Declining FDI, Strong ECBs, Higher outward remittances and more...

This Week In Data #40

In this edition of This Week In Data, we cover:

The continued decline in FDI in India

Continued high outward remittances from India

Strong external commercial borrowings this year

Decline in FX Reserves and RBI’s defense of the rupee

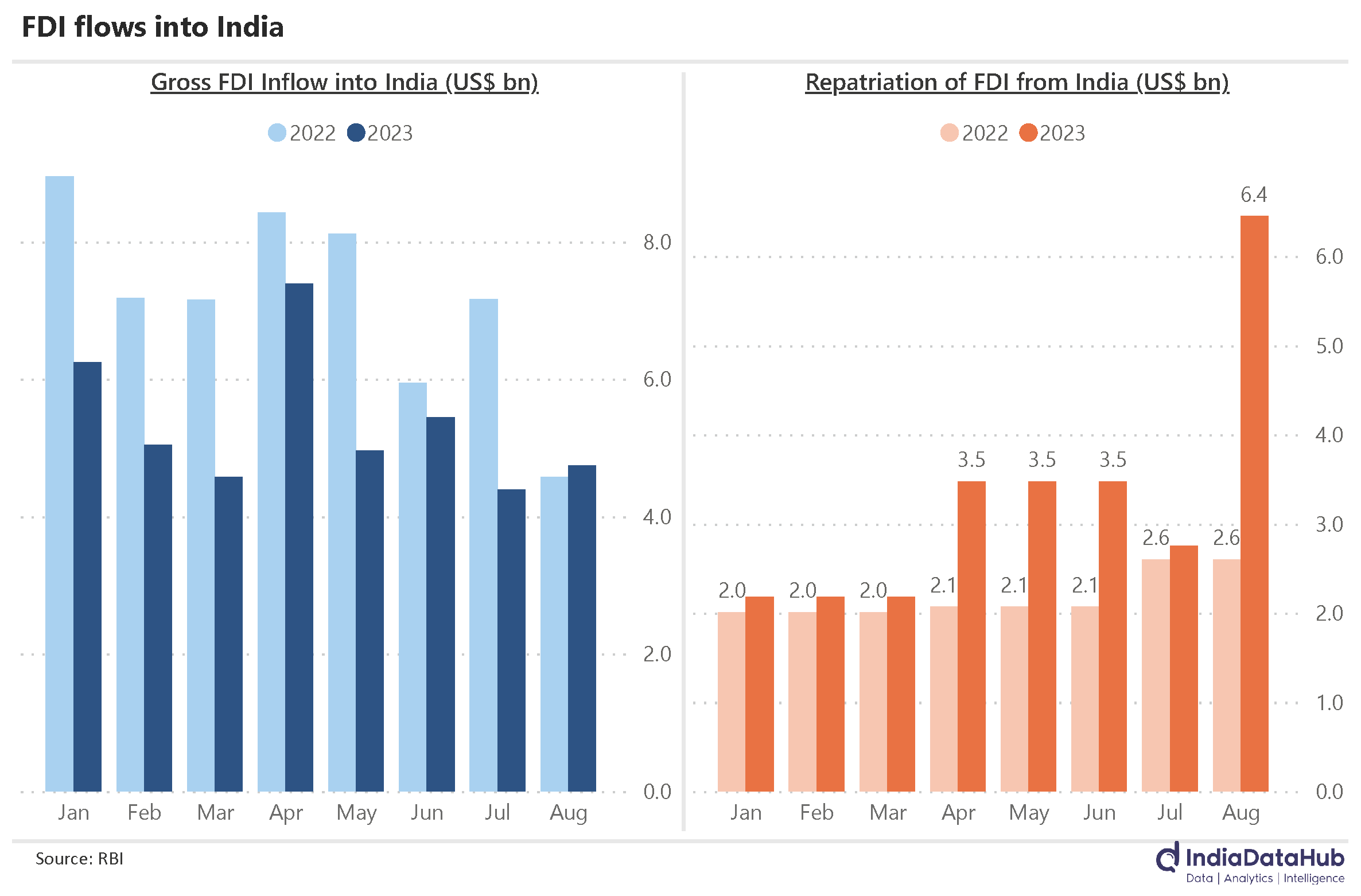

The first newsletter after mid-month means we must talk about FDI. And the bad news continues. August saw a negative net FDI of US$1.7bn. This means money went out of India rather than it came in. In 12 of the last 13 months, FDI received by India has declined on a YoY basis. But this trend of decline is not just that of the last 12 months, it is a few years old now. The peak FDI received by India was US$70bn during the 12 months ending June 2021. During the latest 12-month period, India received just US$26bn of FDI. That’s a decline of more than 60%. Given this sharp decline in FDI even as the overall economic activity as well as the broader investment sentiment in India remains buoyant suggests that a large part of this decline has to be attributable to the decline in PE/VC activity.

The problem in August was not so much the gross FDI received by India. It grew by over 20% YoY after seven consecutive months of a decline. The problem was the big increase in repatriation of FDI from India (existing FDI investors taking out money from India). August saw almost US$6.5bn being repatriated from India, almost a 150% increase on a YoY basis. This was also the highest monthly repatriation on record.

And this is also the silver lining. FDI inflow is starting to grow, and repatriation tends to be a lumpy number. Thus, it is quite likely that August is probably the worst FDI print we will see for some time and from September onwards the numbers will likely trend up. Fingers crossed…

August was also a strong month for outward remittances under the RBI’s LRS. It was only the second month when outflows crossed US$3bn – the other being June this year. Effectively, as the date for the higher TCS regime draws closer, outflows under LRS have accelerated.

And it is not just the ultra HNI’s parking money outside. August saw almost US$2bn being remitted for overseas travel – the highest ever. The last 3 months have seen almost US$5bn being remitted under the heading overseas travel. These are not busy months for overseas travel for Indians. October-November is the busy season for travel with Diwali vacations for schools. So, it is quite likely that people are booking overseas holidays in advance. In comparison, overseas investments continue to be a relatively small sum for remittances – just under US$1bn in the last 3 months, up 2x over the past year. Equally, resident Indians have suddenly seen a big increase in gifting. They have remitted over US$1.1bn abroad as ‘Gifts’, an increase of almost 75% over the same period last year.

YTD so far, the outward remittances under the LRS have totalled US$15bn, 40% higher on a YoY basis. The annual limit under the LRS is US$250k per person. If we assume that the average remittance per person is US$150k, that means that almost 100,000 resident Indians have already used the LRS window! For reference, only 130k individuals reported a taxable annual income of over ₹10m (~US$125k) in the most recent year for which we have data (assessment year 2021-22). Of course, the LRS can be out of stock of wealth and not just annual income. But the comparison is stark. And the average is likely to be lower because the tail will be very long – thousands of people will be spending a few thousand dollars on a short 4–5 day overseas vacation.

FY24 is turning out to be a good year for overseas borrowings, despite higher global rates and the narrowing of the rate differential with domestic rates. In the first 5 months of this year, the RBI has authorised US$26bn worth of ECBs. This is the same as the amount RBI authorised in the full year FY23! The manufacturing sector has been the biggest borrower with authorisations totalling to US$12bn (almost half) so far. Telecom is the next big sector with US$6bn worth of authorisations and NBFCs have seen almost US$5bn worth of authorisations.

Since mid-July, India’s FX reserves have declined by almost US$25bn and given the resilience of the rupee in the face of global dollar strength, it is not surprising that a fair amount of this decline is due to RBI’s FX intervention rather than just valuation loss. In August, for which data was released this week, the decline in FX reserves was almost US$5bn and of this almost US$3.9bn or 80% was due to FX intervention by the RBI.

Since August (and through mid-October), the FX reserves have declined by US$13bn and extrapolating the data for August suggests that the RBI has in the last few weeks spent an additional almost US$9-10bn to defend the rupee. As we wrote here, the rupee’s exchange rate relative to the CNY is a key variable for inflation and thus this intervention from the RBI is mostly a reflection of its inflation mandate (and having to prevent further rate hikes) rather than a defence of the rupee per se.

That’s it for this week. The men in blue play the black caps tomorrow in what is perhaps the biggest challenge for both the teams of this tournament. Here’s hoping for a Virat win…