Aviation slowdown, Gold holdings, Vi back to growth and more...

This Week In Data #160

In this edition of This Week In Data, we discuss:

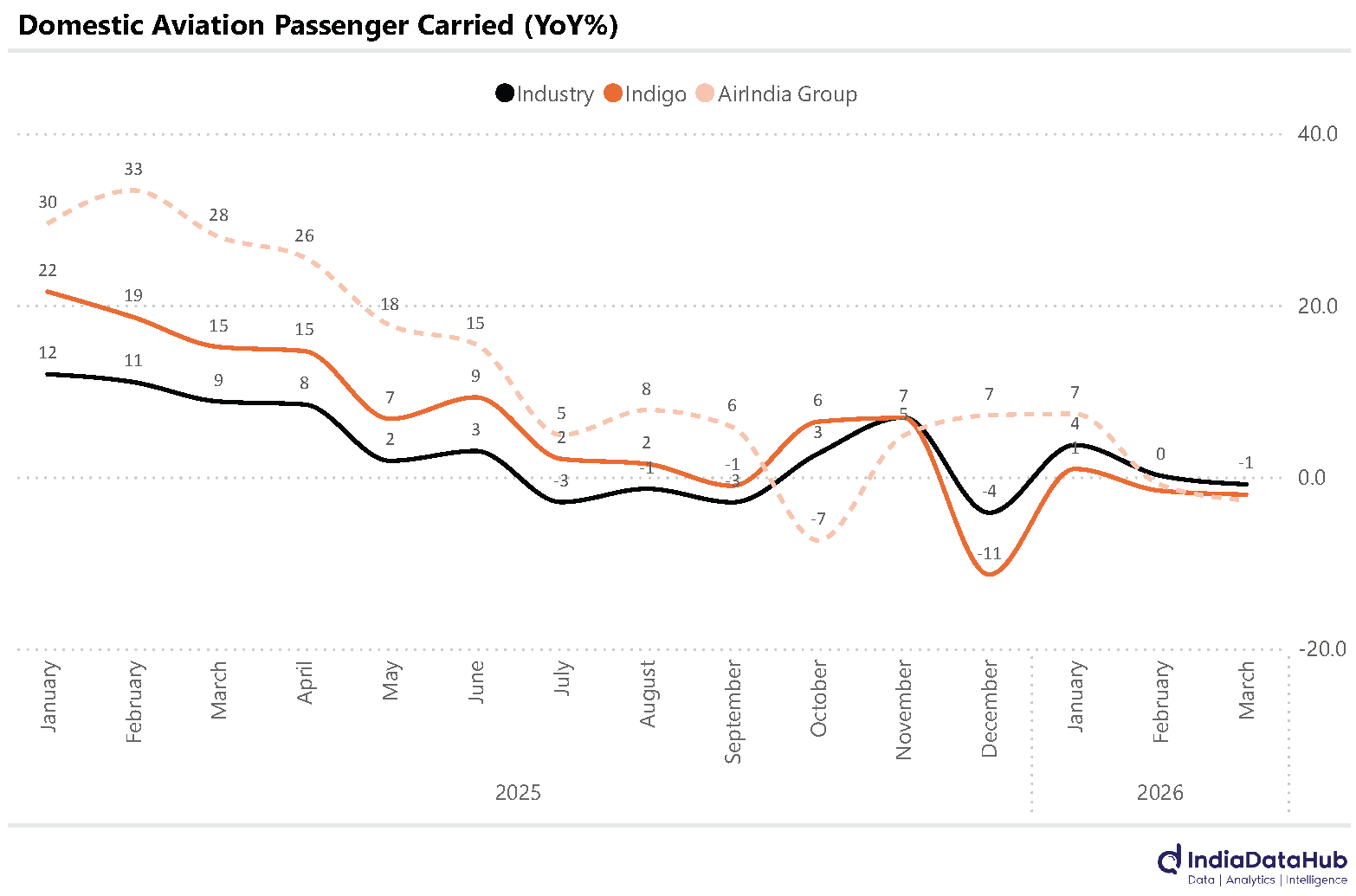

Domestic aviation sector is seeing a sharp slowdown

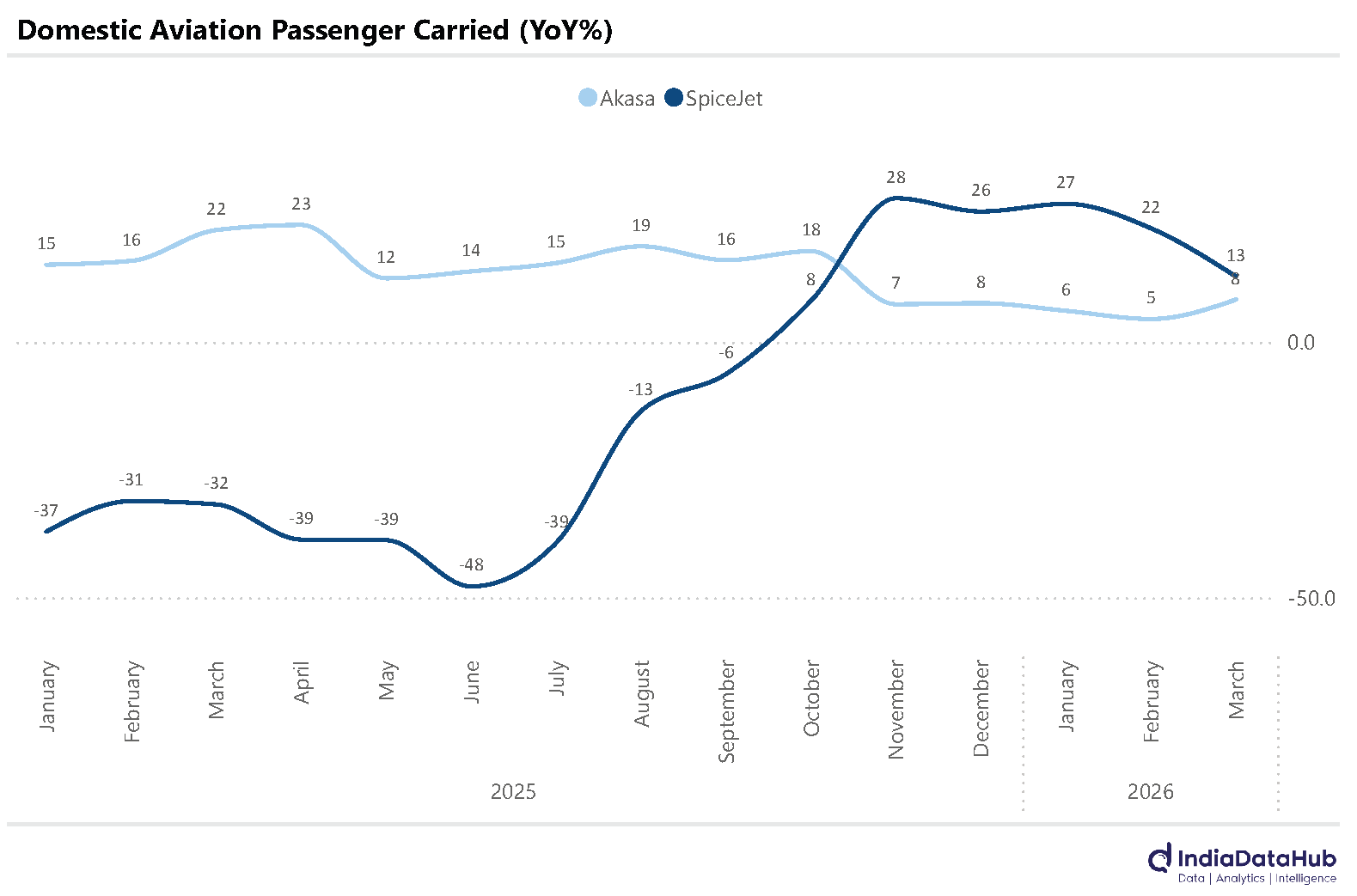

While Indigo & Air India are seeing decline, SpiceJet & Akasa are seeing growth!

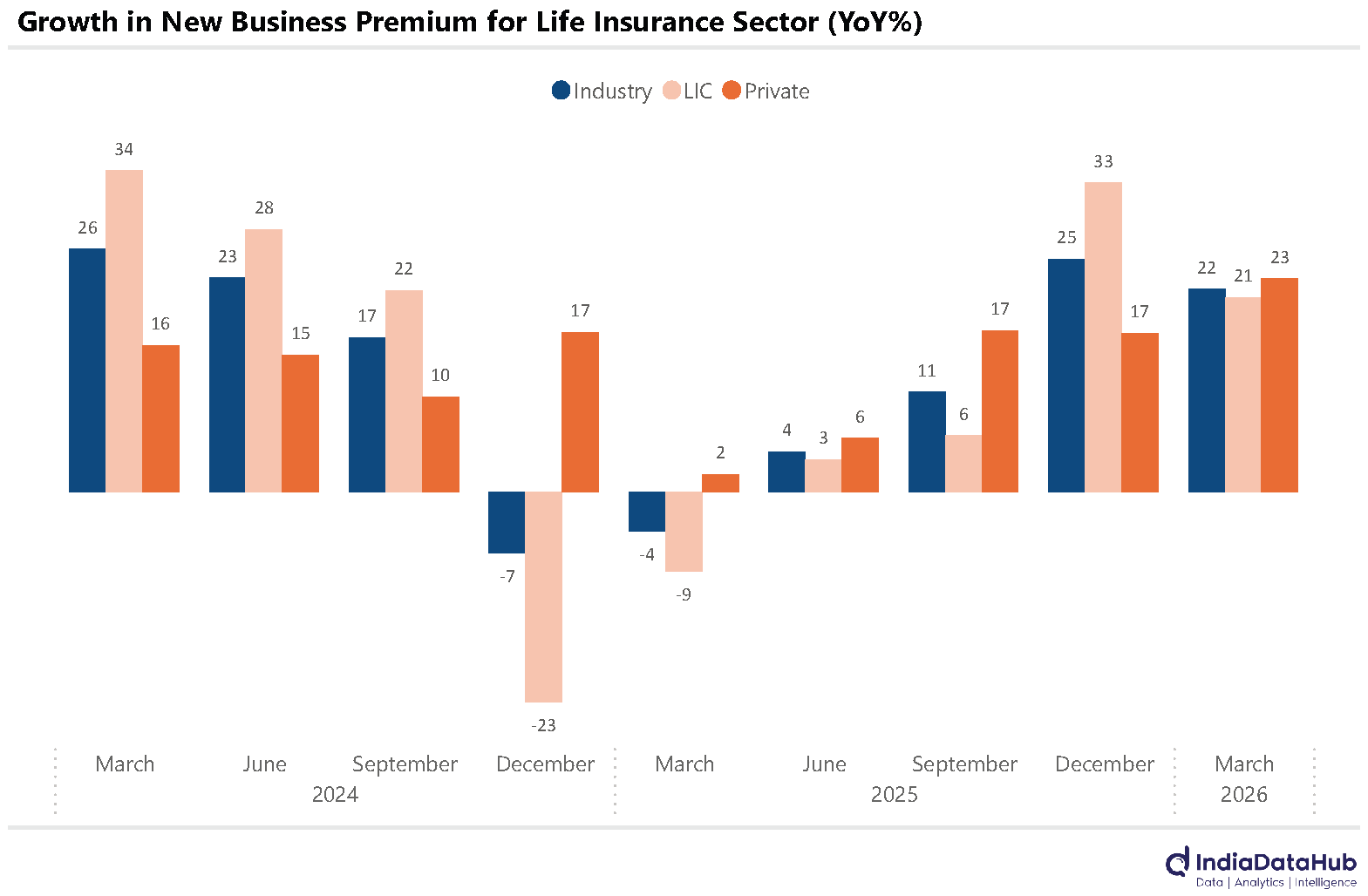

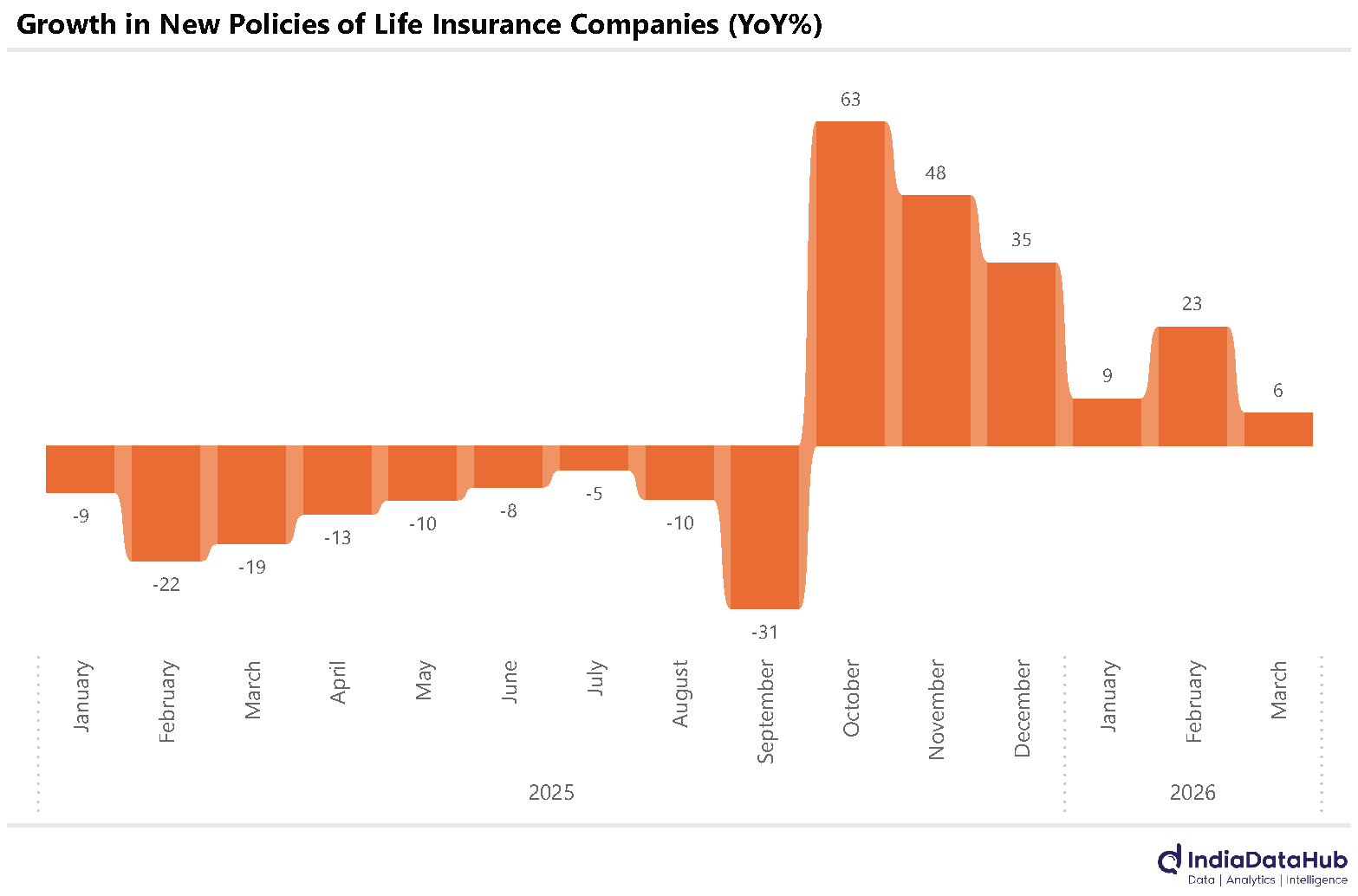

Life Insurance Sector is seeing strong growth driven both by LIC and Private insurers

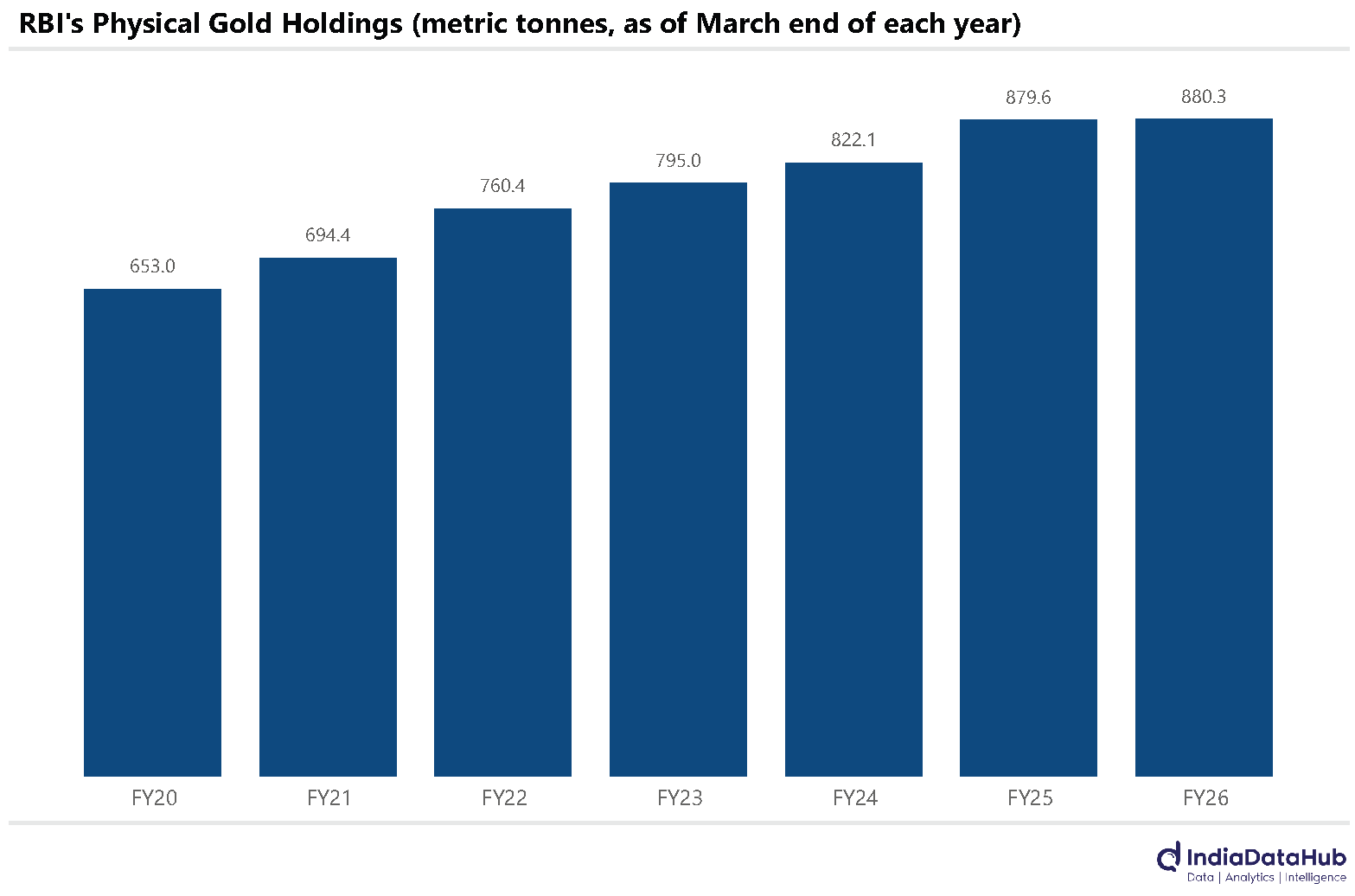

After 5 years of steady increase in Gold holdings, RBI takes a pause in FY26

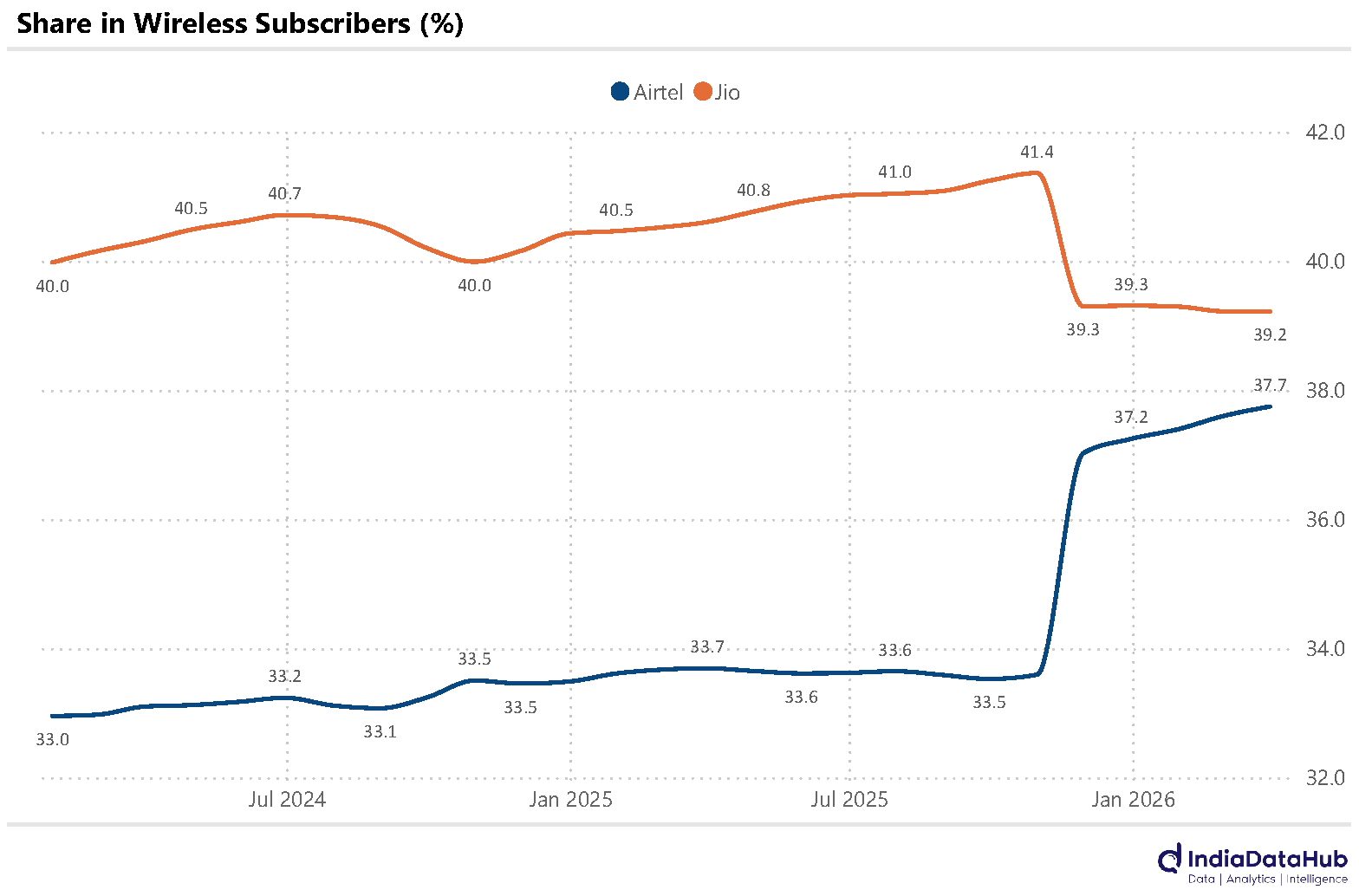

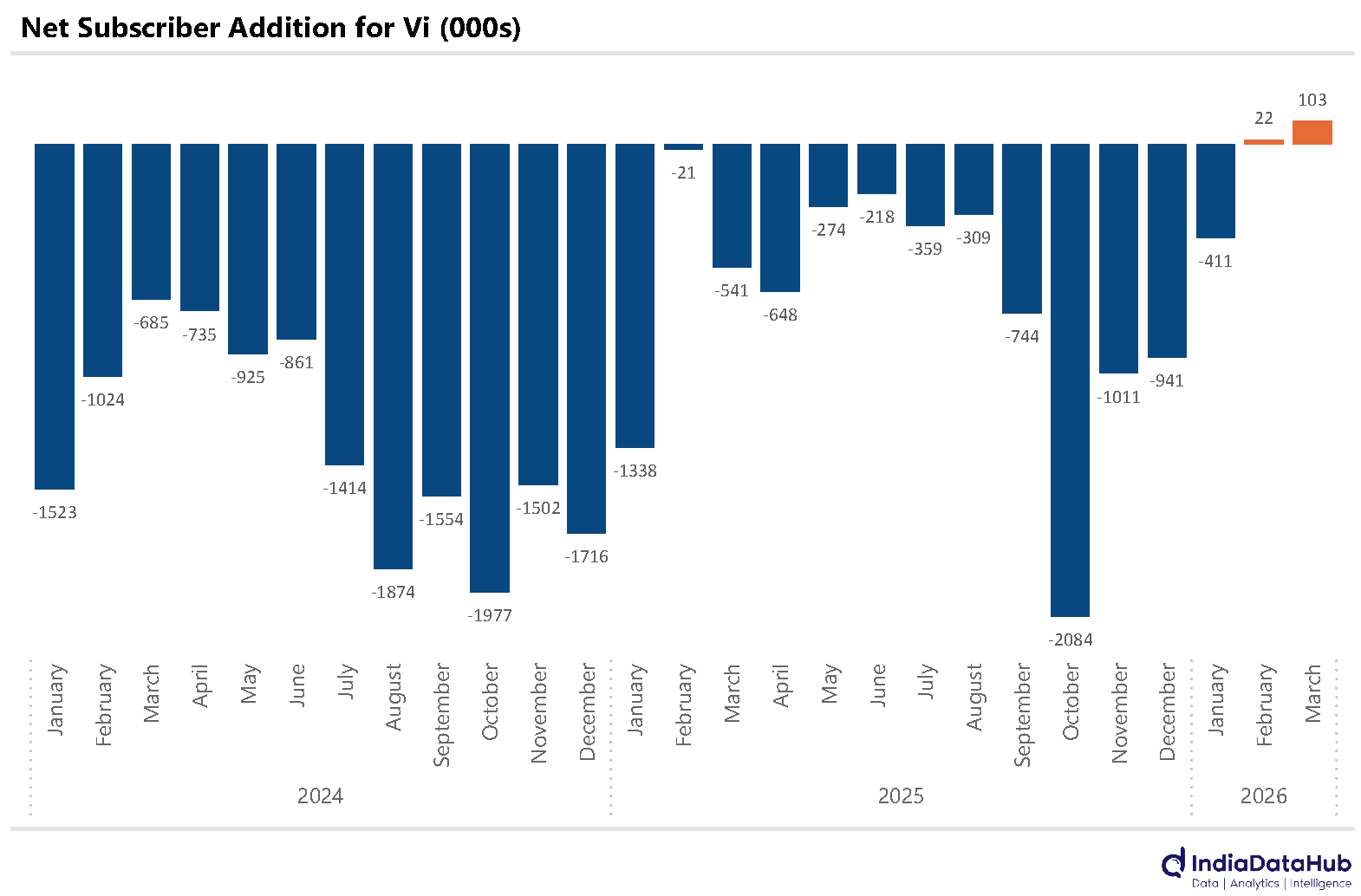

Wireless subscriber addition continues to remain strong and Vi has finally returned to growth

Domestic aviation passenger traffic growth declined by 1% YoY, the weakest performance since December (which was largely due to disruptions at Indigo). February had also seen a modest 0.1% growth in passenger traffic, and thus the last two months have seen fairly weak growth in the domestic aviation sector. With Jet fuel prices having increased further in April, the weak growth is likely to continue.

Both Indigo and the Air India group saw a decline in passenger carried, while smaller airlines like SpiceJet and Akasa saw strong growth. SpiceJet seems to have stabilised its operations and is returning to growth. Its share in passenger traffic has doubled to 3.8% in March from a low of 1.9% in September last year

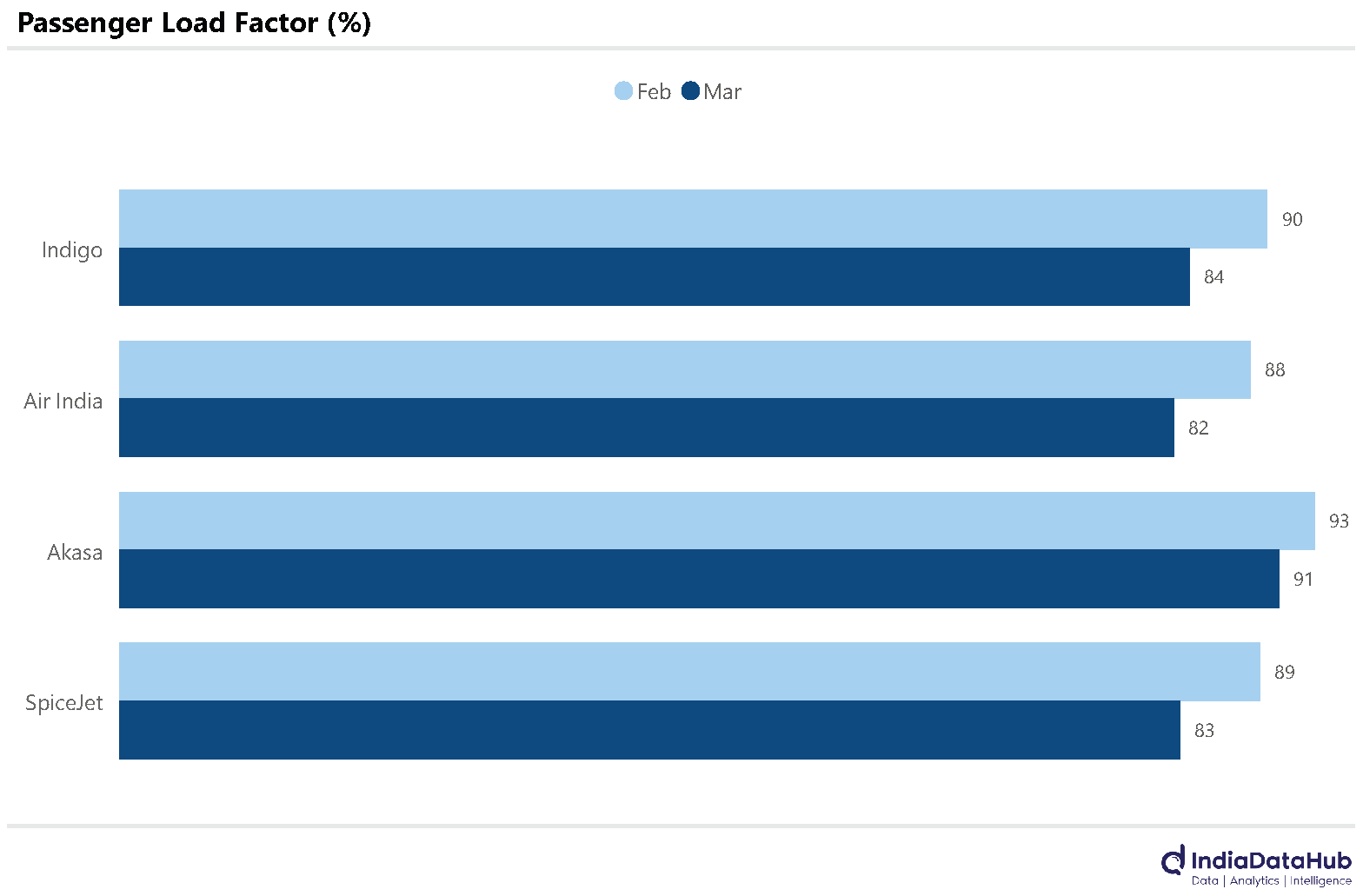

More importantly, though, the passenger load factor declined sharply (~6ppt) pretty much across the board for all the airlines. For Indigo, at 83.5% in March, the passenger load factor was the lowest since October last year.

The Life Insurance sector is seeing strong growth. New business premium grew over 20% YoY in the March quarter, the second consecutive quarter of over 20% growth. This comes after 4 consecutive quarters of close to 0% growth. Both LIC and the Private insurers saw over 20% growth during the March quarter. LIC’s market share in new business premium has stabilised at ~57-58% for the last few quarters.

The growth in new policies sold, however, moderated to a 6-month low of 6% YoY in March 2026, with both LIC and Private insurers seeing this slowdown in growth.

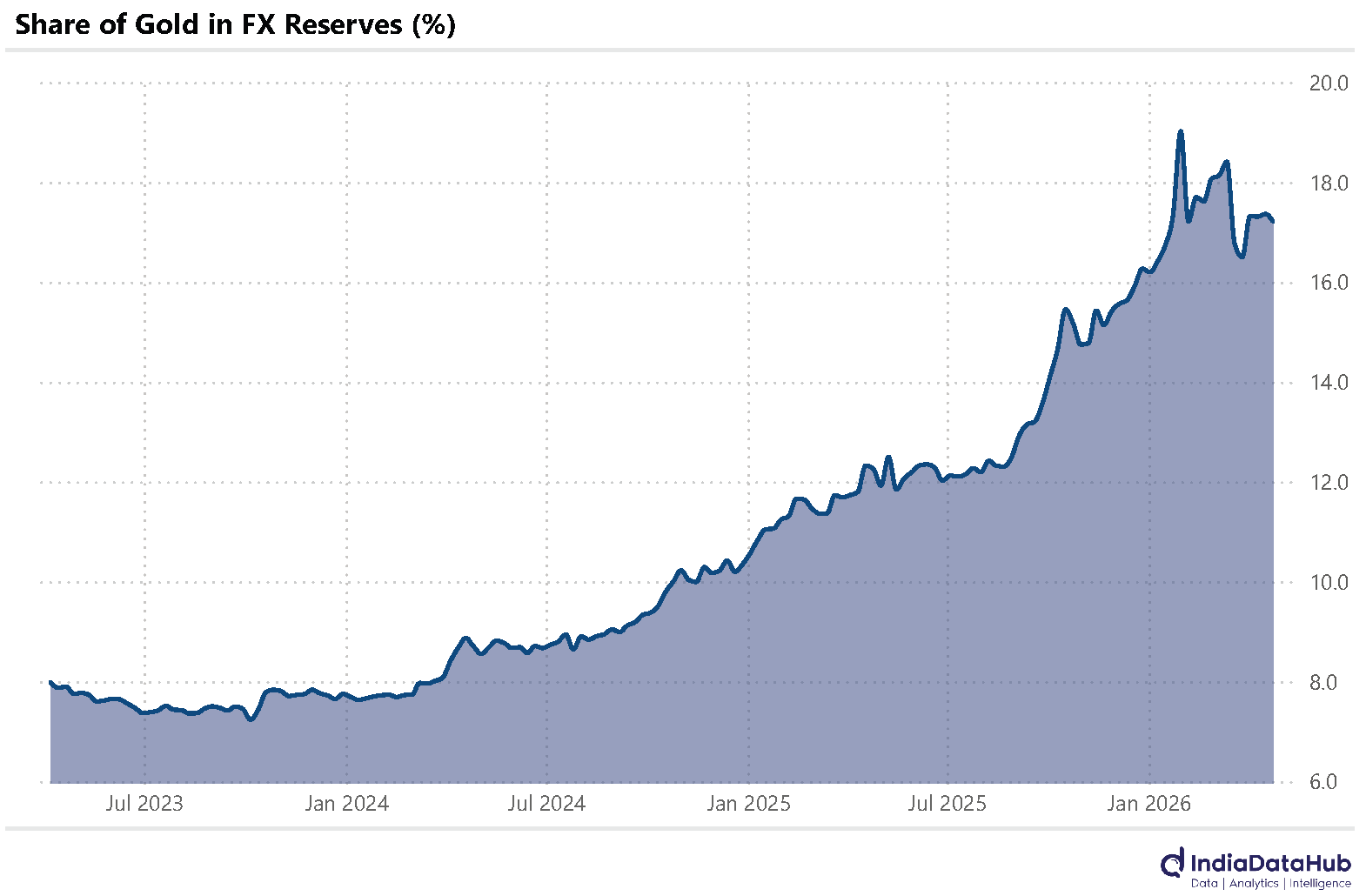

The value of Gold reserves has increased by over 50% since the start of the last financial year. At the start of April 2025, the value of FX reserves held in Gold totalled just under US$80bn. As of the last week of April this year, this has increased to US$120bn. Gold holdings now account for 17% of total FX reserves, up from just under 12% a year back.

However, almost the entire increase in this is due to the higher value of gold holdings. In volume terms, RBI’s holdings of physical gold have increased by less than 1% or less than 1 metric tonne over the past year. Indeed, FY26 was the first year in recent times when the RBI did not add to its physical gold holdings. In each of the preceding 5 years, the RBI, on average, increased its gold holdings by ~45 tonnes.

The growth in wireless subscribers has continued in the last few months. After the adjustment for M2M subscribers in November, the subscriber addition has remained strong. The last 4 months have seen 7 million subscribers being added each month, with March seeing over 8 million subscribers being added – this is the highest monthly addition in over 3 years (excluding the Nov 2025 M2M adjustment).

And the increase is mostly due to Airtel and Jio, with Airtel closing the gap to Jio in the wireless subscriber market share. As of March, Airtel had 38% of the wireless subscribers while Jio had 39% of the subscribers.

And after losing subscribers in every single month for the last few years, Vi seems to have stabilised its subscriber base. In the last two months, its subscriber base increased by ~100k. This is, of course, not a lot. But remember that it had lost subscribers in each of the previous 36 months with an average monthly loss of 1.15 million.

That’s it for this week. See you next week…