GDP Growth, Inline Fiscal deficit, Credit growth and more...

This Week In Data #20

In this week of This Week In Data we cover

Strong 4Q GDP growth

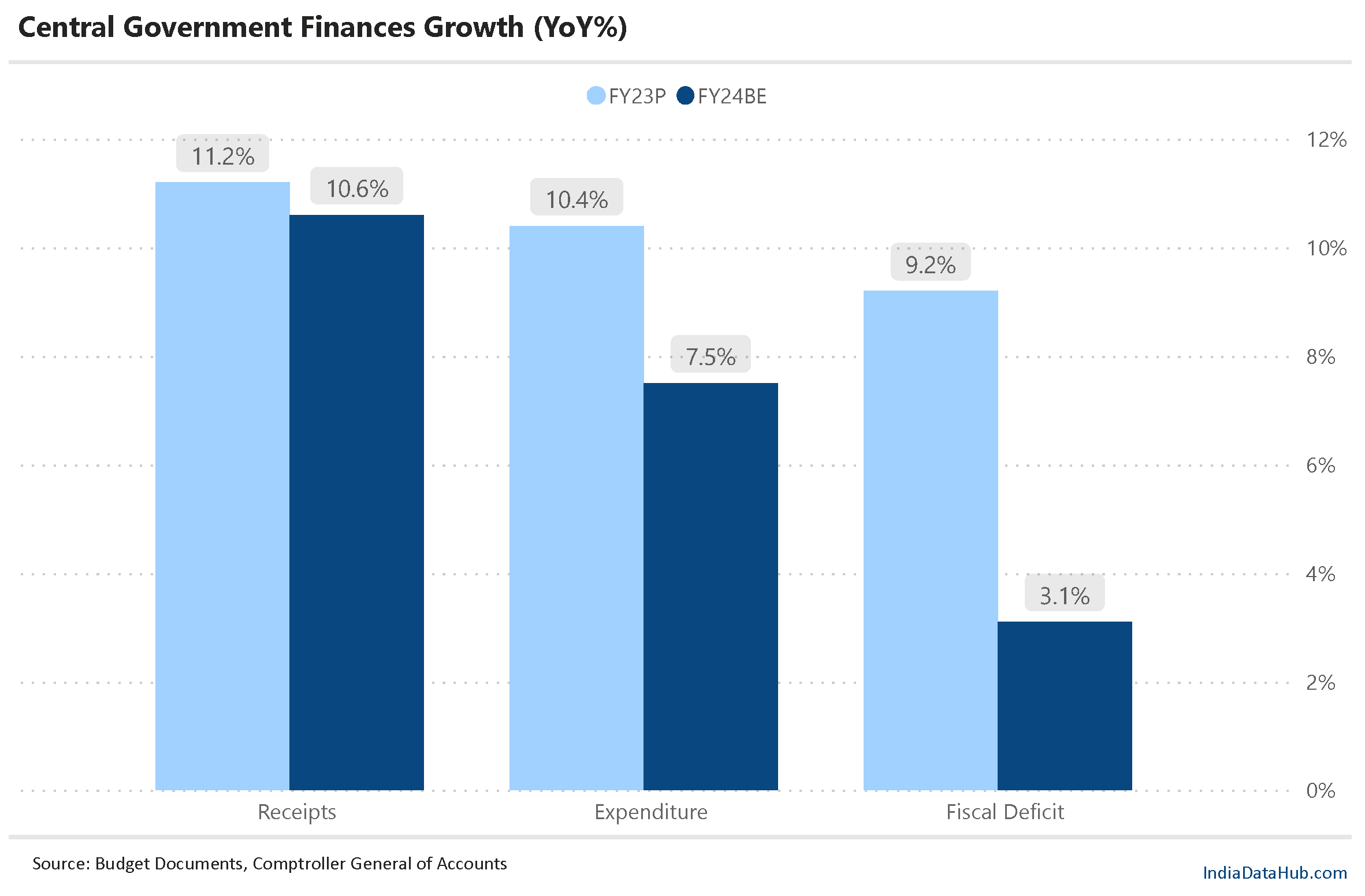

Provisional FY23 Government finances

Continued strong services and personal loan growth

Week 1 of Demon 2.0

Moderating global inflation

Strong US Payroll data

Lots of data to cover this week. So let us get right into it.

By far the biggest event of the week was the 4Q GDP release. And yes, it was a strong number. India’s GDP grew 6.1% YoY during the March quarter. This is a full percentage point above the implied 4Q growth estimate of 6.1% based on the advance estimate released at the end of February. Sequentially the GDP expanded 8.4% QoQ during the March quarter (not seasonally adjusted). This is the strongest expansion during the March quarter in over a decade.

The current FY24 GDP growth estimate is 6% as against 7.2% for FY23. There will be some upgrades for the FY24 estimate. But as we wrote here, the bigger picture remains that GDP growth is likely to decelerate by ~100bps during the current year. And nominal GDP growth will decelerate from 16% in FY23 to single digits. And if some of the tail risks emanating from the monsoon and global backdrop materialise, the deceleration in growth could be even sharper. And the high-frequency data for March and April does not suggest, for now, that there are too many upside risks.

We got the provisional full-year FY23 finances of the Central government this week. Both the fiscal and revenue deficit was slightly lower than the revised estimate but higher than the original budgeted estimate. This was achieved due to revenues which were slightly higher than the revised estimate whereas aggregate expenditure was in line with the revised estimate. The outlook for next year depends largely on the strength of revenue buoyancy. The budget estimate is for low teen growth in tax revenue as compared to high single-digit growth in nominal GDP. While nominal GDP growth is likely to decelerate sharply, receipts growth is budgeted to remain broadly the same.

RBI released the data on sectoral credit growth for April. And the overall picture remains the same as in March. The services sector and Personal loans continue to remain the key drivers of credit growth. Credit growth in both cases has been running around 20% for the past six months. Industrial credit growth on the other hand remains sluggish with 7% growth in April, the 5th consecutive month of single-digit growth. Agriculture credit growth has picked up to almost 17% in April, the highest in the last few years.

Currency in circulation declined by ₹365bn during the week ending 26th May. Assuming the entire decline is due to Demon 2.0, that would mean around 10% of outstanding ₹2k notes have been returned. In just the first week. And there are almost 18 weeks still left for people to exchange their ₹2k currency notes.

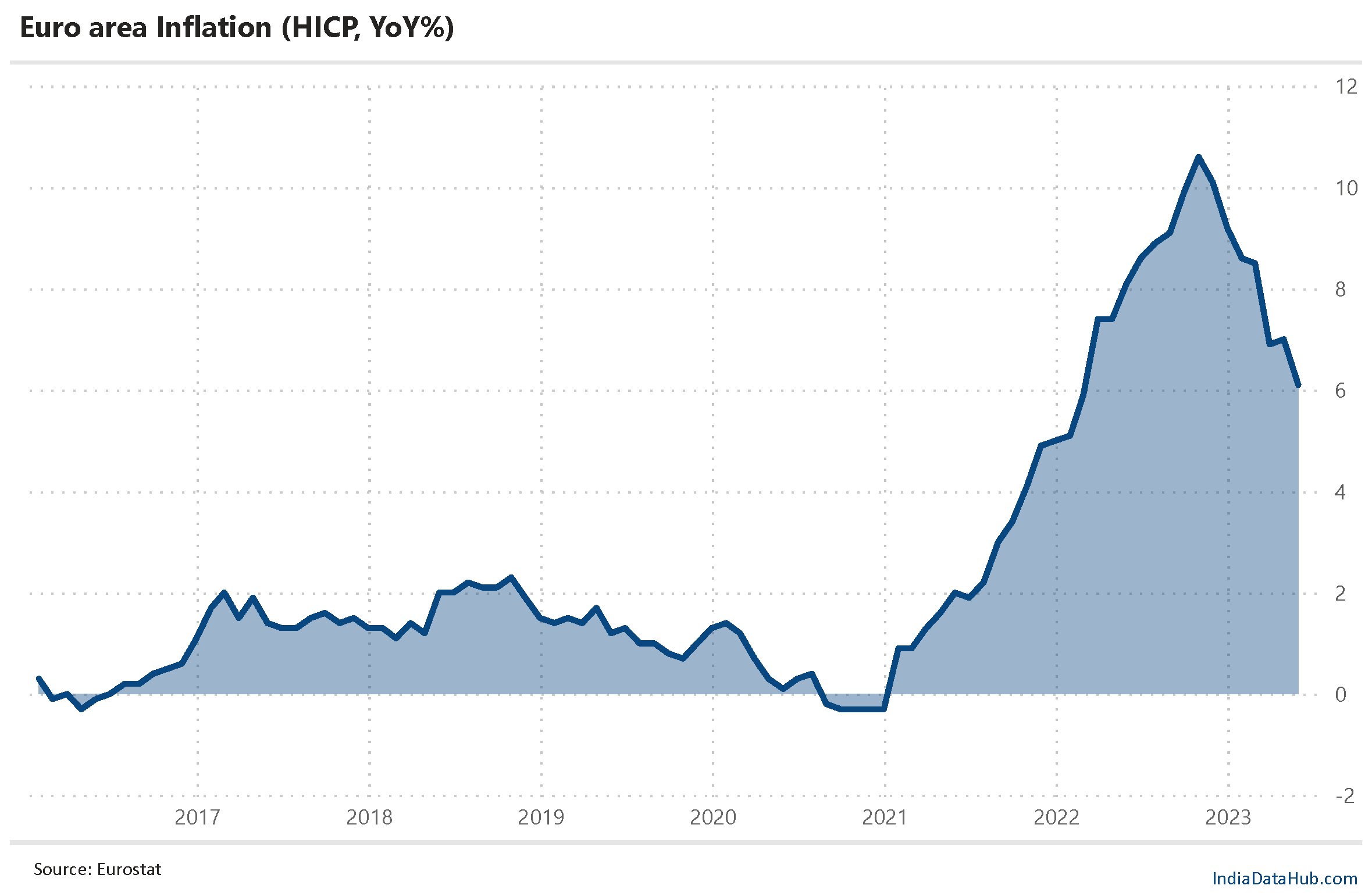

Globally, inflation continues to moderate. And sharply at that. According to the flash estimate by Eurostat, Euro area inflation as measured by the harmonised index of consumer prices declined by 90 bps to 6.1% in May 2023. From its peak in October last year, Euro area inflation has fallen 450 bps and is now the lowest since February last year. US Inflation has already fallen to two years low of below 5% as of April.

And the US released the crucial non-farm payroll data for May. Payrolls were stronger than estimated and prior couple of months data was revised upwards suggesting that the labour market continues to be fairly strong. That said, it is worth noting that the labour market typically tends to be a lagging indicator of growth and the first signs of a slowdown are likely to be visible elsewhere in the economy. So the inflation data is likely to encourage the Fed to take a pause but the labour market data might suggest growth may not be slowing sufficiently for inflationary pressures to wane on a durable basis. The Fed meets on 13-14th June to make the rate decision.

But more near-term, the RBI makes the rate decision next week. Given the pause in the last policy meeting and the soft inflation data subsequently, rates are likely to remain unchanged. But we shall see…