Credit growth uptick, FDI recovery, Corporate tax buoyancy and more...

This Week In Data #159

In this edition of This Week In Data, we discuss:

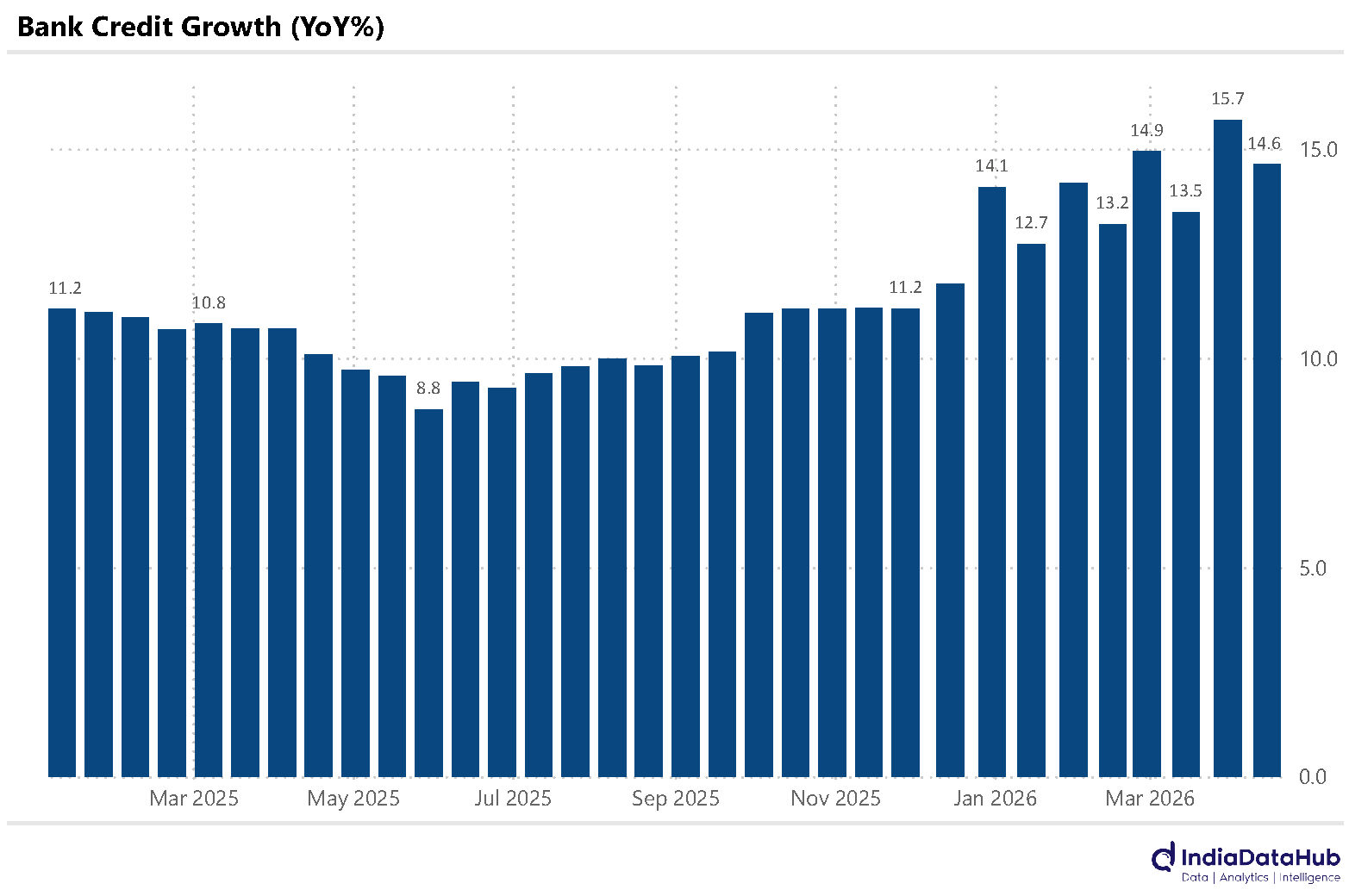

Uptick in credit growth seems for real but is it only inflation?

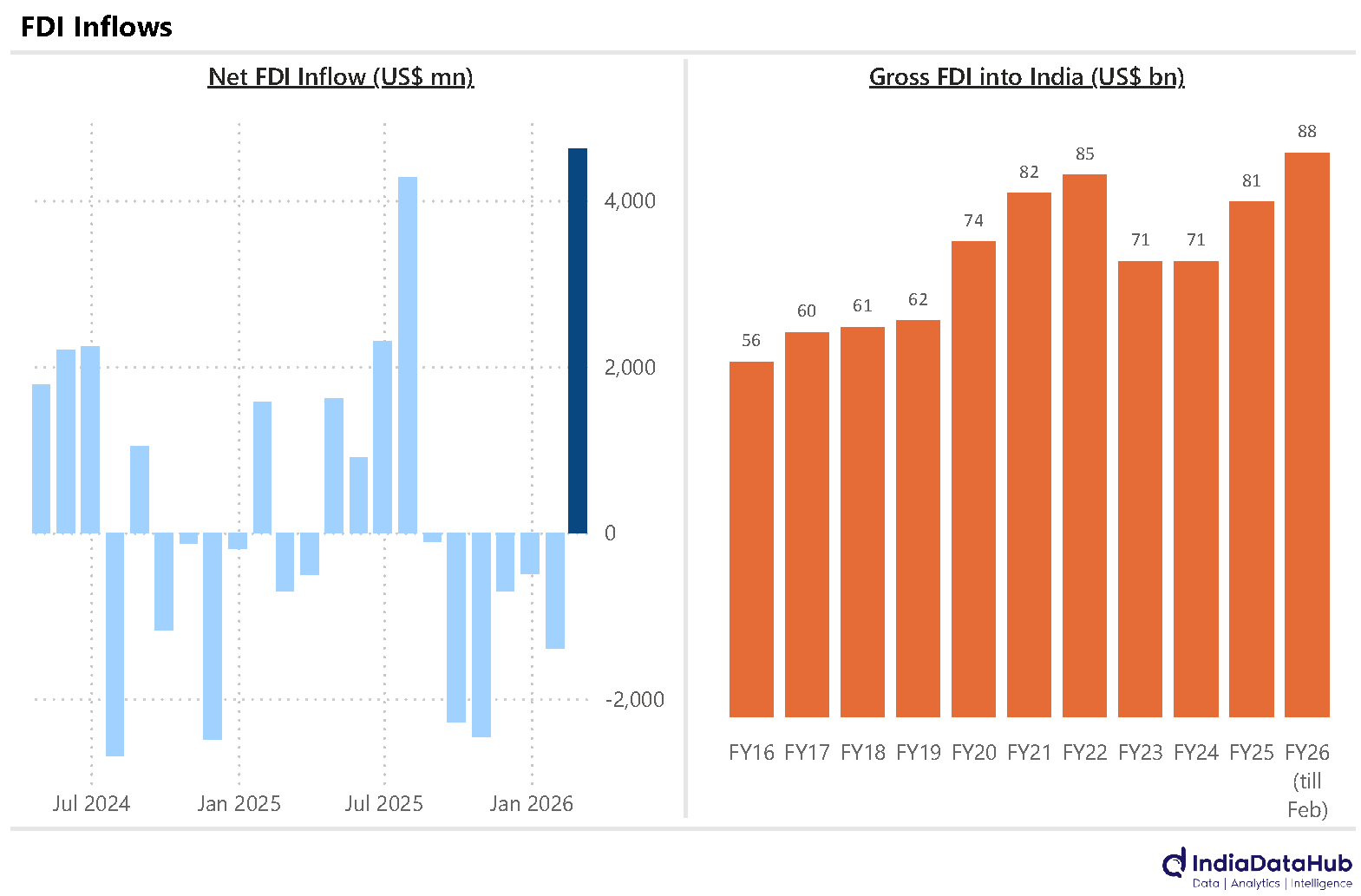

FDI inflows finally turn the corner driven by higher gross inflows

Outward remittances spike in February

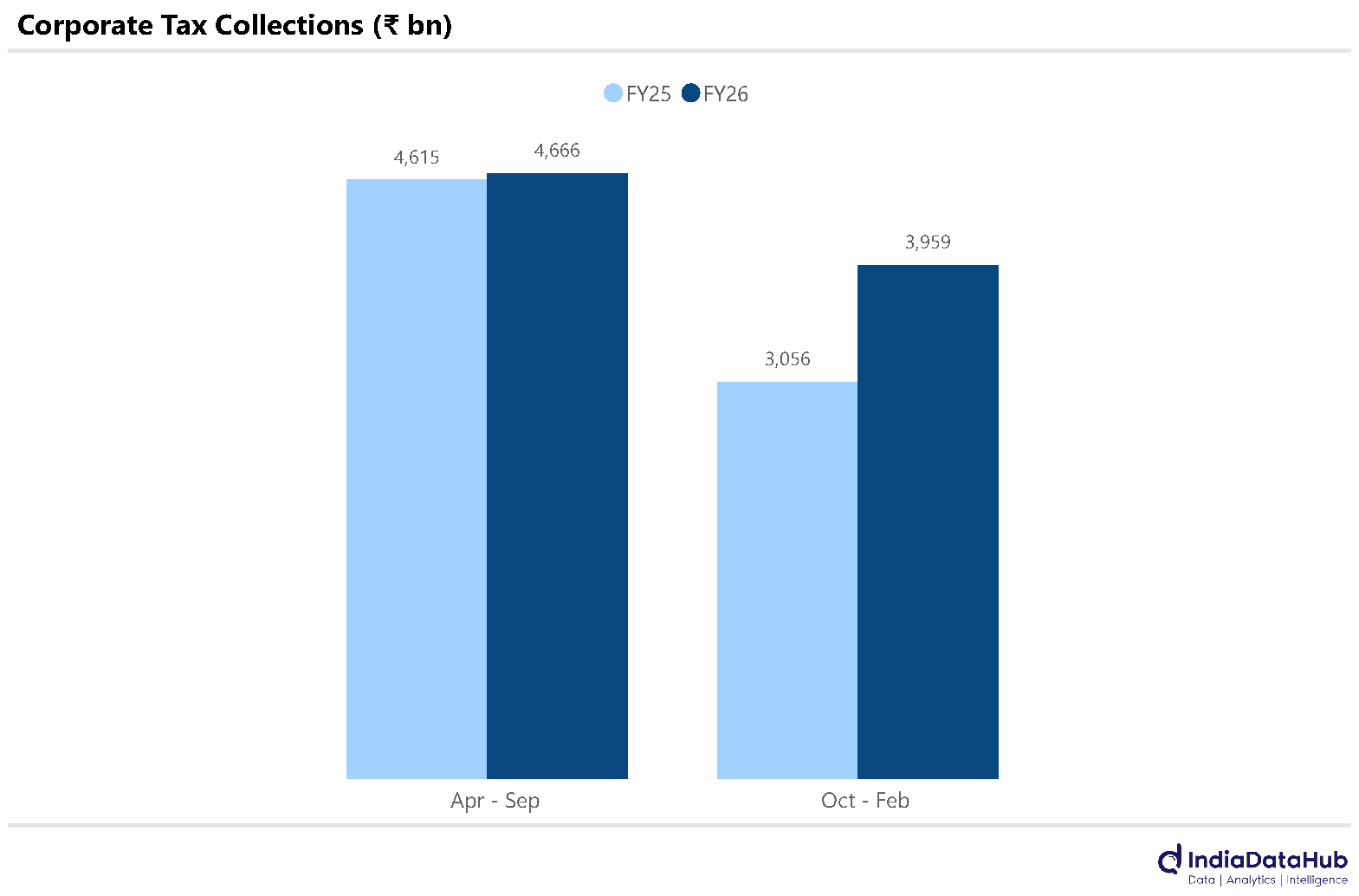

Corporate tax collections are seeing strong growth in 2HFY26

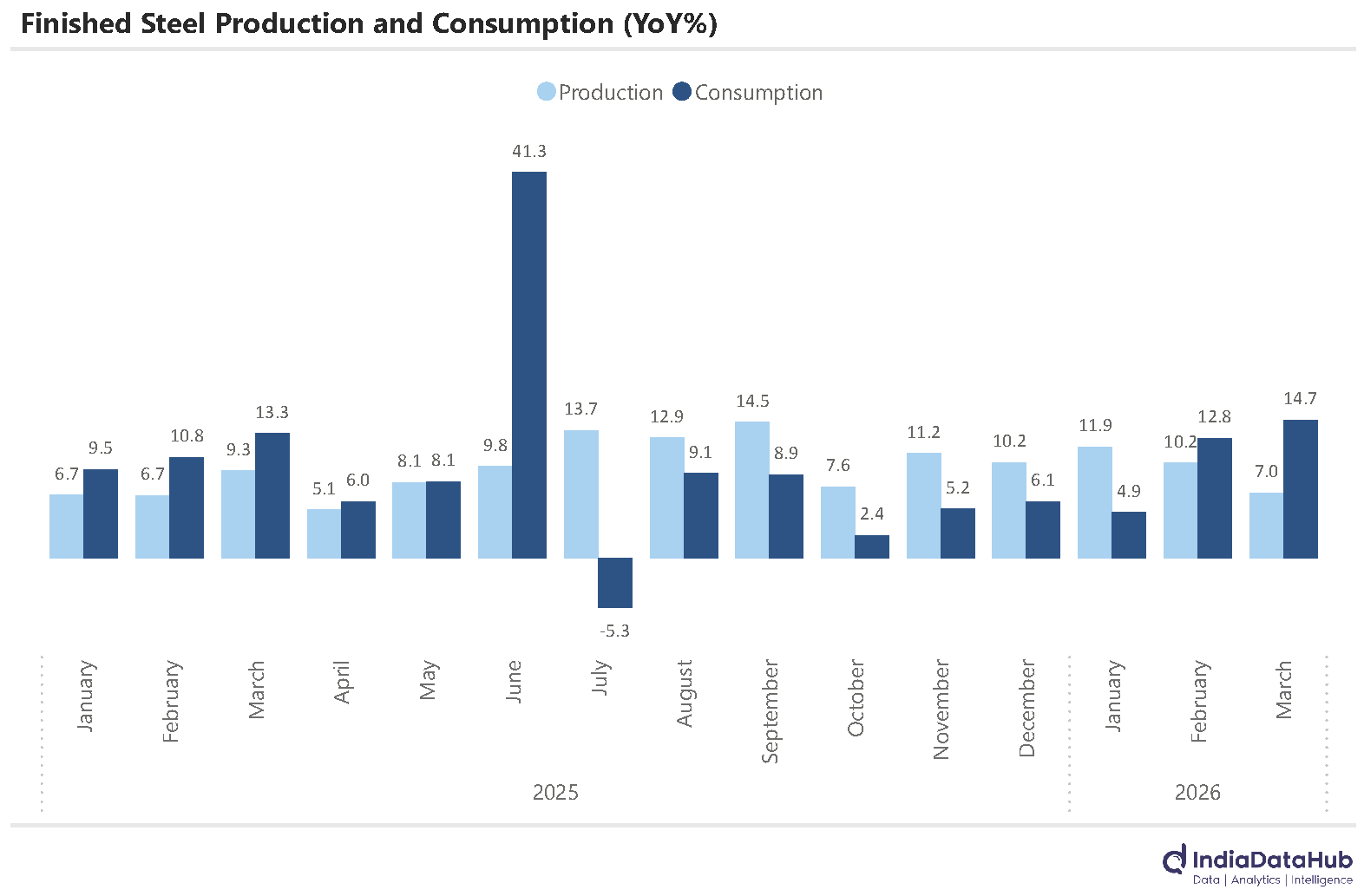

Steel consumption is seeing strong pick up in the last few months

Bank credit growth has indeed picked up in recent months. Our apprehension that the spike in the second fortnight of March was a financial year-end artefact is most likely not the case. While we do not have bank credit data, the money supply data for the first fortnight of April suggests that the banking sector’s credit to the private sector moderated only by 1ppt to a still strong 14.6% YoY. In the last 4 fortnights, this credit growth has averaged ~14.7% YoY as against an average growth of 12.2% since October to early February. And this suggests an uptick in growth. But which growth exactly – real or nominal?

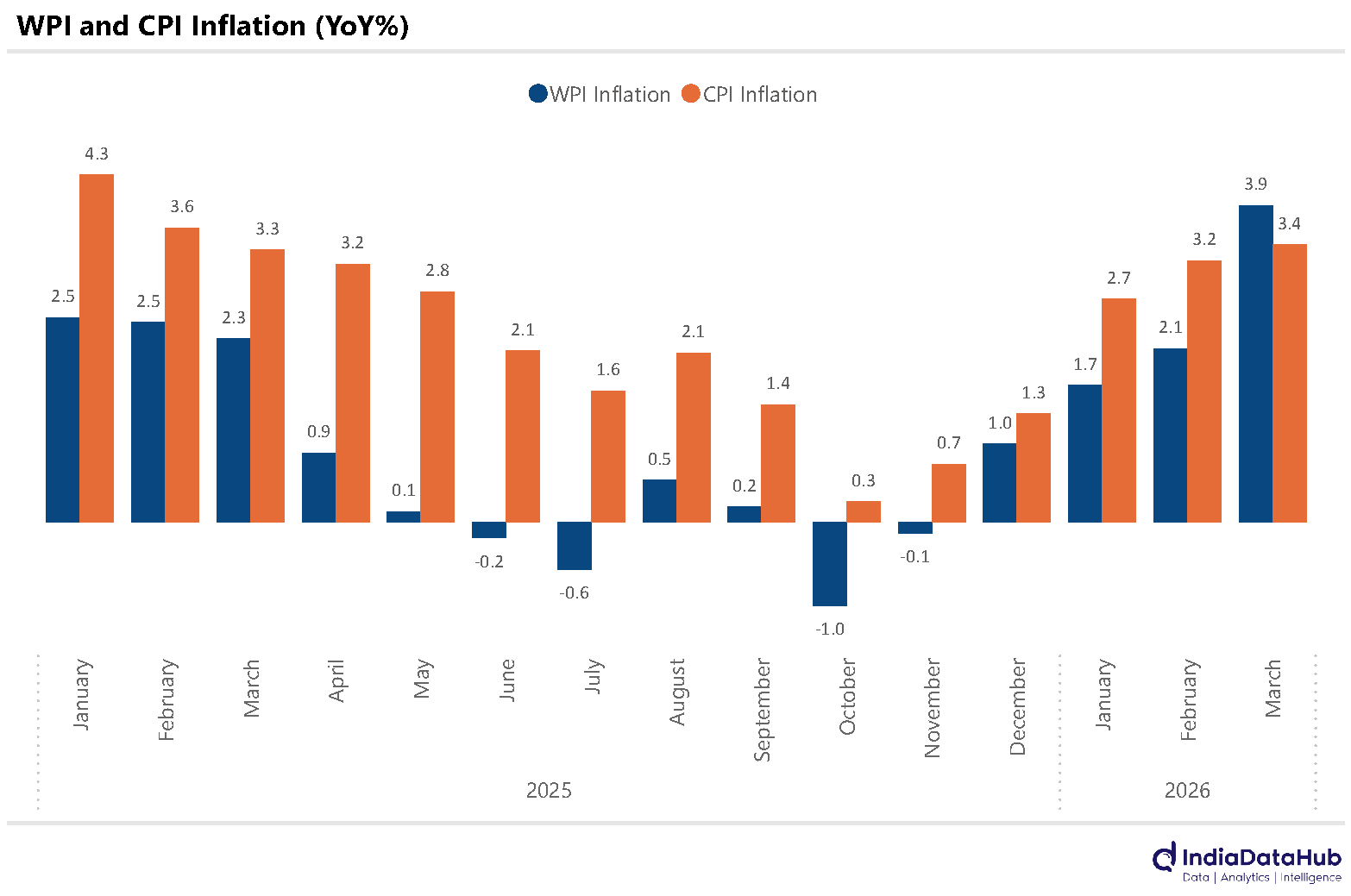

And it looks like most of this uptick might be due to higher inflation. WPI inflation, for example, has ticked up from 0.4% YoY between Oct-Jan to 3% in Feb-Mar. CPI inflation has similarly ticked up from an average of 1.3% YoY between Oct and Jan to 3.3% in Feb-Mar. So inflation has ticked up by 2ppt and so has credit growth. So it does look like there is not much of an uptick in ‘real’ credit growth; it is mostly price driving the uptick in credit growth.

After six consecutive months of outflows, net FDI flow turned positive in February this year. Feb saw a net FDI flow of US$4.6bn, as against a cumulative outflow of US$7.5bn during the preceding six months. The turnaround was driven by a sharp increase in inward FDI to US$9bn, the highest since July last year. Repatriation of existing FDI also declined to a multi-year low of US$1.7bn.

Overall, FY26 is turning out to be a strong year for FDI with YTD (till Feb) gross inward FDI already 10% above full year FY25 levels and also above the all-time gross FDI inflows of US$85bn in FY22. With even a modest growth, FY27 will see gross FDI cross US$100bn.

Outward remittances under the RBI’s LRS surged in February. On a YoY basis, they rose almost 20% to US$2.3bn. Travel continues to be the key driver of remittances, and it also saw 20% growth in February. And on a low base, outward remittances for financial investments overseas increased 50% YoY in February following a strong 70% growth in January.

A sign of improving corporate profitability is the sharp recovery in corporate tax collections in the second half of FY26. Between April and September, net corporate tax collections saw a modest 1% YoY growth. However, as of February, the growth rate has picked up to 12% YoY, implying an almost 30% YoY growth between October and February. The last 3 months (Dec-Feb) have also seen over 20% growth in collections.

Lastly, finished steel production growth moderated to a 11-month low of 7% YoY in March. However, on a full-year basis, production expanded by 10% in FY26, significantly higher than the 6% growth in FY25. Part of this is due to lower imports. Finished steel imports declined by 10% YoY in March, marking the 12th consecutive month of contraction. For FY26, imports fell sharply by 33% YoY, to multi-year lows. And consumption also is accelerating with a 9-month high growth of 15% in March following on the 13% growth in February. A sign of recovery in the construction sector?

That’s it for this week. See you next week…