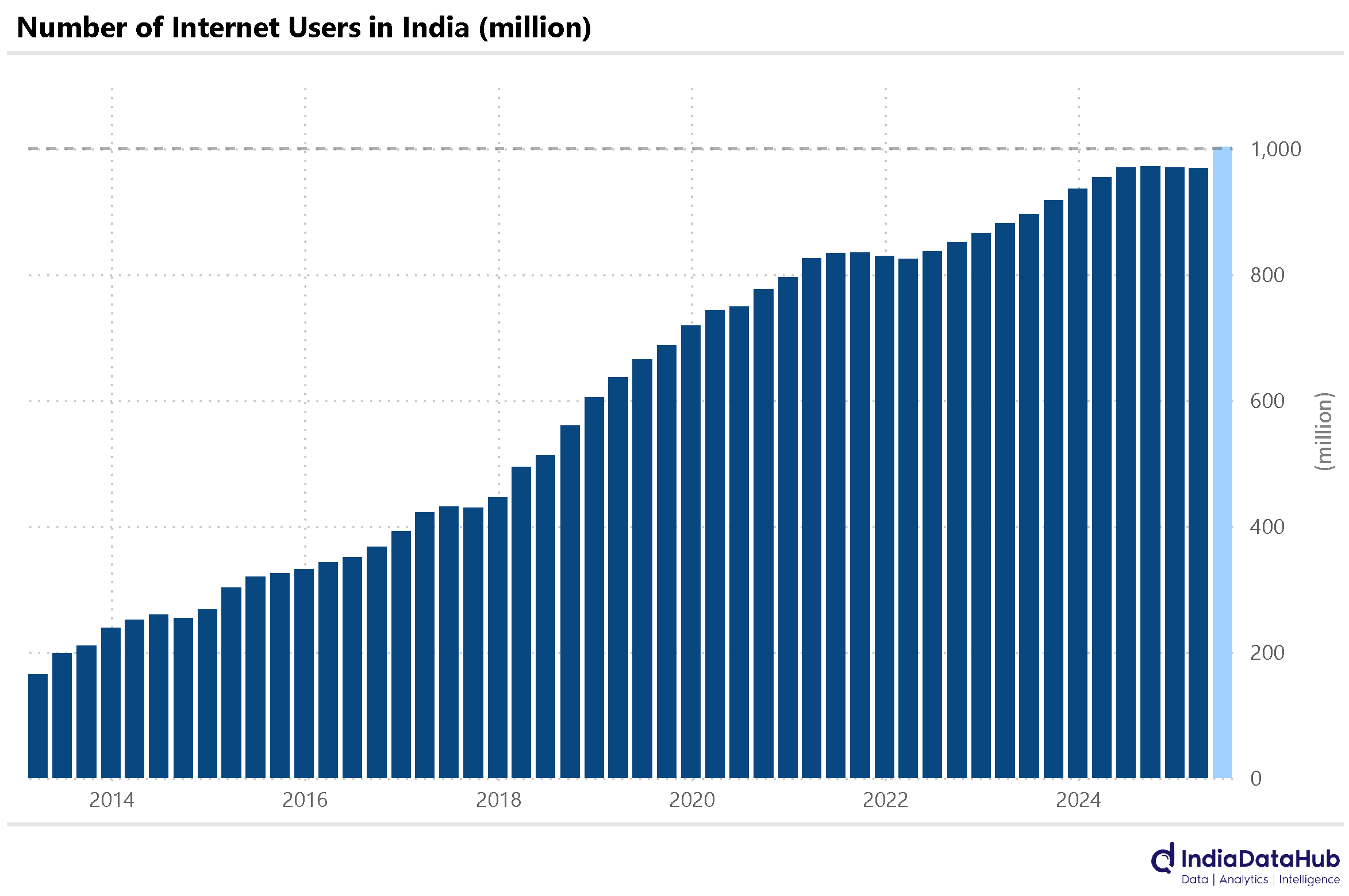

The number of internet users in India has crossed a billion!

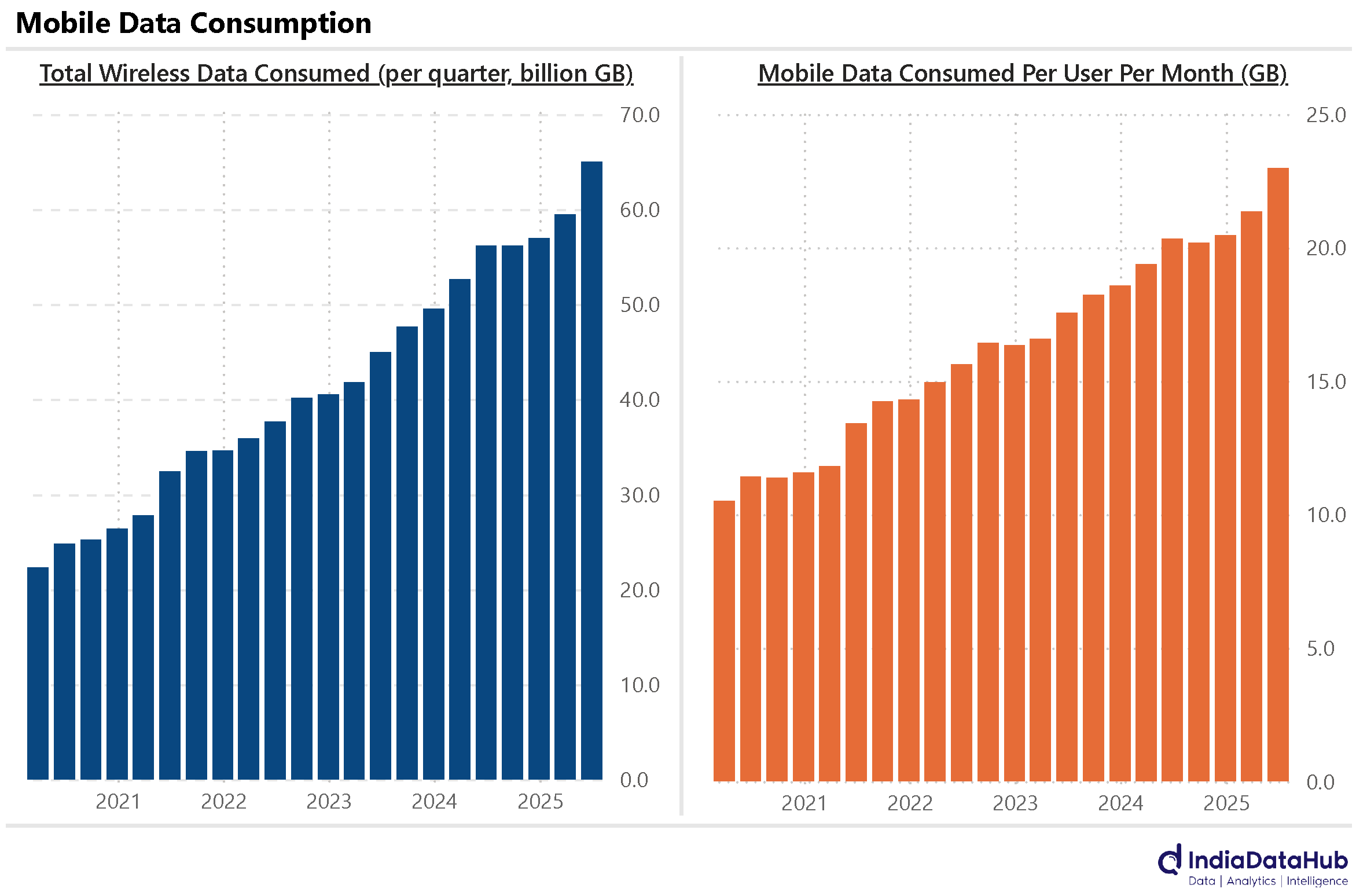

Data consumption continues to grow in double digits

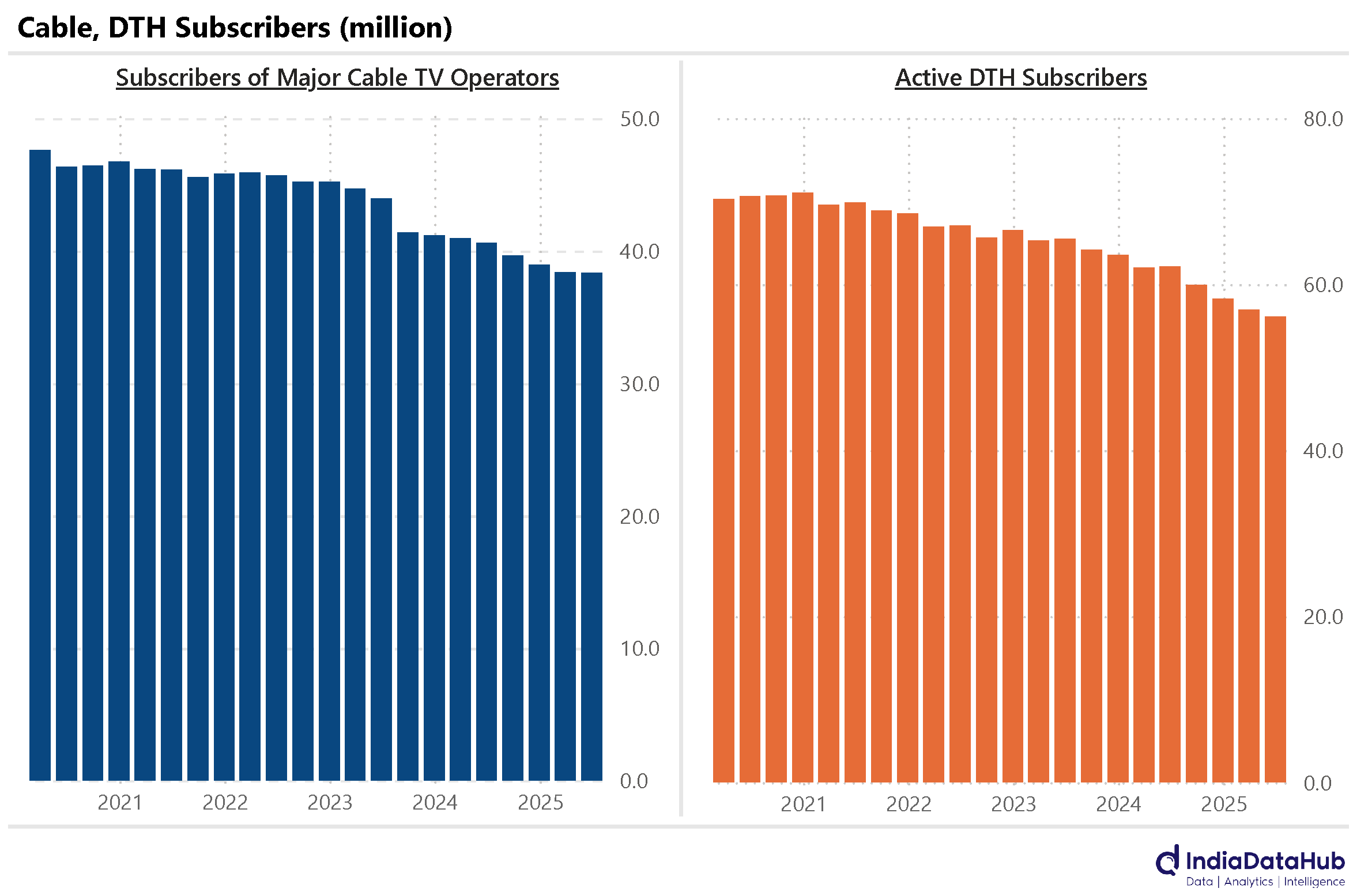

Cord cutting has continued

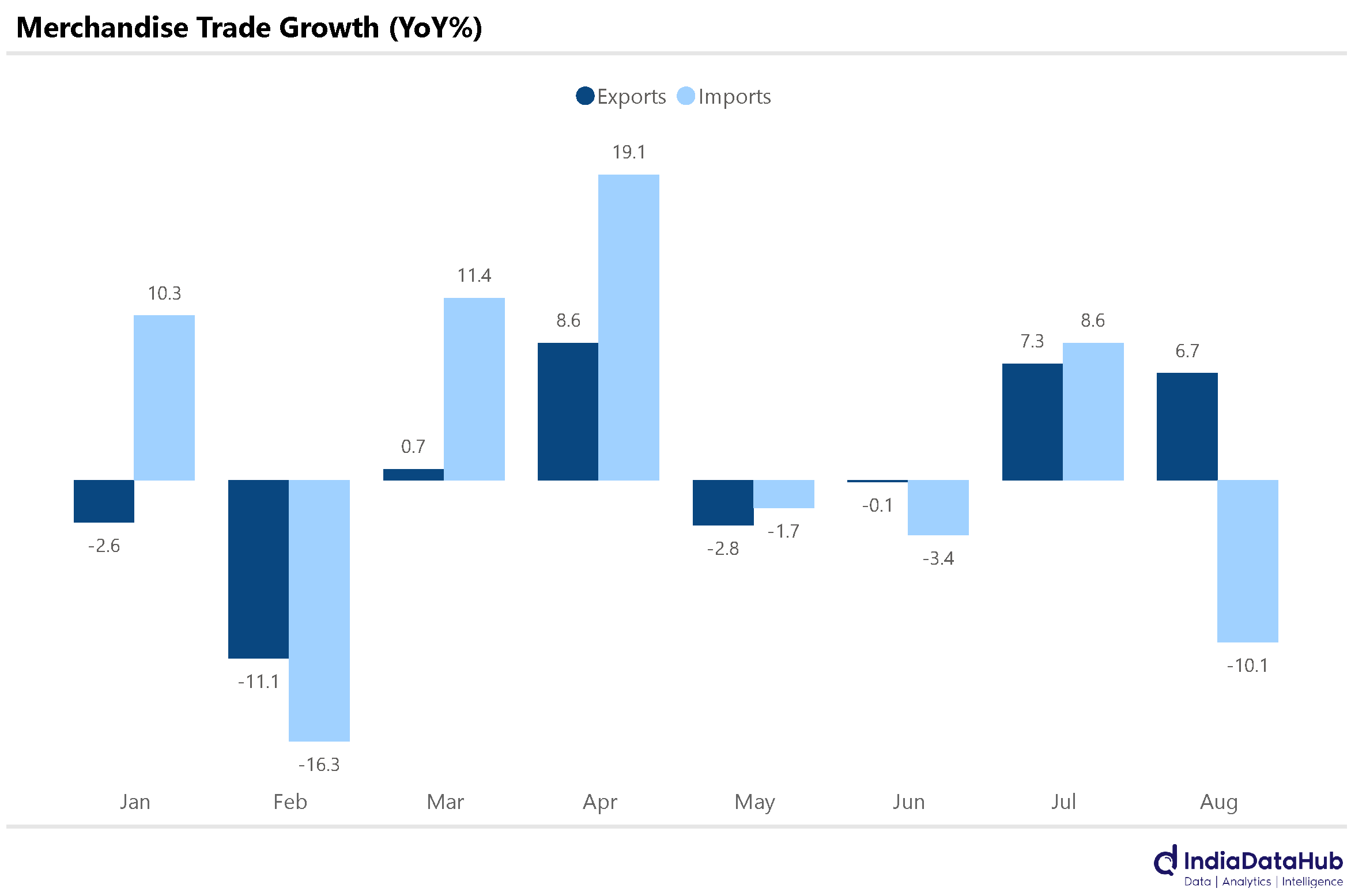

Exports see another month of reasonably strong growth

Imports fall 10% due to collapse in Gold imports

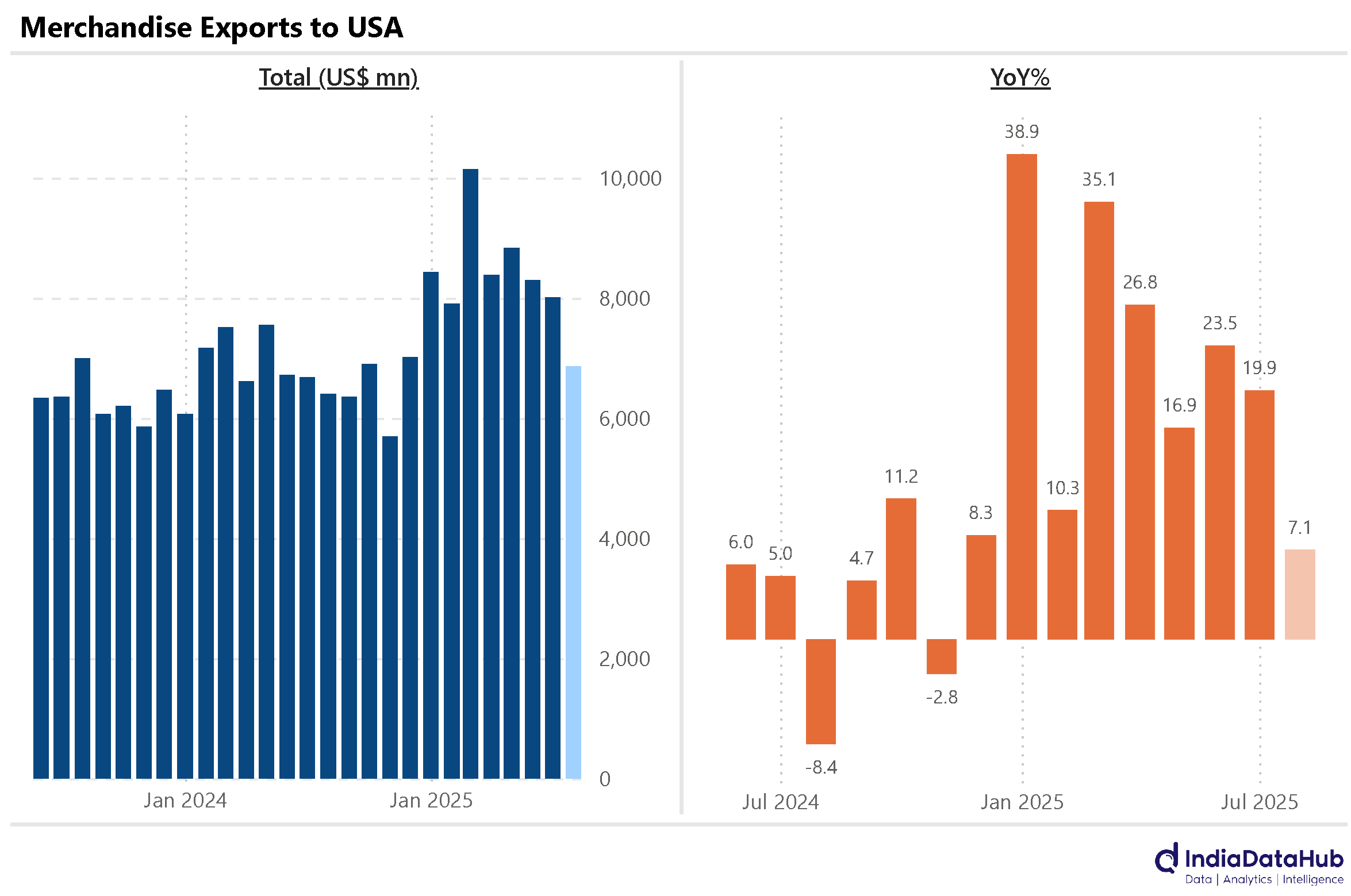

Exports to US slow as tariffs kick in

US Fed cuts interest rates by 25bps

Most other central banks keep interest rates unchanged

A billion. Yes, that is how many internet users we have in India. As of June this year. The June quarter saw almost 35 million increase in internet users, the highest addition in almost 7 years. Of course, this does not mean that a billion Indians use the internet, for there will be instances of multiple internet connections, especially in the cities. The adult population base of India is around a billion people. And so even if we assume that there are 100-150 million cases of multiple connections, we are fast approaching near universal access to the internet. That is a phenomenal achievement considering that a decade back, in 2015, India had just over 300 million internet users. A more than tripling of users in a decade!

Most of these users are, of course, wireless users. Less than 5% of the internet user base is fixed line users. And these wireless internet users consume a lot of data. Like a lot. And the data consumption continues to grow. During the June quarter, 65 billion GB of data was consumed, almost 10% growth QoQ. And this translates to over 20GB of data being consumed per user per month! While there has been some slowdown, data consumption even on this high base has continued to grow in the mid-teens in the last few quarters.

One flipside of this, though, is cord-cutting. The number of users on DTH or Cable TV continues to decline. In the last 5 years, the number of DTH and Cable subscribers have declined by 20%.

Merchandise exports grew by 7% YoY in August, the second consecutive month of high single digit growth. Exports had grown by a similar magnitude in July as well. Electronic goods and Gems & Jewellery were the fastest growing items with exports growing 25% and 15% respectively in August. These two categories contributed almost a third of the growth in exports in August.

Imports declined 10% YoY in August almost entirely due to the more than halving of Gold and Silver imports. Excluding these two, imports saw a modest low single digit growth. YTD, Gold imports have declined by 30% YoY as high prices seem to have weighed in on demand.

The most important data point from the trade data release, though, was exports to the USA. And after months of strong growth, export growth moderated to 7% YoY, the slowest growth this year. Note that the tariffs on Indian goods had kicked in in August. The full impact of the tariffs, though, will be felt next month, and so it is almost a given that exports to the USA will decline in September. The positive takeaway, though, is that overall export growth remained unchanged, despite the sharp moderation in export growth to the USA. If this continues in September also, then it would suggest that in the immediate near-term, at least, there has not been much impact of US tariffs on Indian exports. We shall see…

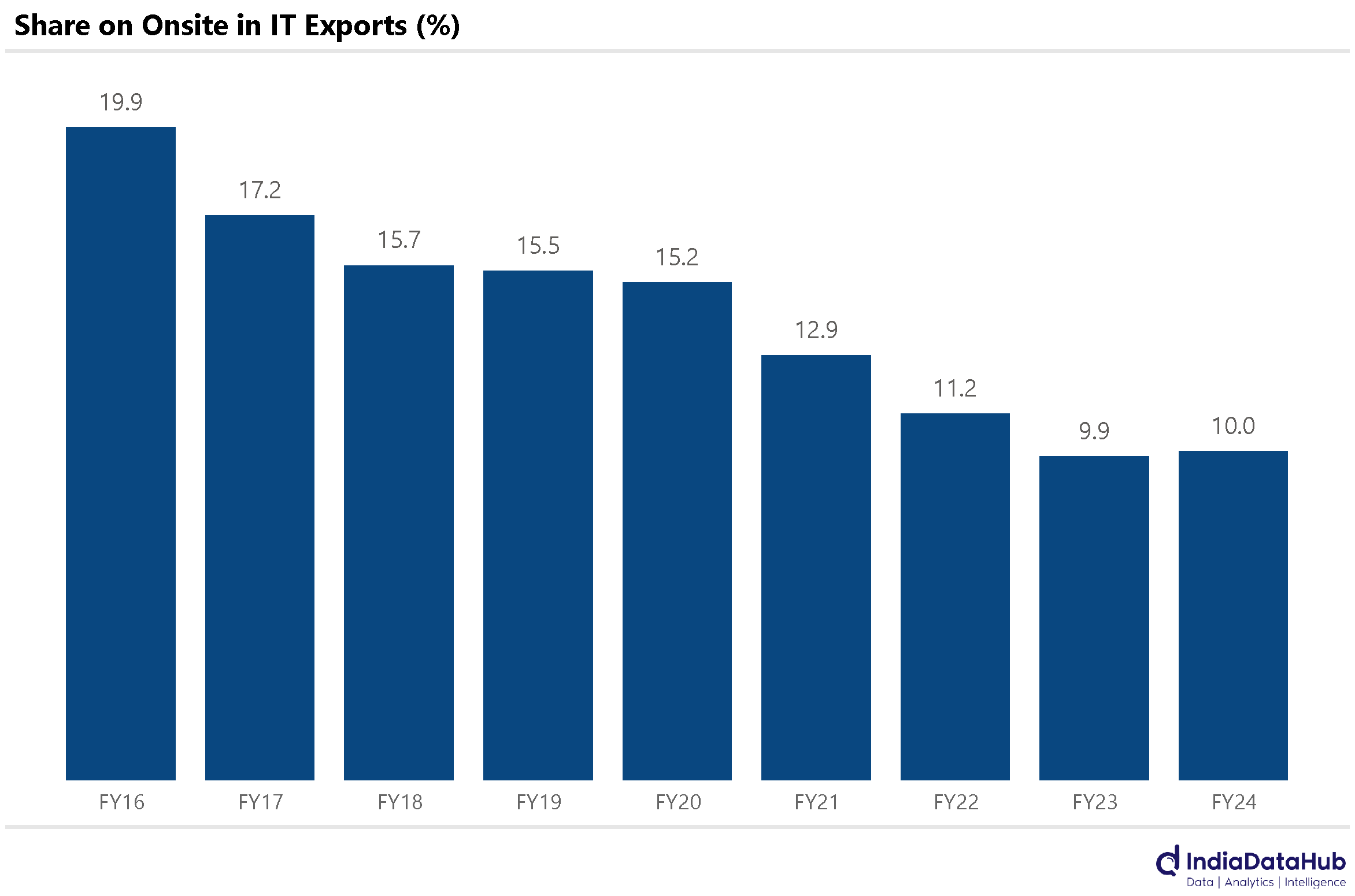

Related to this is the potential impact of the changes in the H1B visa on India’s services exports. While it is unclear what the new H1B visa policy will be, what is worth noting is that from an Indian IT services perspective, the share of onsite work has gradually declined, and it is now a relatively small proportion of their total work. In FY24, only 10% of India’s IT exports were attributable to onsite work, down from 20% in FY16. The share of exports to North American while still large at 55% last year, has fallen from 61% in FY16.

Globally, it was relatively light on economic data releases. That said, several major central banks held policy meetings this week. In Brazil, the central bank opted to keep its benchmark Selic rate unchanged at 15%, the second consecutive policy pause. The previous one being in July. Unlike other countries where interest rates are falling, Brazil has seen interest rates increase. A year ago, the policy rate was 10.75% (425bps lower than current). And at 15% the current policy rate is the highest in the last several years.

In the UK meanwhile, the Bank of England also maintained its policy interest rate, the bank rate, at 4%, following the 25bps rate cut last month. Central banks in South Africa and Japan also opted to maintain their current interest rates.

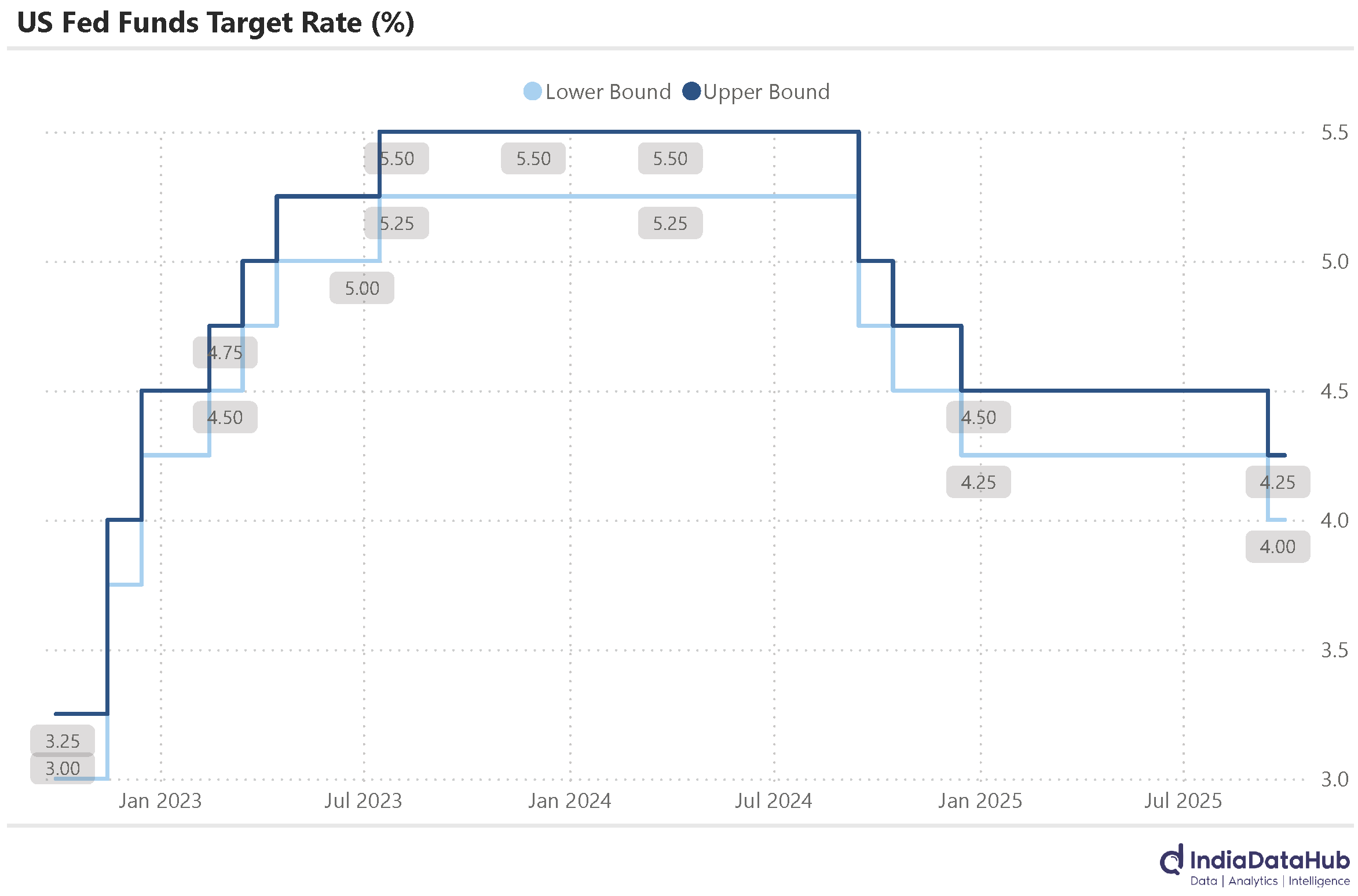

Lastly and most importantly, the U.S. Federal Reserve decided to reduce its target range for the federal funds rate by 25 basis points, bringing it down to 4.00–4.25%, citing a weakening labour market and moderate economic activity in the first half of the year. This is the first rate cut from the US Fed this year, the last policy change (rate cut) was in December last year. Markets are currently expecting another two 25bps rate cuts from the Fed in the two remaining meetings this year – October and December.

That’s it for this week. See you next week…