Falling CPI, Rising Imports, Record Trade Deficit, RBI Intervention and more...

This Week In Data #43

In this edition of This Week In Data, we discuss:

The fall in October CPI and implications for interest rates

The rise in October Imports and all-time high trade deficit

The increase in risk weightage on some consumer loans by RBI

The fall in US and UK CPI in October

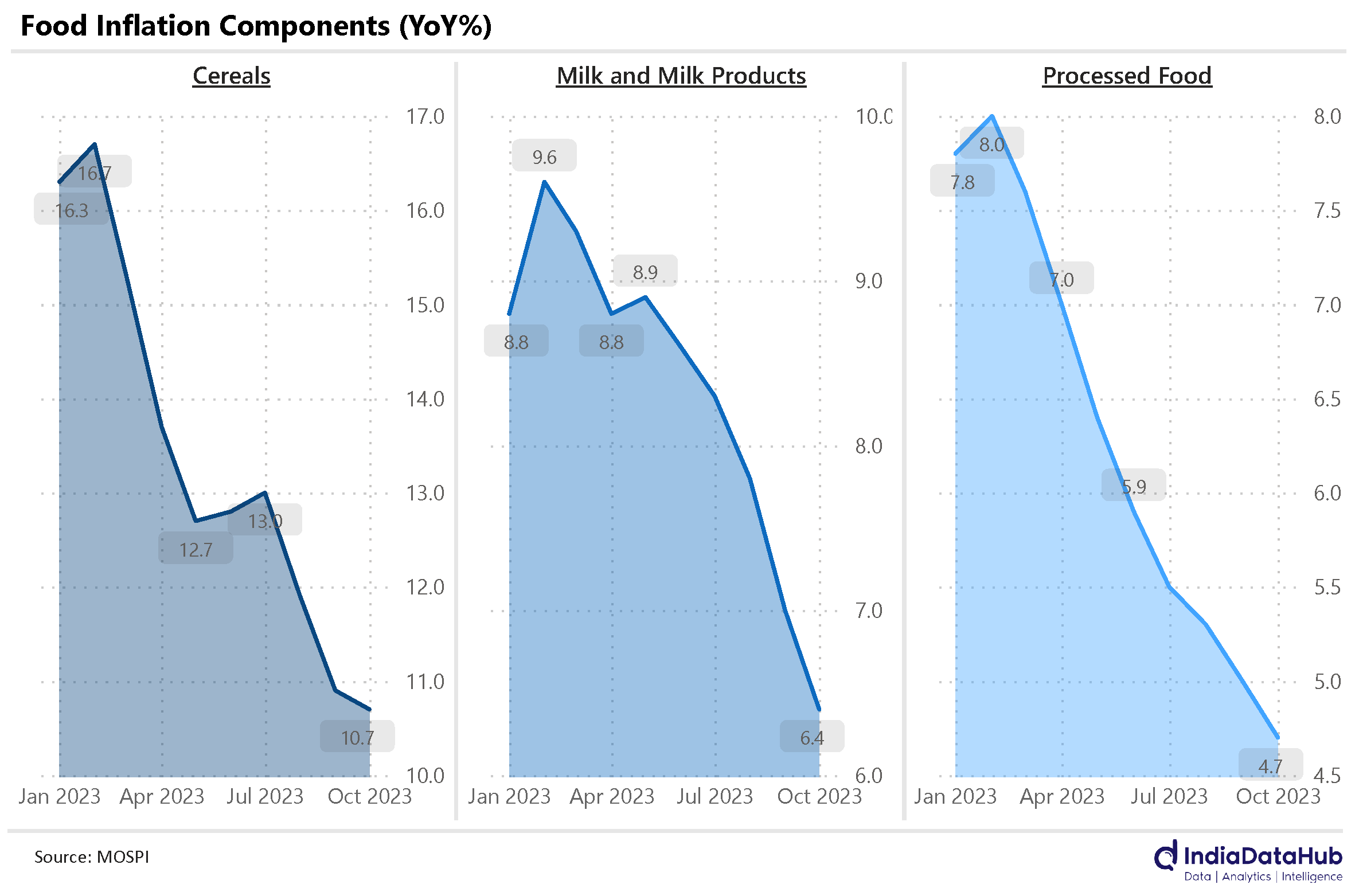

We release our self-service API portal next week. You can build APIs to query the data through an intuitive UI and even scan the metadata. Stay tuned!So Inflation. Headline CPI inflation moderated 15bps in October to 4.9% YoY. From its peak in July, headline CPI has fallen 250bps in the last three months. More importantly, CPI has reverted to the level in June, when it spiked due to the sharp rise in Vegetable and specifically Tomato prices. Both food and core inflation moderated in October. However, while core inflation is now below the level in June, food inflation is still slightly higher. Thus, the decline in inflation in the last three months is not just attributable to lower food inflation, non-food categories have also seen a sharp moderation.

Food inflation remained largely stable in October, moderating 10bps to 6.2% YoY. While Vegetable price inflation moderated, this was almost fully offset by the rise in Fruits and Pulses inflation. Inflation in both these categories has risen sharply in the last few months. However, excluding these two, inflation in most other categories has continued to decline. Cereals inflation for example has fallen to 10.7% YoY, down 6ppt in the last few months. Milk and Processed food has also seen a ~3ppt moderation in inflation in the last few months.

The benign CPI readings in the last two months, especially at the core and services level, ideally ought to have made the RBI shift its stance from hawkish pause. However, it will most likely wait, for what lies ahead of it is a spike in inflation in November and possibly in December as well due to the recent rise in Onion prices. As we discussed in last week's TWID, the full impact of the recent increase in Onion prices is likely to be felt in November. The MPC is thus likely to wait till this bout of vegetable price inflation to play itself out and signal a change in its stance only in the first quarter of next year. If there are no further shocks, then it is likely that rate cuts might happen in the first half of next year (CY2024).

India’s exports expanded 6% YoY in October. However, imports grew 12% YoY and consequently, the trade deficit rose to US$32bn, the highest on record. While the spike in the trade deficit is worrying it is likely an aberration. We have been highlighting how the change in Diwali is impacting all YoY metrics and some of it has happened in the trade data also, specifically imports.

Gold imports for example almost doubled, increasing by US$3.5bn in October. This almost certainly reflects the buildup of the supply chain in anticipation of a demand spike during Diwali. Similarly, electronics imports rose over 25% YoY, the highest growth this year. This also reflects the build-up in supply chains in anticipation of the demand increase during Diwali. So, the point is that we should not be unduly perturbed by the higher trade deficit in October.

The other big event of the week was the RBI increasing risk weights on some categories (mostly unsecured) of consumer loans from 100% to 125% (except for credit cards from 125% to 150% in the case of banks). This follows on from concerns expressed by the RBI Governor over the sharp growth in these loans in the last few quarters. As the chart below shows, in the last 2 years, such loans have increased by over 50% in the last two years in the case of the scheduled commercial banks and have been growing at over 20% for over a year now. This is ~10ppt faster than the growth rate of credit to other sectors of the economy. As of September this year, these loans account for just over 10% of the outstanding loans of Scheduled Commercial Banks.

In theory, these measures should reduce the credit growth in these categories of loans by increasing the amount of capital that banks have to set aside for making these loans. However, the increase in capital requirement is modest for banks with well-diversified loan books. If for example, the loans covered by the higher risk weights are 20% of the loan book for a bank, then the capital requirement increases by a modest 5%. However, in aggregate, the banks are already carrying significantly higher capital than that mandated by the RBI. As of June 2023, the scheduled commercial banks had a tier I capital ratio of 14.6% as against the statutory minimum of 8%.

Thus, banks can simply run down this extra capital they are carrying and continue business operations as they were. In that case, the RBI directive will have no impact on either their growth or profitability or the broader economy. It is likely then that the RBI might follow through with this measure with higher provisioning norms, which will directly impact profitability if the intended outcome of this regulatory intervention is not visible. And that is what makes this measure negative for lenders. The RBI intends to make lenders slow down the growth in their fastest-growing segment. And investors don’t like slower growth – although history shows us that, at least in the credit business, hypergrowth generally does not end well…

Globally, the US and the UK reported CPI data for October this month. And both countries saw a sharp moderation in inflation.

US CPI came in at 3.2% YoY, down from 3.7% readings in the previous two months. Energy was a key contributor to this moderation in inflation. UK CPI came in at 4.7% YoY, down sharply from 6.7% in September. This is the lowest CPI print in the UK in the last 2 years.

That’s it for this week. Tomorrow is the D-Day then! Fingers crossed…