In this edition of This Week In Data, we discuss:

CPI Inflation rises to over 3% in February but continues to remain modest

Oil prices rise to US$100/bbl and are up almost 50% YoY in INR terms

India’s energy balance has worsened in the last few years

Domestic oil production has declined

Imports of Petroleum products, and not just crude oil, have increased

China’s exports and imports are off to a strong start in 2026

CPI Inflation rose to 3.2% YoY in February, up from 2.7% in January. This is the highest reading since April last year. However at 3.2% it remains still remains below the 4% target set for the RBI’s Monetary Policy Committee. So despite the rise, CPI remains low and comfortable. This, however, is a rear-view mirror analysis. Since then, international Oil prices have shot up due to the hostilities in the Middle East. The price of Brent crude, which averaged U$71/bbl in February, has now crossed US$100 per bbl. If they sustain at this level, and given the sharp depreciation in the rupee in the last few months, this will translate to an almost 50% increase in Oil prices on a YoY basis in INR terms.

Petroleum products directly have a ~7% weight in the new CPI basket. So a 50% increase in prices will, ipso facto, push up inflation by ~3-4ppt, pushing CPI above the upper end of the MPC’s threshold of 6%. This, of course, assumes that the international oil prices are fully passed on to the consumers. They most likely will not, at least not in the short term. To begin with, it will be the Oil companies which will absorb the higher prices, and if prices remain high for more than a few weeks, then the Government will be expected to also chip in.

But petrol, diesel and LPG are just one source of impact of higher oil prices. Almost every manufactured item that we consume has some element of petroleum. And the services required to deliver those goods require petroleum. Suffice to say that such a sharp increase in prices, compounded by the fall in the rupee, will adversely impact the price system. And what might exacerbate this, at least in the short term, is the risk of shortages, which might cause production outages, curtailing supply. But given the uncertainty over how long and severe the disruption will be, it is not possible at this point to quantify the impact on either growth or inflation with any degree of precision.

But while we are discussing energy, it is worth noting how India’s energy dynamics have changed in the last few years.

India was and remains a crude oil-deficient but refining-surplus nation. What this means is that while India is a net importer of crude oil, it is a net exporter of refined products. In calendar year 2025, for instance, while India imported 250 million tonnes of crude oil, it exported, on a net basis, 15 million tonnes of petroleum products (imported 50 million tonnes and exported 65 million tonnes).

But both of these balances have worsened over the last decade. This is because while India’s energy demand has increased, domestic production has actually declined. In 2015, India’s domestic crude oil production was 37 million tonnes or 16% of total crude oil consumption (84% was imports). In 2025, however, domestic crude oil production had declined to 28 million tonnes, down 25%, and it now covers just 10% of the domestic crude oil requirement. So 90% of the crude oil is now imported.

And our excess refining capacity has also been whittled away in the last few years. In 2015, India’s exports of petroleum products stood at 59 million tonnes. And in 2025, India’s exports of petroleum products stood at 65 million tonnes, a less than 10% increase. India primarily exports Petrol and Diesel. But imports of petroleum products almost doubled during this period – from 27 million tonnes in 2015 to 50 million tonnes in 2025. And most of these imports are LPG (~45%) and Petroleum Coke (~25%).

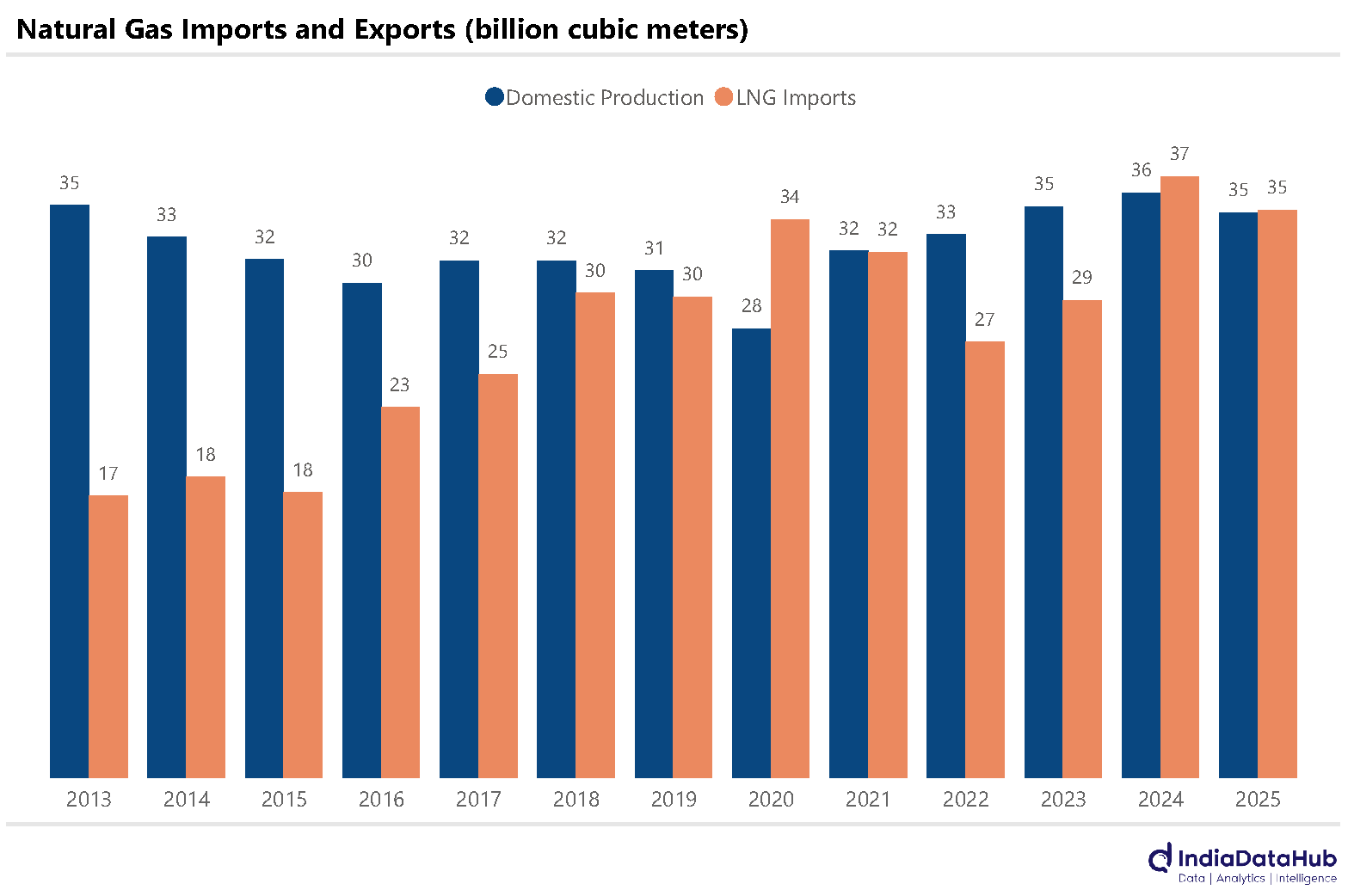

And a similar story has played out in natural gas. Between 2015 and 2025, while consumption of natural gas increased by 40%, domestic production increased by just 10%. Consequently, imports of LNG doubled. And more than 50% of domestic consumption of natural gas is now sourced through imports.

Bottom line, India’s energy balance or petroleum balance has worsened. And thus our vulnerability to sustained dislocation in the global energy market, which was always high, has increased in the last few years. So at this point in time, we can simply watch how things unfold. Fingers crossed…

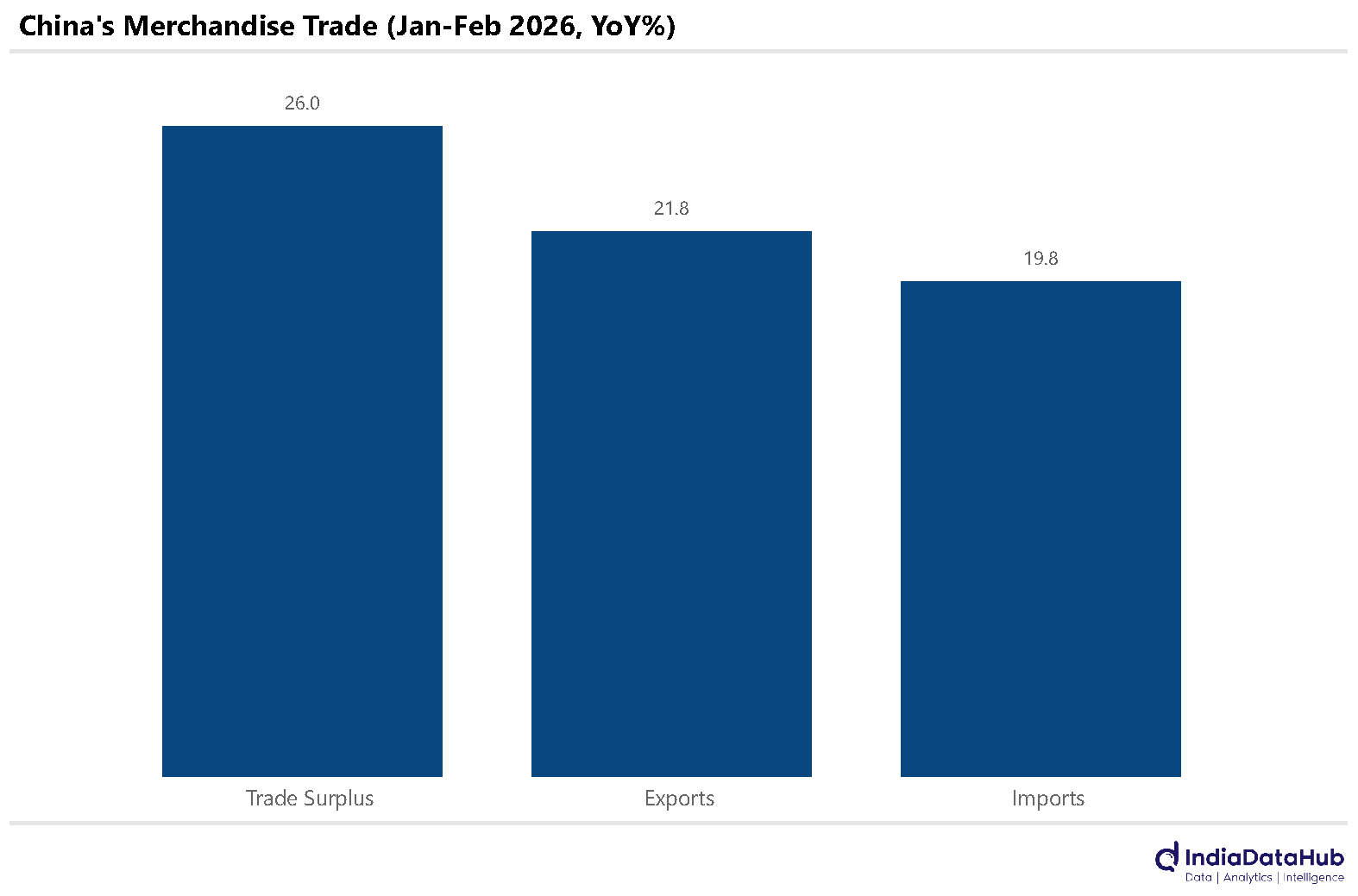

Lastly, China’s foreign trade is off to a strong start in 2026. Merchandise exports in the first two months of the year grew by over 20% YoY while Imports grew ~20% YoY. The trade surplus consequently expanded by over 25% YoY to over US$200bn during this period.

Trade with the United States weakened, with exports down 11% YoY and imports plunging over 25% YoY, reflecting the continued impact of tariffs. By contrast, exports to the European Union grew by over 25% and those to Southeast Asian nations surged by almost 30% YoY. Imports from these regions also rose sharply. Together, the data highlights China’s deepening ties with regional and European markets and underscore China’s ability to diversify trade partnerships and reduce reliance on the US amid ongoing geopolitical tensions.

That’s it for this week, see you next week…