Fed rate hike, Decline in FDI, Underperforming Rupee and more...

This Week In Data #11

In this issue of This Week In Data, we will discuss:

Fed rate hike and implications for India

Declining FDI

Decline in ECBs

Uptick in NRI Deposits

Depreciating rupee

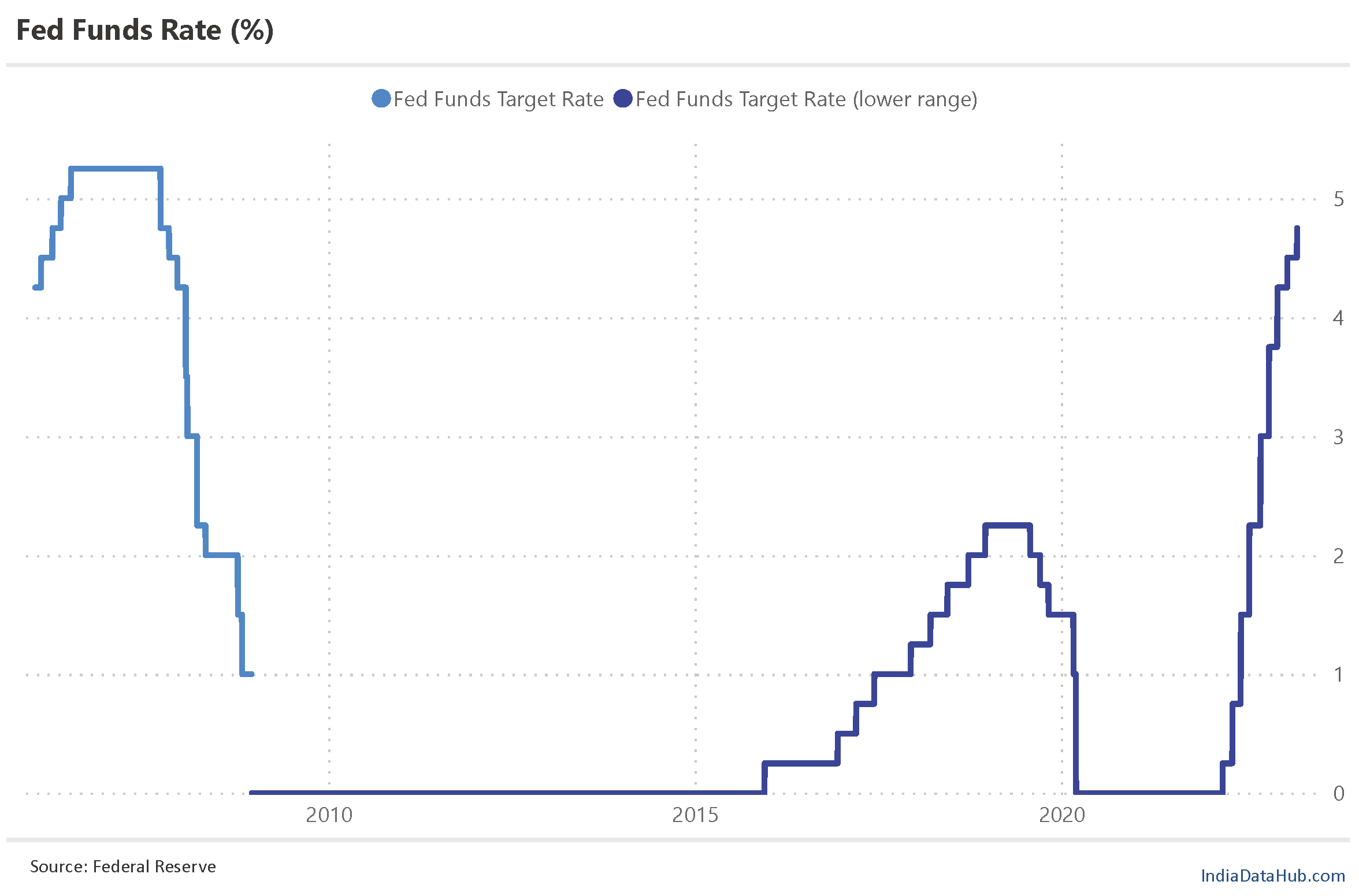

So, the Fed raised rates by 25bps this week to a range of 4.75 – 5%. While the 25bps hike was expected, expectations had been toned down after the mini-banking crisis in US and Europe. The Fed Funds rate is now at the same level as in September-2007, just before the global financial crisis. In a way, interest rates have completed a full circle. The Bank of England also raised its policy rate by 25bps to 4.25%. The ECB had already raised its policy rate by 50bps to 3.5% last week. On the other hand, the central banks of Brazil, Indonesia and Turkey kept their policy interest rates unchanged this week. So, there has been a divergence in the terms of rate trajectory between the developed and emerging market economies.

The question that now arises is whether the RBI will follow other emerging markets and pause in April, or will it follow the developed central banks and hike the policy rate? Worth noting is that in the last policy review, the MPC had signaled (with a 4-2 split) that it intends to continue policy tightening. And the two inflation readings since then have been higher than expected. And while crude oil prices have declined in recent days, the odds are for the MPC to hike the rate by 25bps (and indicate a pause thereafter), if there are no signs of a global contagion from the banking issues in the US and Europe.

Back home, it was a light week in terms of data flow. We got the FDI data for January and it was not positive. FDI continues to remain weak. While sequentially January was the second consecutive month of over US$6bn of gross FDI, the FDI received was still 30% lower on a YoY basis. As a result, the YTD FDI inflow is down 13% on a YoY basis and in absolute terms, it is at a 5-year low. The repatriation of FDI is flat YTD however, it is likely to see a spike in March when the Citi-Axis deal gets booked. This repatriation of FDI is also likely to be higher for the full year. FY23 is thus likely to be a disappointing year for FDI.

ECBs were also unusually weak in January. Sanctions totalled US$1.8bn, down almost 80% YoY. And outflows under the RBI’s Liberalised Remittance Scheme spiked in January to US$2.7bn, the highest ever. The budget has imposed a TCS on outflows under the LRS and so outflows will likely moderate hereon. On the bright side, there has been an uptick in inflows under NRI Deposits. The last 4 months have seen inflows totalling US$3.1bn. The corresponding period in the last financial year had seen inflows of just under US$1bn.

Even portfolio flows are not looking strong this year. YTD FPIs have been net sellers of US$2.7bn in the first three weeks of March. Most of this outflow has been from the equity market which has seen outflows of over US$3bn. Net net, the environment for capital flows is not looking pretty and what is helping the rupee is the sharp decline in the trade deficit – a decrease in the goods trade deficit coupled with an increase in the services trade surplus.

However, despite this lower deficit, the rupee is amongst the worst-performing currencies in the last 3 months. Against the basket of trading partners, the rupee has fallen by 4.3% in the last three months (Nov – Feb). Among the EMs only Turkey and South Africa have seen a sharper decline in their currency. Indeed, most EMs have seen their currency appreciate during this period.

That’s it for this week. More things to talk about next Friday!