Declining Exports, Uptick in CPI, Higher credit growth, and more...

This Week In Data #158

In this edition of This Week In Data we discuss:

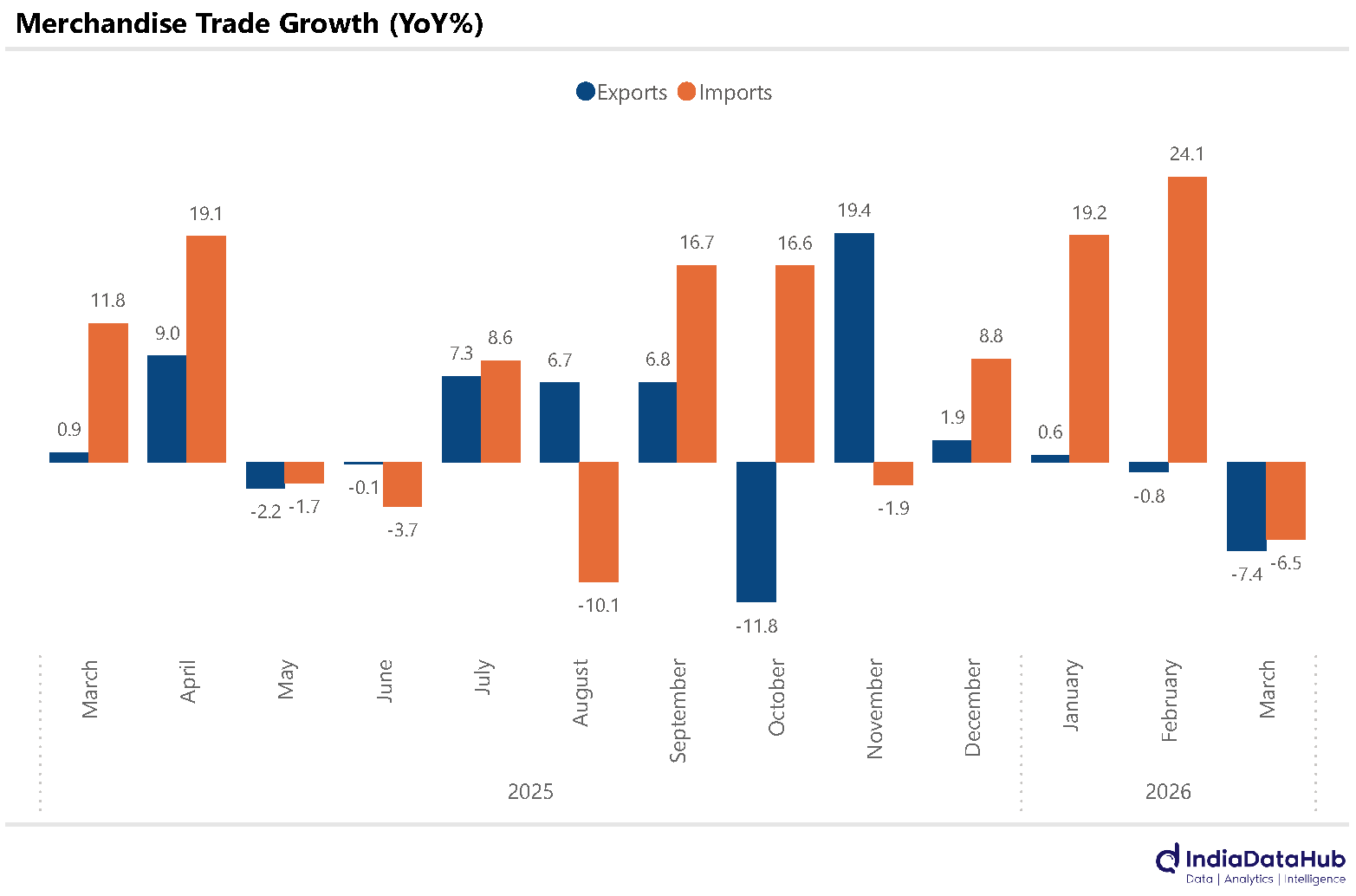

Exports and Imports see sharp decline in March driven by different sectors

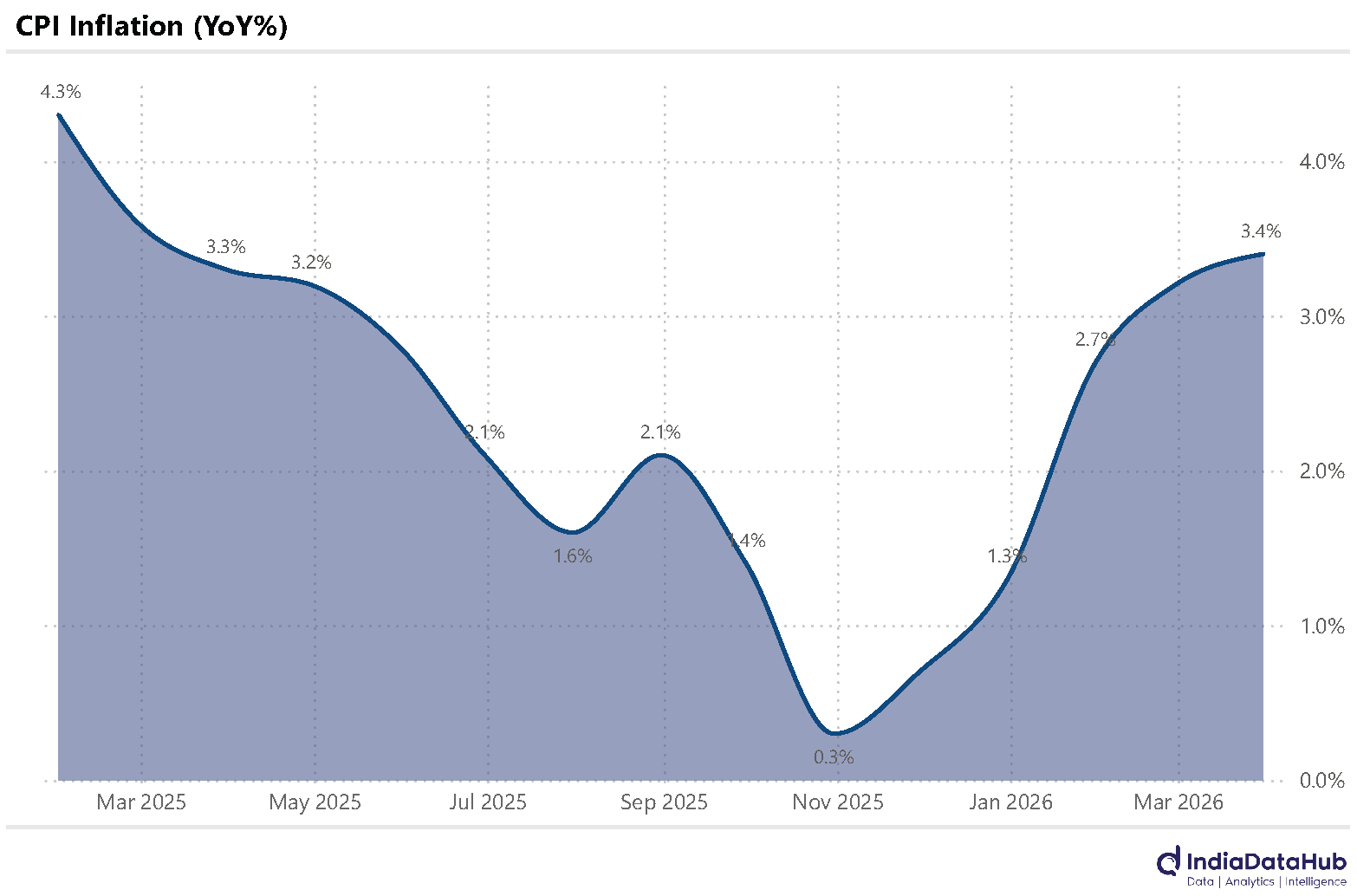

Inflation continues to edge up, driven largely by Food

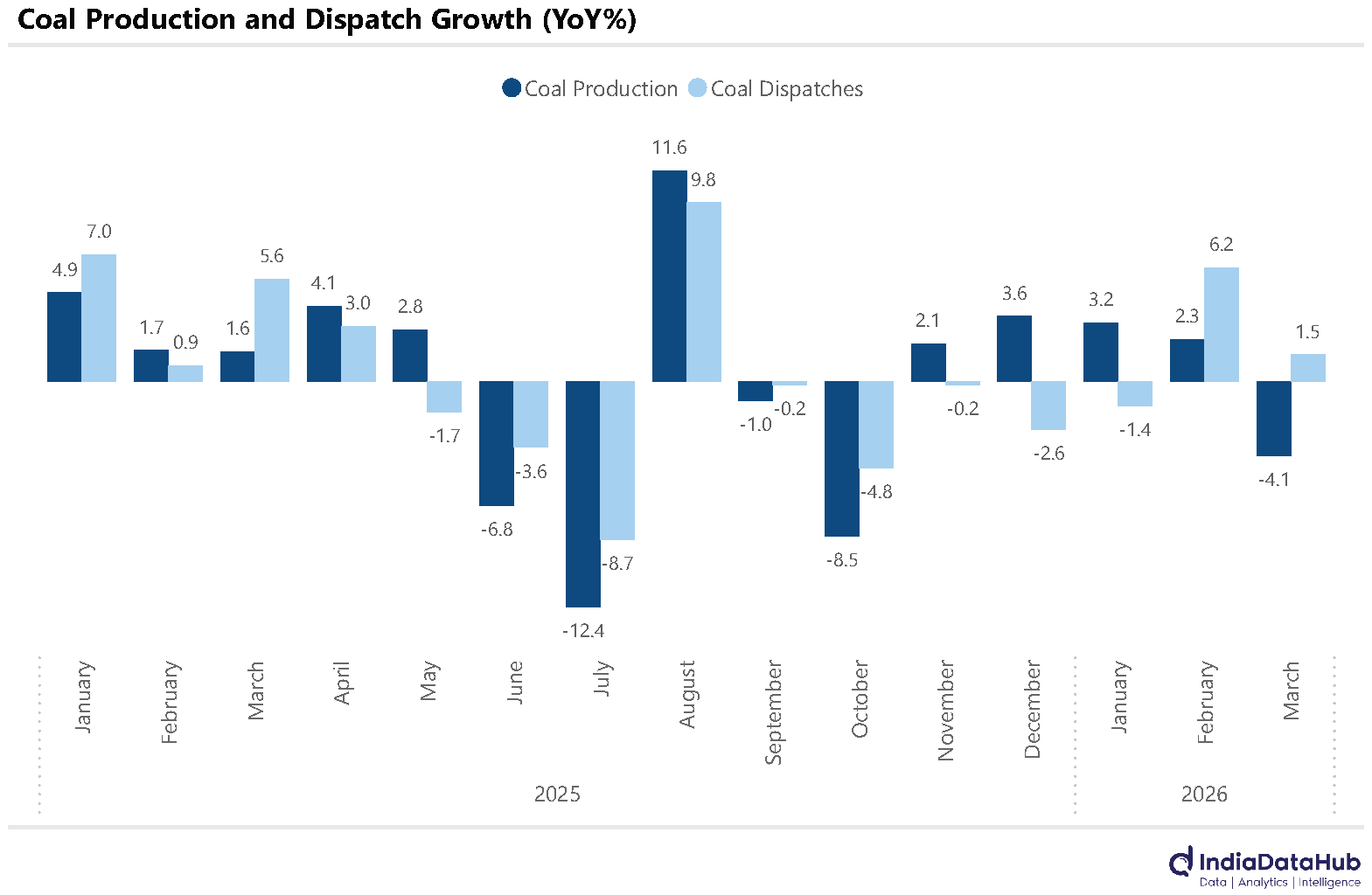

Coal production declines in March, first time in 4 mths, dispatches also remain soft

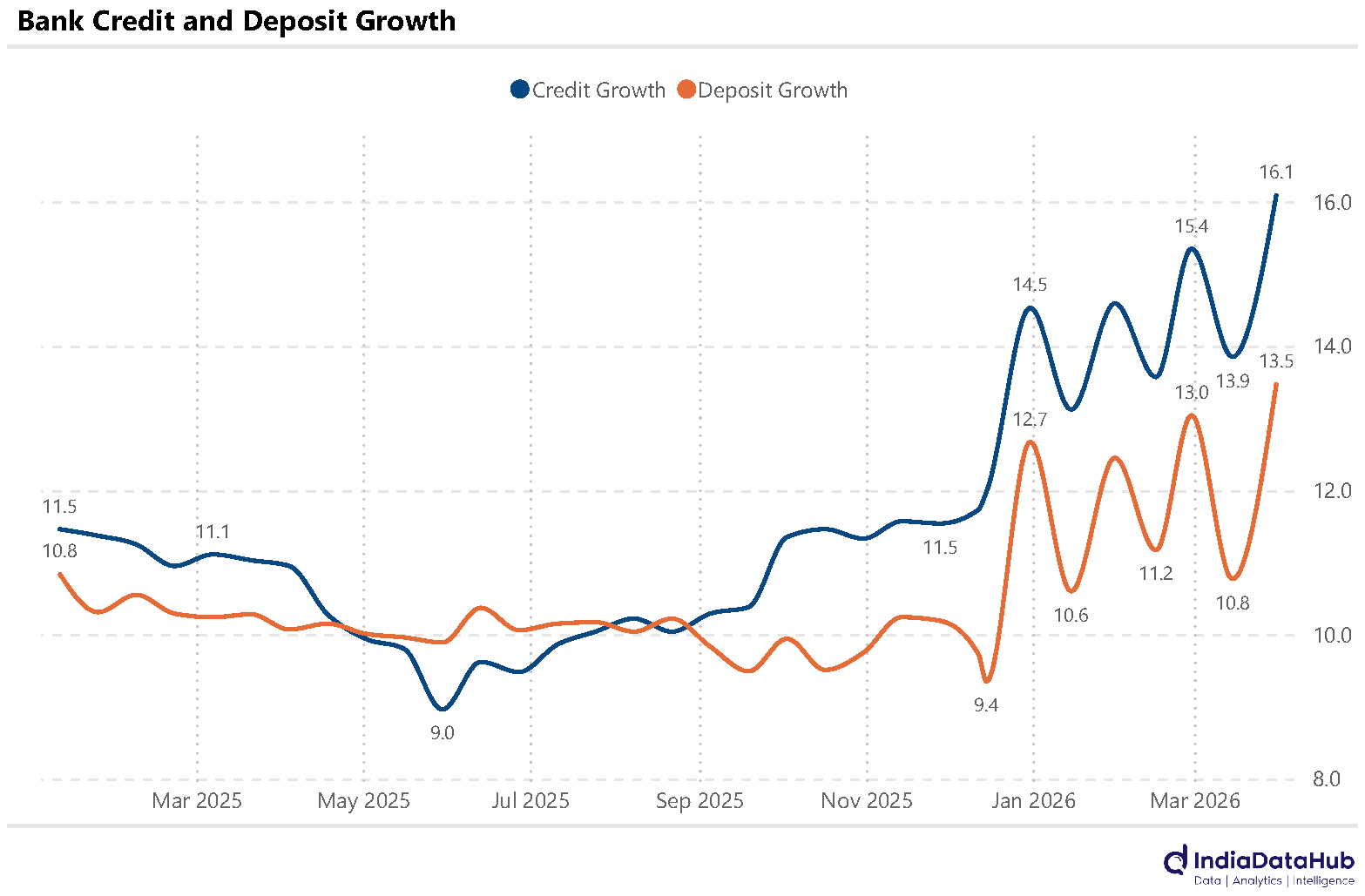

Bank credit and deposit growth accelerate in March but uptick could be spurious

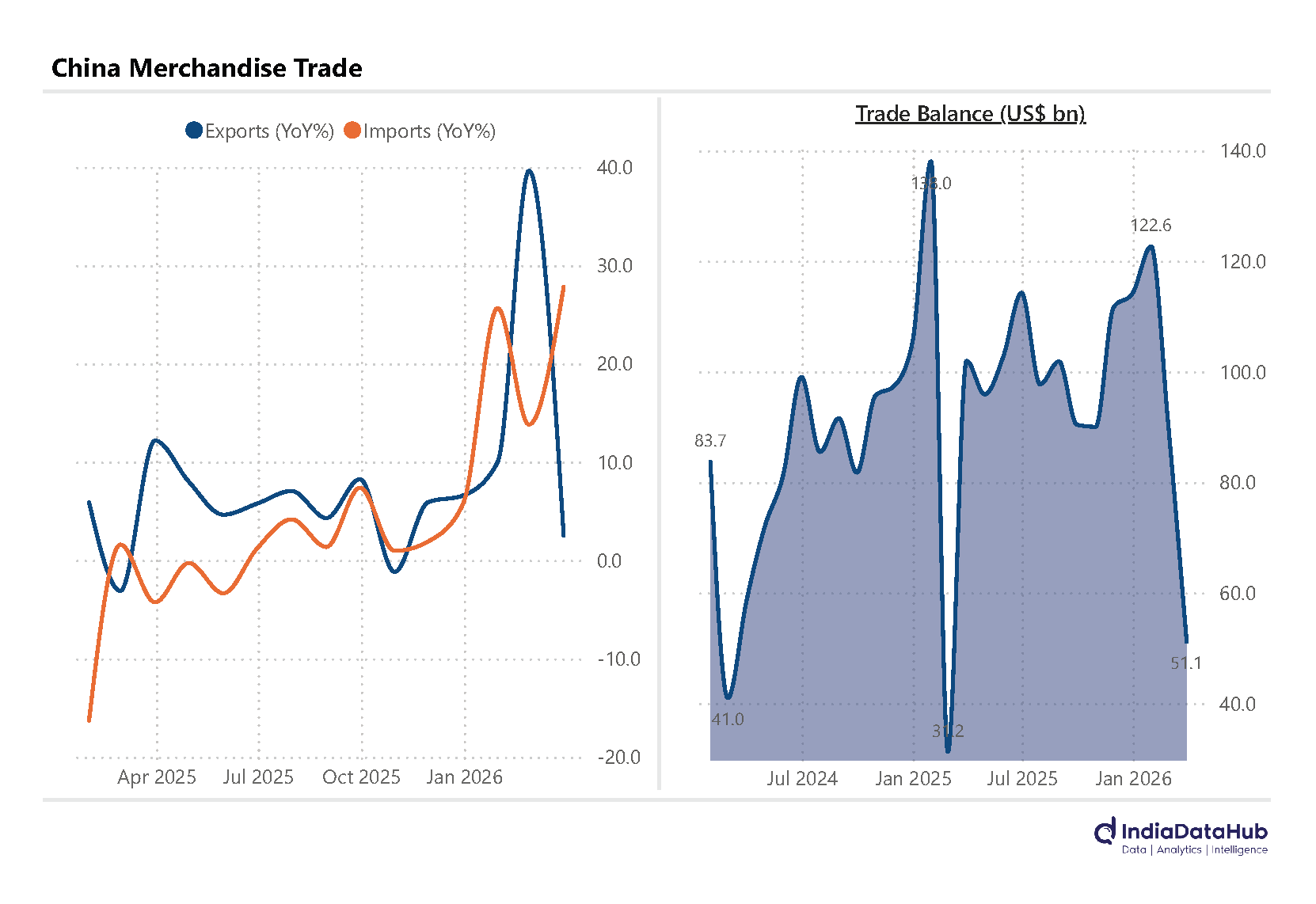

China’s trade surplus falls sharply in March as imports surge

Exports decreased 7% YoY in March, driven by over 20% decline in Gems & Jewellery and Pharmaceuticals exports and ~15% decline in Textiles exports. Electronics goods exports also declined in March. Petroleum goods were the sole exception, with exports growing 6% YoY – mostly reflecting higher prices rather than higher volumes.

Imports also declined by almost 7% YoY. But this was driven by an over 35% decline in Petroleum imports (despite the higher prices). Excluding Petroleum, imports rose 6% YoY with Machinery and Electronic goods imports seeing ~20% YoY growth in imports. Gold is the other category that saw a sharp decline in imports.

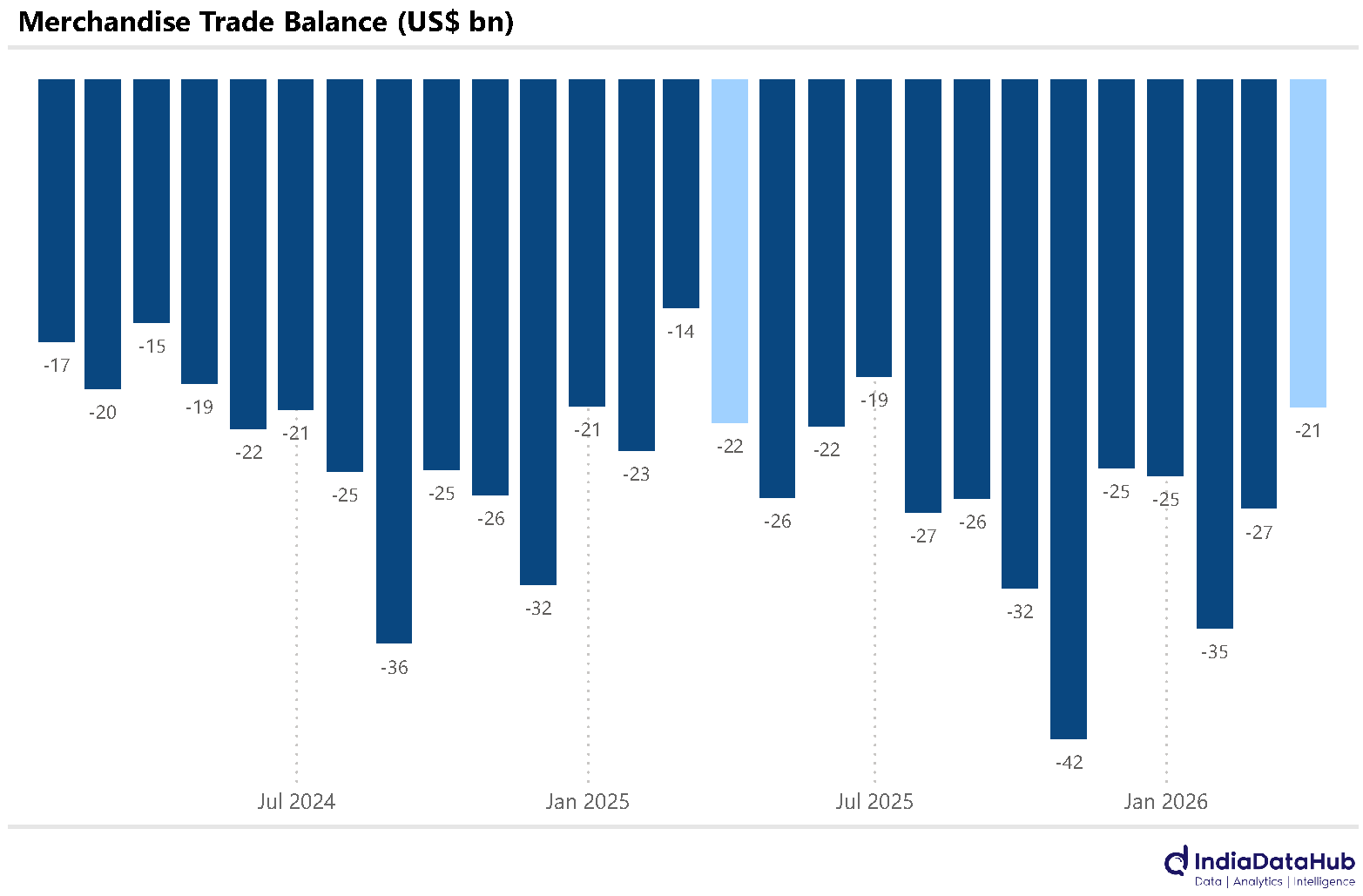

The sharp decline in both exports and imports meant that the trade deficit declined modestly on a YoY basis and at just under US$21bn, it was the lowest since June in absolute terms.

CPI Inflation continued to tick up, rising to 3.4% YoY in March from 3.2% in February and 2.7% in January. Food inflation continues to be the key driver of this uptick having risen from 2.1% in January to 3.7% in March. So core inflation remains modest at close to 3%. More importantly, this level is broadly the same as last year and so it is not base effect which is keeping inflation low.

Oil continues to be the wild card. So far, the Oil marketing companies have absorbed the impact of higher oil prices, especially the retail fuels. But it remains unclear if and when Oil prices return to the levels they were at a couple of months back. And until that happens, there remains material upside risk to inflation. In the last monetary policy meeting, the RBI’s projections were for inflation to rise closer to 5% in the next few months. This means that any discussion around interest rate cuts is, at least for now, off the table.

Domestic coal production growth declined by 4.1% YoY in March, the first decline in the last 4 months. On the demand side while coal dispatch growth was positive, it was subdued at less than 2% YoY. Sectoral trends suggest weakness in industrial sector demand: dispatches to the sponge iron sector declined 34% YoY, marking the 11th consecutive month of contraction.

On an annual basis, sponge iron demand fell sharply in FY26. Meanwhile, dispatches to the power sector declined ~4% YoY in FY26, aligning with moderation in thermal power generation growth to ~4% in FY26, compared to a higher growth rate in the previous year, indicating relatively softer coal-based power demand.

Lastly, bank credit growth has accelerated sharply to over 16% at the end of March from just over 13% at the start of the year. Deposit growth has similarly accelerated by ~3ppt and is now running at over 13%. Both credit and deposit growth are currently at the highest rate in the last few years.

Some of this is a year-end effect, as last year the data is not exactly as of 31st March due to the change in the definition of fortnight. So once mid-April data is available, we will better know if there is a real pick up in monetary data or just a year-end artefact.

China’s merchandise exports grew just 2.5% YoY in March 2026, down from 12.2% in March 2025 and marking a five‑month low. Imports, however, surged 27.8% YoY, reversing last year’s 4.3% decline. With imports rising much faster than exports, China’s merchandise trade surplus narrowed to $ 51.13 billion.

Trade with the U.S. remained weak: exports to the U.S. fell 26.5% YoY, while imports from the U.S. rose 2.1% YoY, ending a year‑long decline. As a result, China’s bilateral goods trade surplus with the US narrowed to $16.8 billion — its lowest level since March 2025.

That’s it for this week. See you next week…