Central Bank Watch, Inflation and Monetary Policy...

This Week In Data #105

We missed pushing out the TWID last week. Our apologies for that but we were so swept away by Gukesh’s victory that financial markets took a step back. I think that counts as a good enough excuse😊

We start this edition with global because several Global central banks have been in action in the last few days. The European Central Bank lowered all three key policy rates by 25bps the week before amid slower-than-expected growth. The Fed followed it up this week with a 25bps cut in the Fed funds target rate. The Fed funds rate now stands in the band of 4.25-4.5%. The Bank of Mexico also lowered its overnight interbank funding rate by 25bps from 10.25% to 10%. Finally, the Bank of the Philippines also reduced its policy rate by 25bps to 5.75%.

On the other hand, the Bank of England maintained its policy rate keeping the Bank rate unchanged at 4.75%. Note that in the UK inflation has risen for two consecutive months now – this week the November CPI print came in at 2.6% YoY, up 30bps from October. Despite weak growth and very low inflation, the People's Bank of China (PBoC) maintained its 1-year Loan Prime Rate unchanged at 3.1% and the 5-year rate at 3.6%. The Central banks of Thailand and Indonesia also kept their policy rates unchanged this week. Not to mention earlier this month even the RBI kept its policy rate unchanged.

While most central banks are thus either cutting interest rates or keeping them unchanged, the one exception to this is Brazil. The Central Bank of Brazil hiked its key policy rate, the Selic rate, by 100bps to 12.25% the week before.

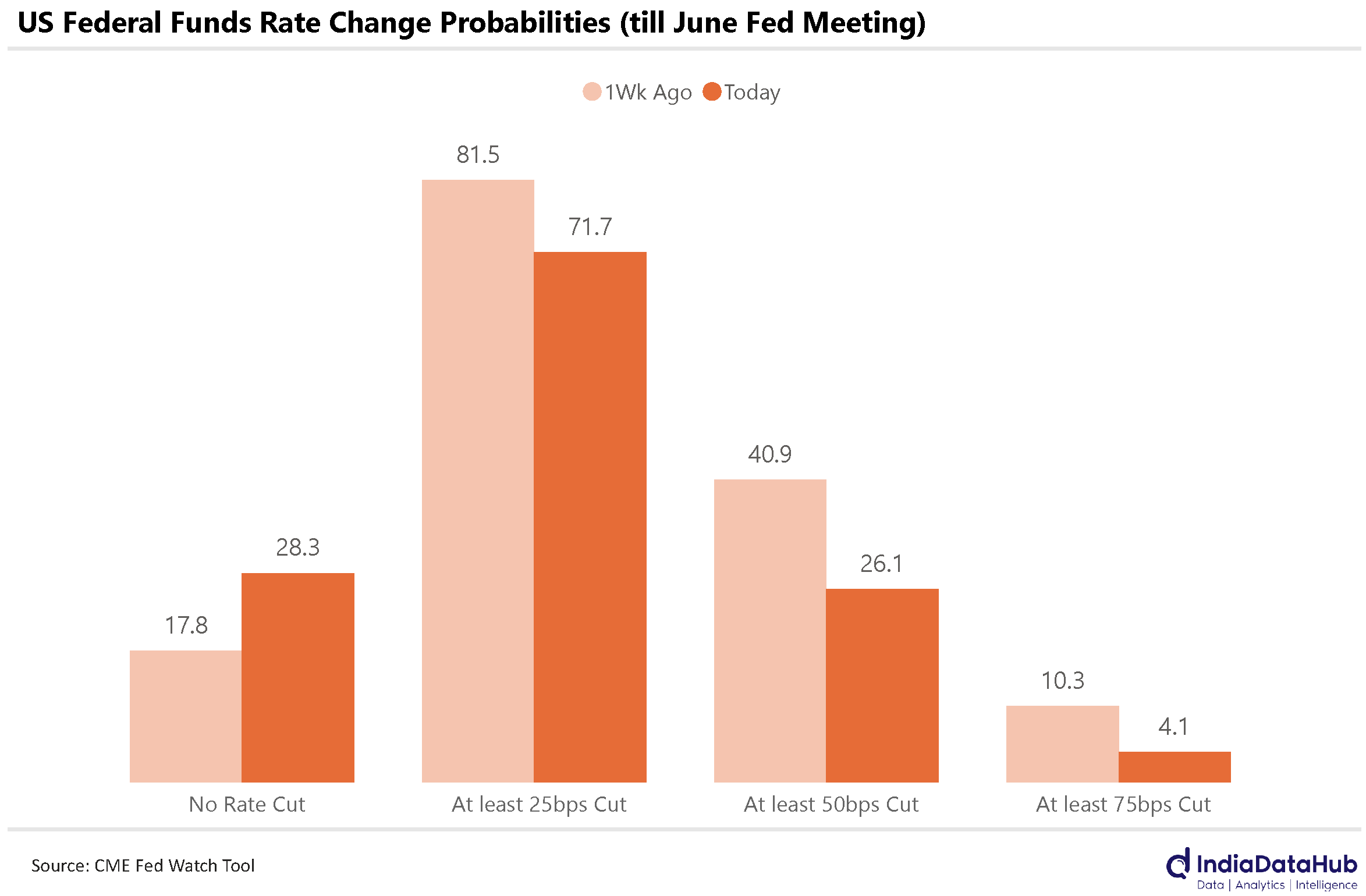

In large part, this divergence in monetary policy also stems from what is happening in the US and the uncertainty over how deep the monetary easing in the US will be. Growth in the US has not seen a material slowdown. Just this week the revised estimate for 3Q GDP saw GDP growth being revised upwards to 3.1% SAAR, up from the provisional estimate of 2.8%. Inflation has also not exactly fallen dramatically. US CPI was at 2,75% YoY in November and the Fed’s preferred measure the core PCE deflator was at 2.8% YoY - the highest since April 2024 and well above the 2% target.

Accordingly, the commentary from the US Fed post the rate cut was not very dovish and this resulted in the global market sell-off. The markets now expect only a 25bps rate cut from the Fed in the first half of 2025. Just a week back, they were expecting 2 or potentially even 3 rate cuts by June next year.

Back home we had the November trade data released earlier this week. And ideally, we should comment on it as the data showed a very dramatic increase in imports and thus the trade deficit. However, it looks like the data is wrong, especially the import data. And so, we will reserve our judgement till the data is revised.

FX reserves have continued to decline. In the last two weeks reserves have fallen by US$5bn. As of mid-December, India’s FX reserves stood at US$652bn a fall of US$52bn from the peak in late September. That said, reserves are still up US$35bn on a YoY basis. Effectively, reserves rose sharply in the first half of this year and have then fallen towards the end but still ending the year higher than at the start of the year. So, the fall in reserves is not really worrying. The question for debate is whether the RBI should have put up such an aggressive defense of the rupee (by spending its reserves).

Not a lot of other data this past week. But in the prior week we had the CPI data for November. Inflation did moderate as expected to 5.5% from 6.2% in October. And the core CPI remained stable at 3.6% (dipped by 3bps). So, the entire moderation was due to the fall in food inflation. Food inflation fell by 150bps to 8.2% in November. Food inflation should moderate further in December and thus the headline CPI should fall further towards 5%.

Unfortunately, a 5% CPI is neither low nor very high. Or to paraphrase that famous Ajit dialogue it is akin to liquid oxygen – not low enough to cut rates and not high enough to raise rates. So, by the time the RBI meets next (in early Feb), inflation data by itself would not be sufficient for any rate action.

But between now and early Feb, there will be several data releases which will give us a sense of the growth trajectory in India. Recall that RBI’s growth projection for FY25 implies a recovery in the second half. Additionally, there will be the budget on 1st February which will lay down the path for fiscal policy. There will also be another Fed meeting at the end of January. And last but not least, the new government would have taken charge in the US.

So, the first quarter of 2025 is thus going to be quite eventful. Not just for the world of finance and markets but for us at IndiaDataHub. We can't wait to release some of the things we have lined up. And to be prepared for what lies ahead, we are taking the next week off. Merry Christmas everyone and wish you all a very happy new year. See you on the other side.