Exports recover, Oil imports decline and Price pressures build up...

This Week In Data #162

In this edition of This Week In Data, we discuss:

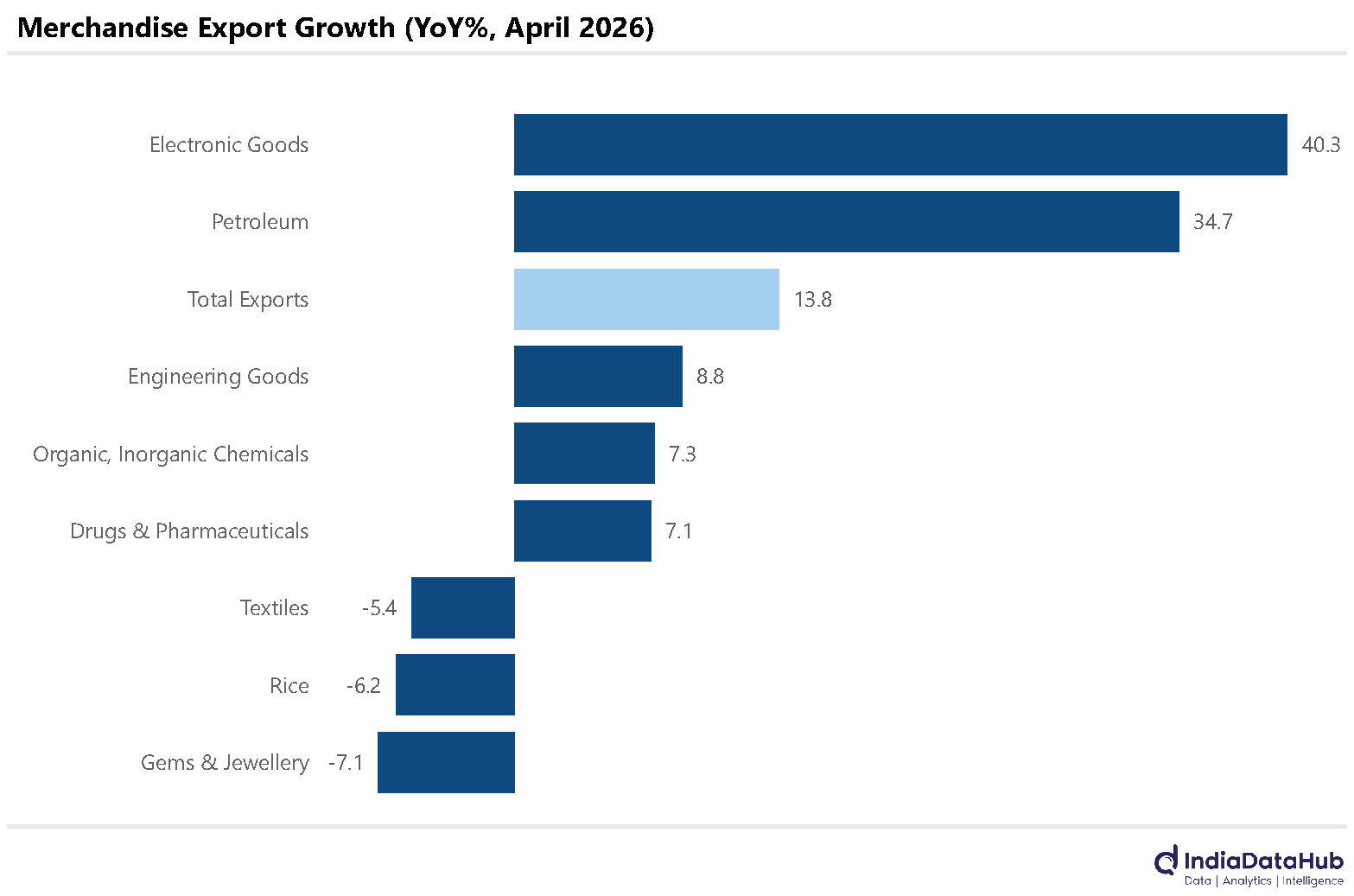

Exports recover in April driven by Electronics and Petroleum

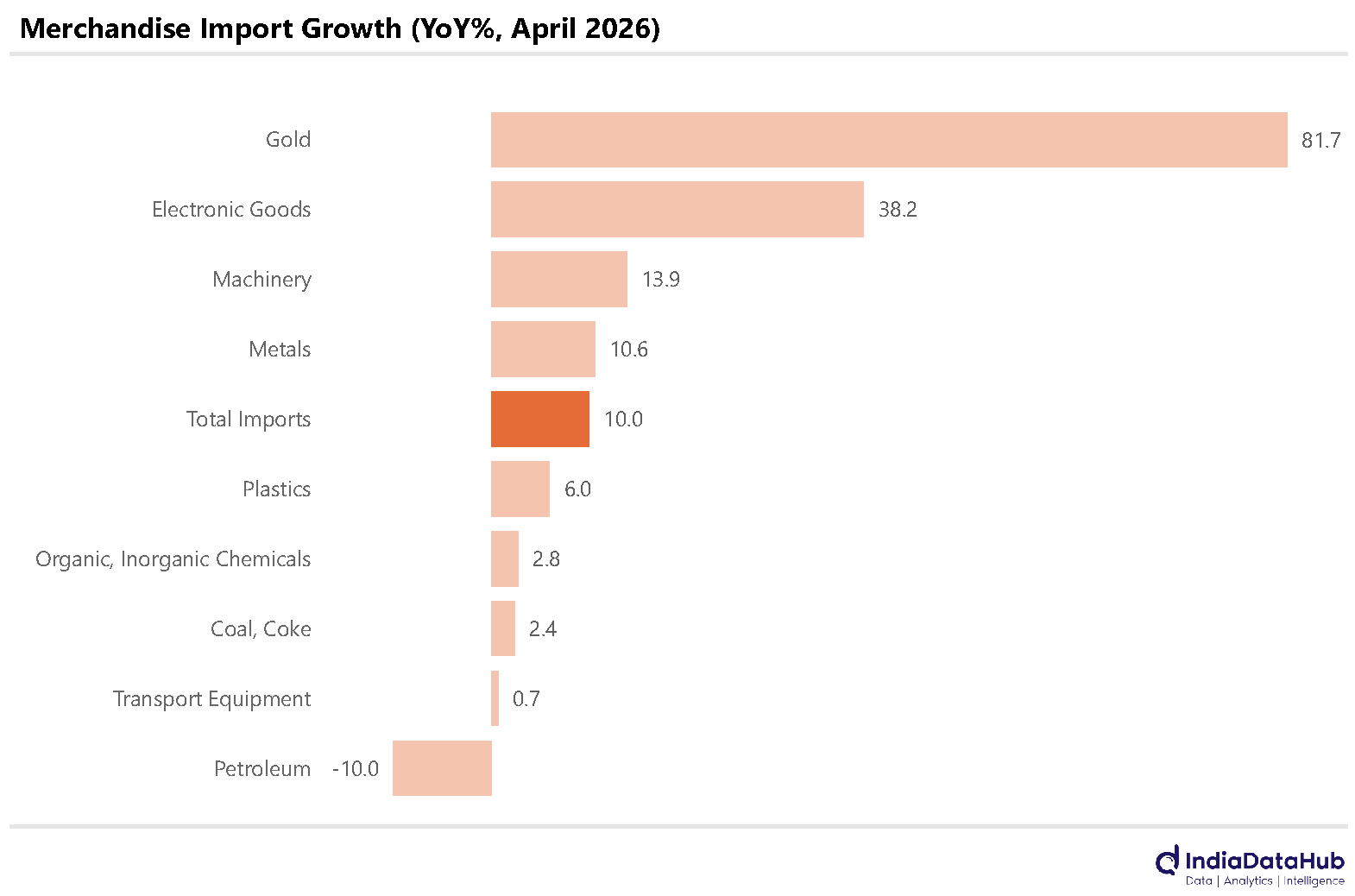

Imports surprisingly see only modest growth as Oil imports decline

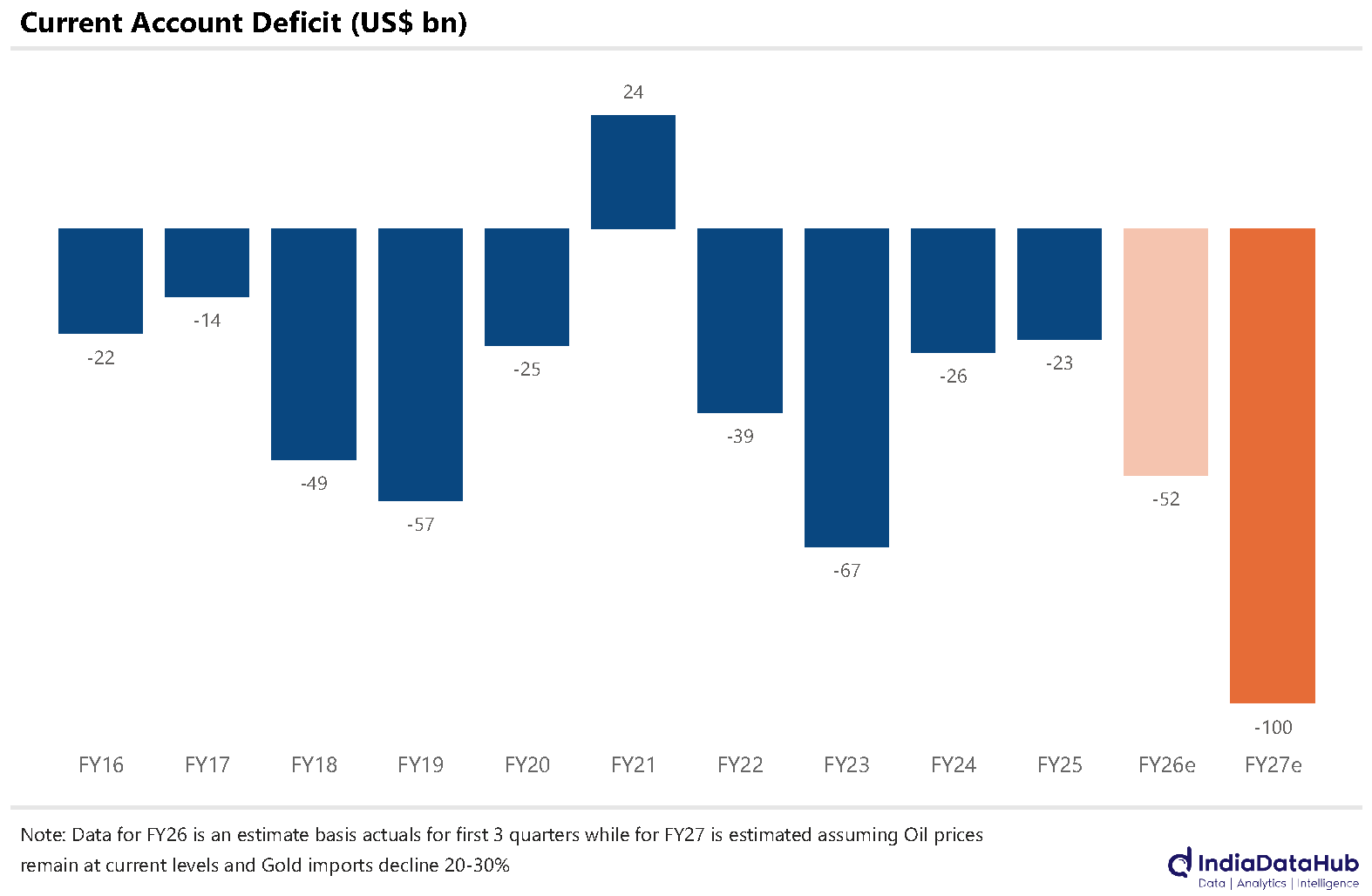

Current account deficit likely to touch US$100bn this year

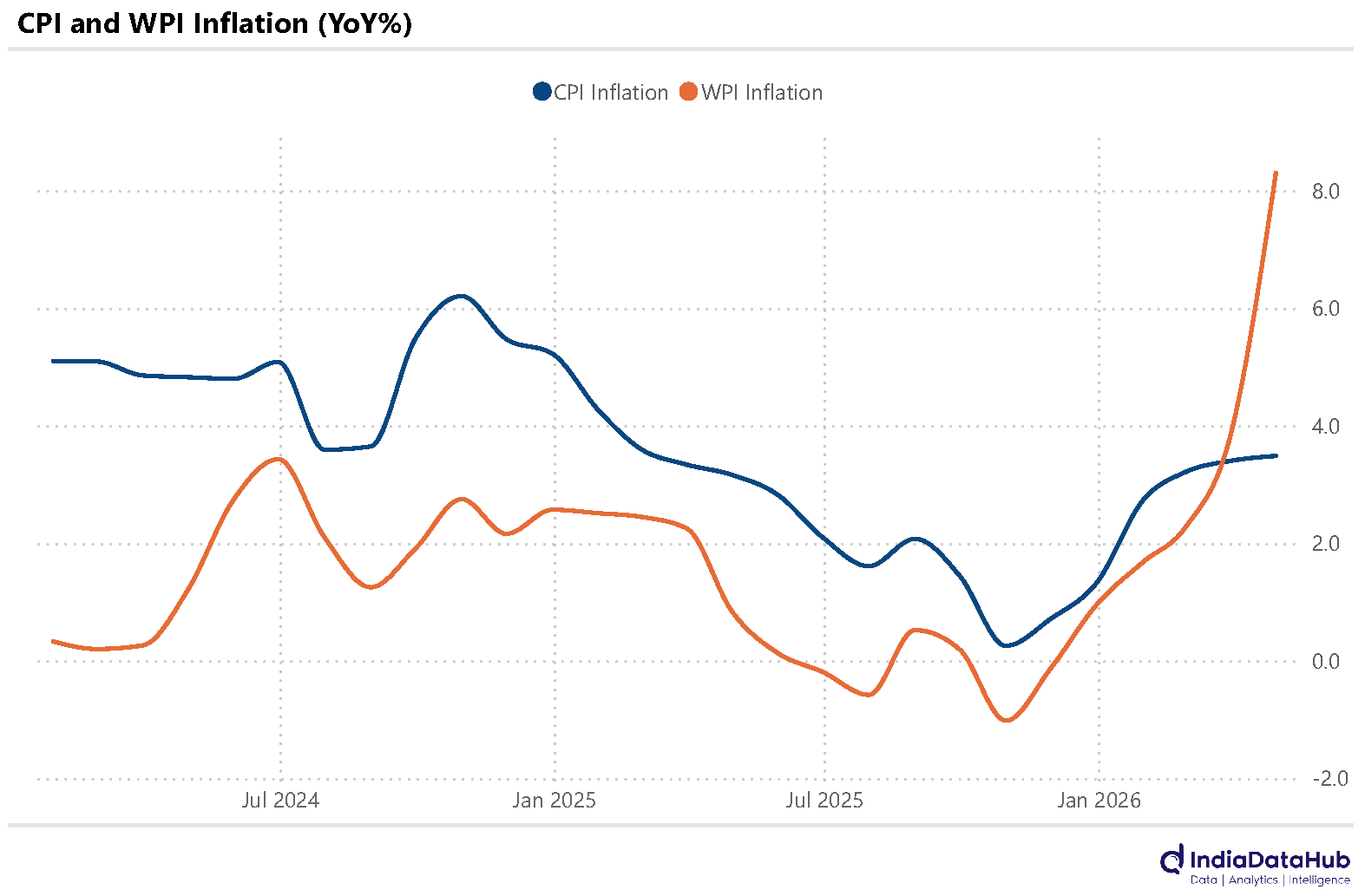

CPI remains soft but WPI rises sharply suggesting build up of price pressures

India’s exports rebounded in April, growing 14% YoY, according to provisional data. This is the highest growth since November last year. The uptick was driven by a sharp 40% growth in electronics exports and a 35% growth in petroleum exports (largely reflecting the higher price, but prices have risen more than rise in exports). At just over US$5bn, electronic exports are now the third largest component of exports after engineering goods and petroleum products, both of which contributed ~US$10bn to exports in April.

Imports, in contrast, rose just 10% YoY, and what was most noteworthy was that despite the sharply higher oil prices on a YoY basis, Oil imports declined 10% YoY in April. This is quite counterintuitive and suggests difficulty in sourcing crude Oil and products (sharply lower volume of imports), rather than lower domestic demand. On the flipside, electronic imports spiked 38% YoY while gold imports rose 80% YoY. At US$5.6bn, Gold imports in April were the third highest category after Oil and Electronic goods. Gold imports in April were higher than machinery, metal, or Chemicals imports. This possibly explains the recent increase in import duty on Gold.

The April trade data is thus not representative of how FY27 will evolve, if Oil prices remain elevated. As we discussed last week, assuming Oil prices remain at current levels, oil imports on a net basis will likely increase by ~US$70bn on a YoY basis or ~1.7% of GDP.

India’s current account deficit for FY26 is likely to have been ~US$50-55bn, and even if Gold imports drop by 20-30%, we are looking at a current account deficit of over US$100bn for the full year FY27 if oil prices stay at current levels.

And with FPI flows negative, NRI deposit inflows down to a trickle, and FDI still sluggish, there is likely to be a big shortfall on the capital flows side to fund this deficit. So as things stand now, FY27 is likely to be the second consecutive year and the third year in the last 4 to see a balance of payments deficit. This means a further drawdown of reserves, on top of what happened last year (FY26), but was masked by revaluation gains on Gold. And it also means continued pressure on the rupee. Which is again something we have been seeing for the last few months.

But of course, a lot can change in the next few weeks and months. The war in the Middle East might end, and Oil prices can drop to ~US$60-70/bbl. Gold price can also fall. And India benefits – pressure on the rupee eases, sentiment turns around, and FPI flows come back, liquidity improves, inflation pressure comes down, and things cascade the other way round.

The other big data release last week was the CPI inflation. And it remained steady at 3.5% YoY in April, up ~10bps over March. Food inflation continues to run higher, at 4% in April, and thus the non-food CPI is closer to 3%. But price pressures are building. The sharp rise in WPI shows that higher global oil prices are starting to get transmitted to domestic markets despite the retail fuel prices having remained unchanged through April and till last week, when they saw only a modest increase.

The IMD has also forecasted lower than normal monsoon rains this year. And this means that when the RBI meets next in early June, the discussion surrounding monetary policy will change from rate cuts to whether rate hikes are likely. Rate hikes are not imminent, but they are now very much in the air.

And on this somber note, let’s call it a day. See you next week…