GDP Growth, Slowing Steel sector, Rupee at decadal low and more...

This Week In Data #147

In this edition of This Week In Data we discuss:

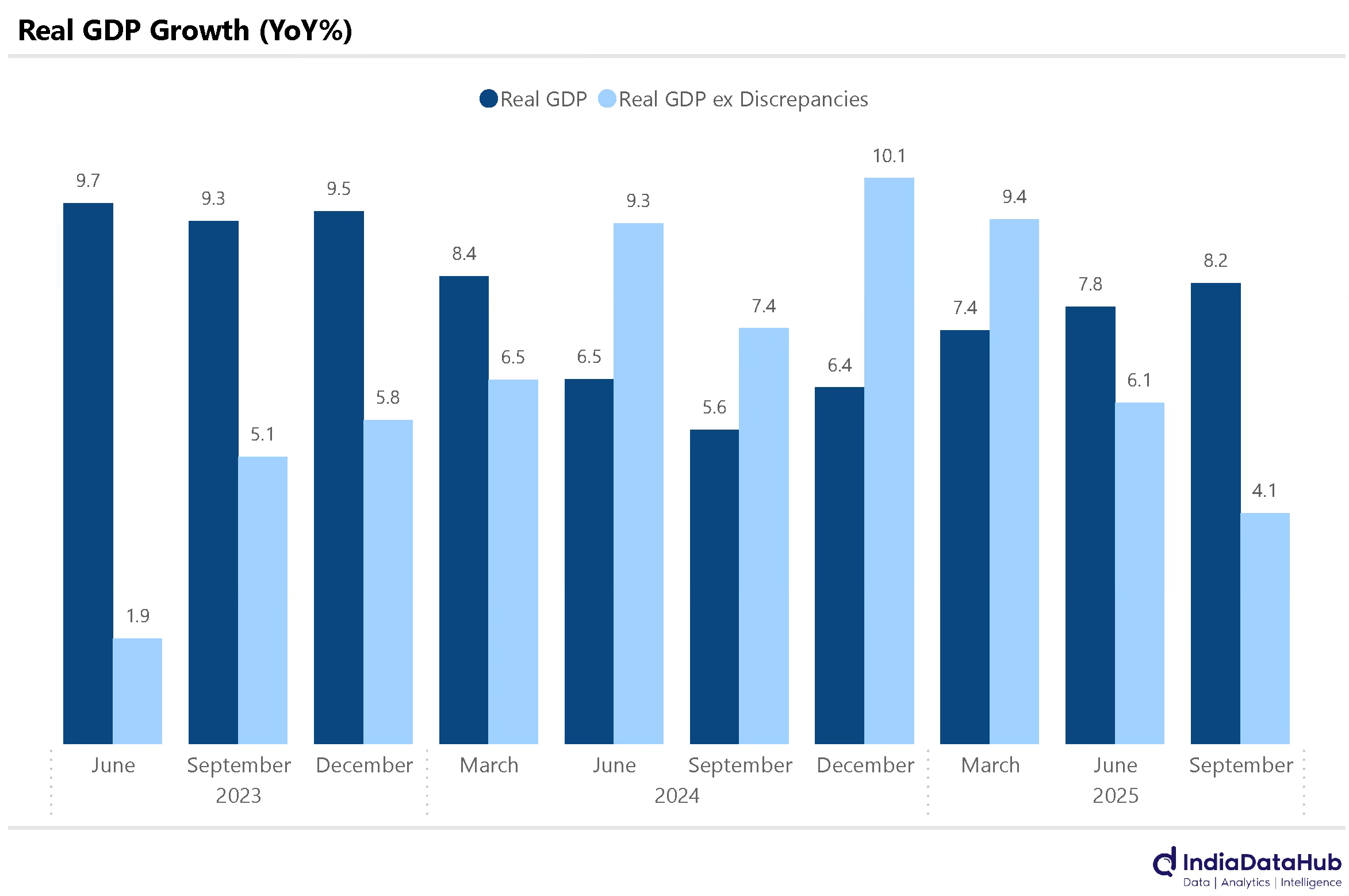

GDP Growth accelerated but because of discrepancies

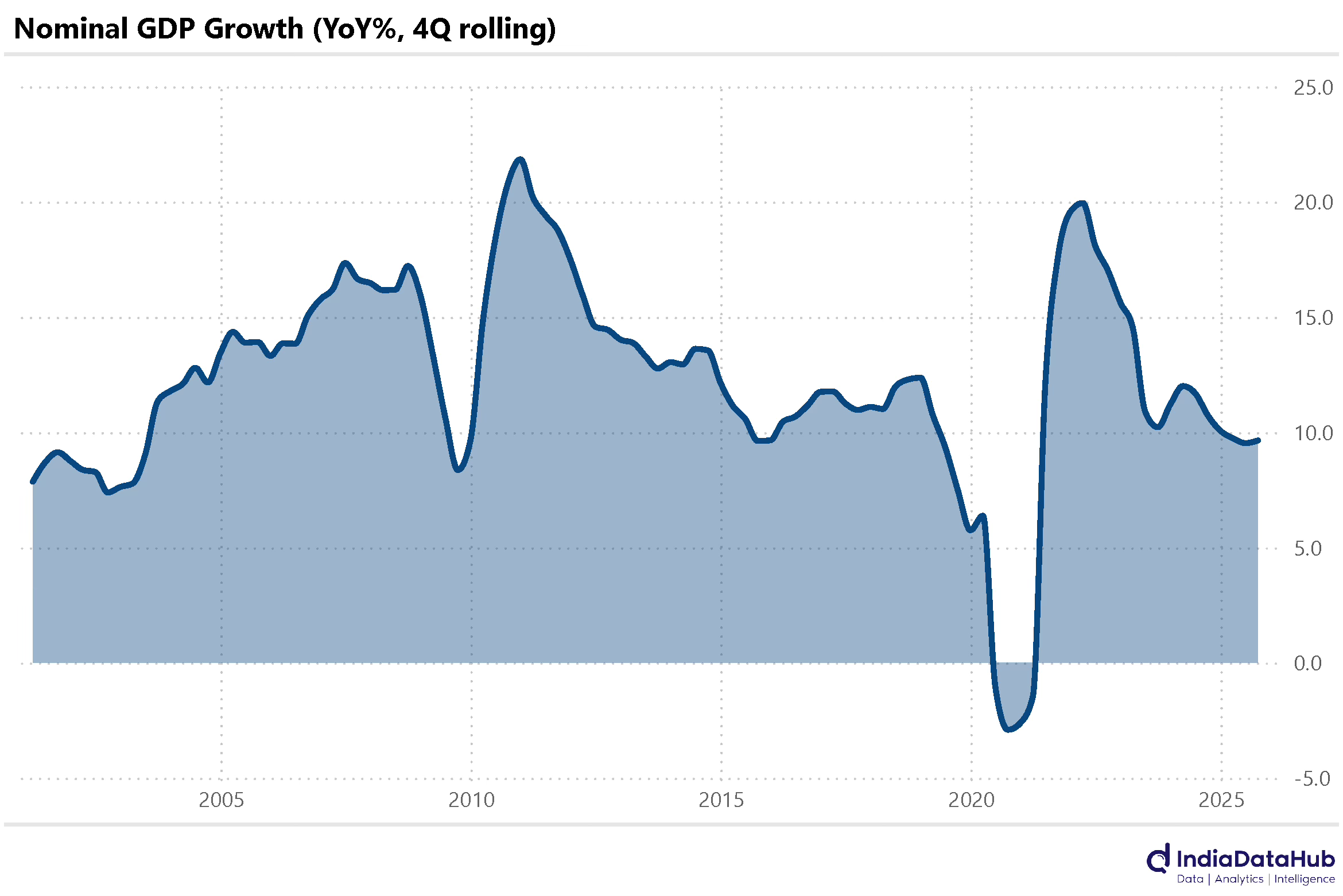

Nominal GDP growth remains sluggish

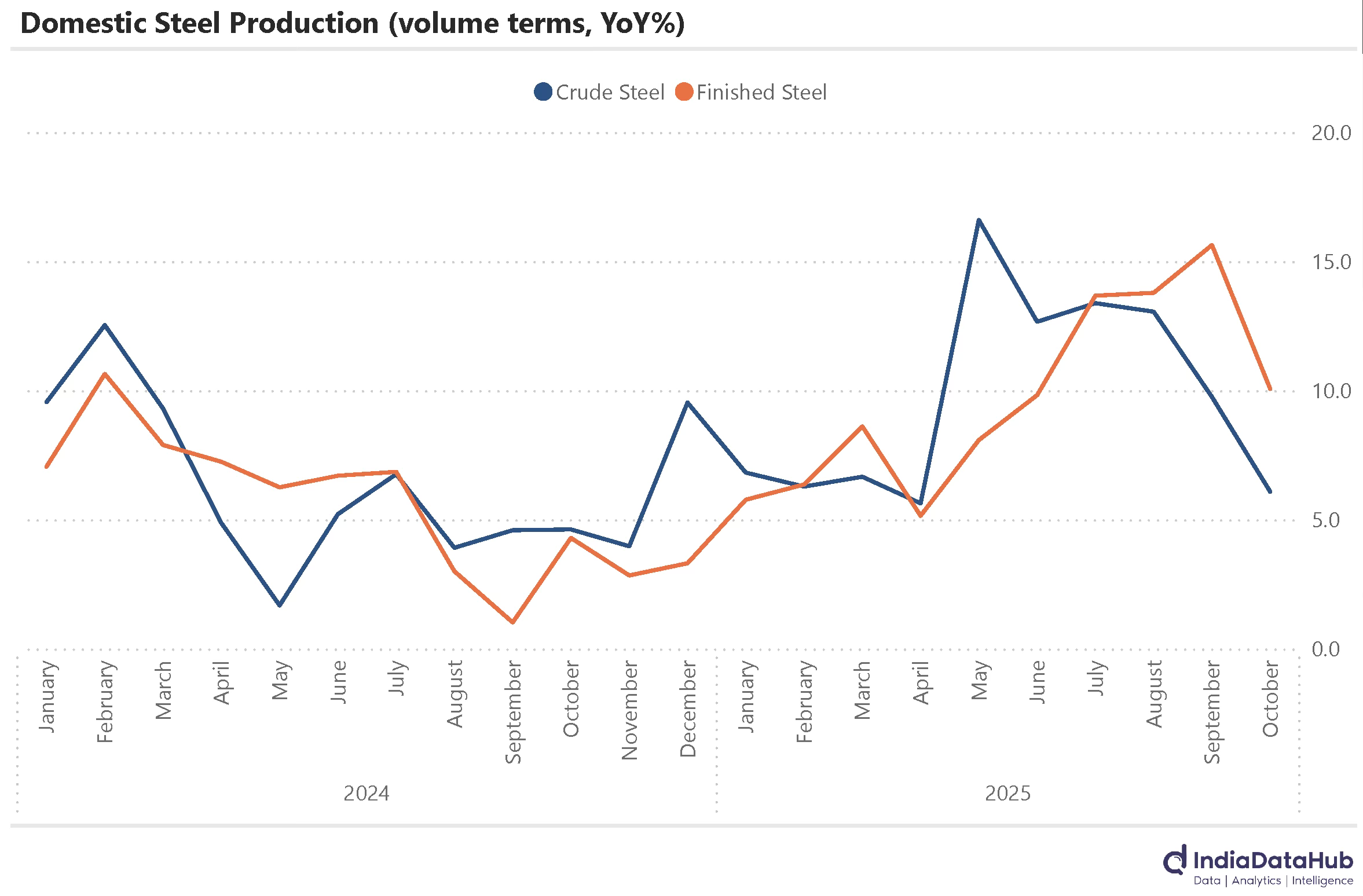

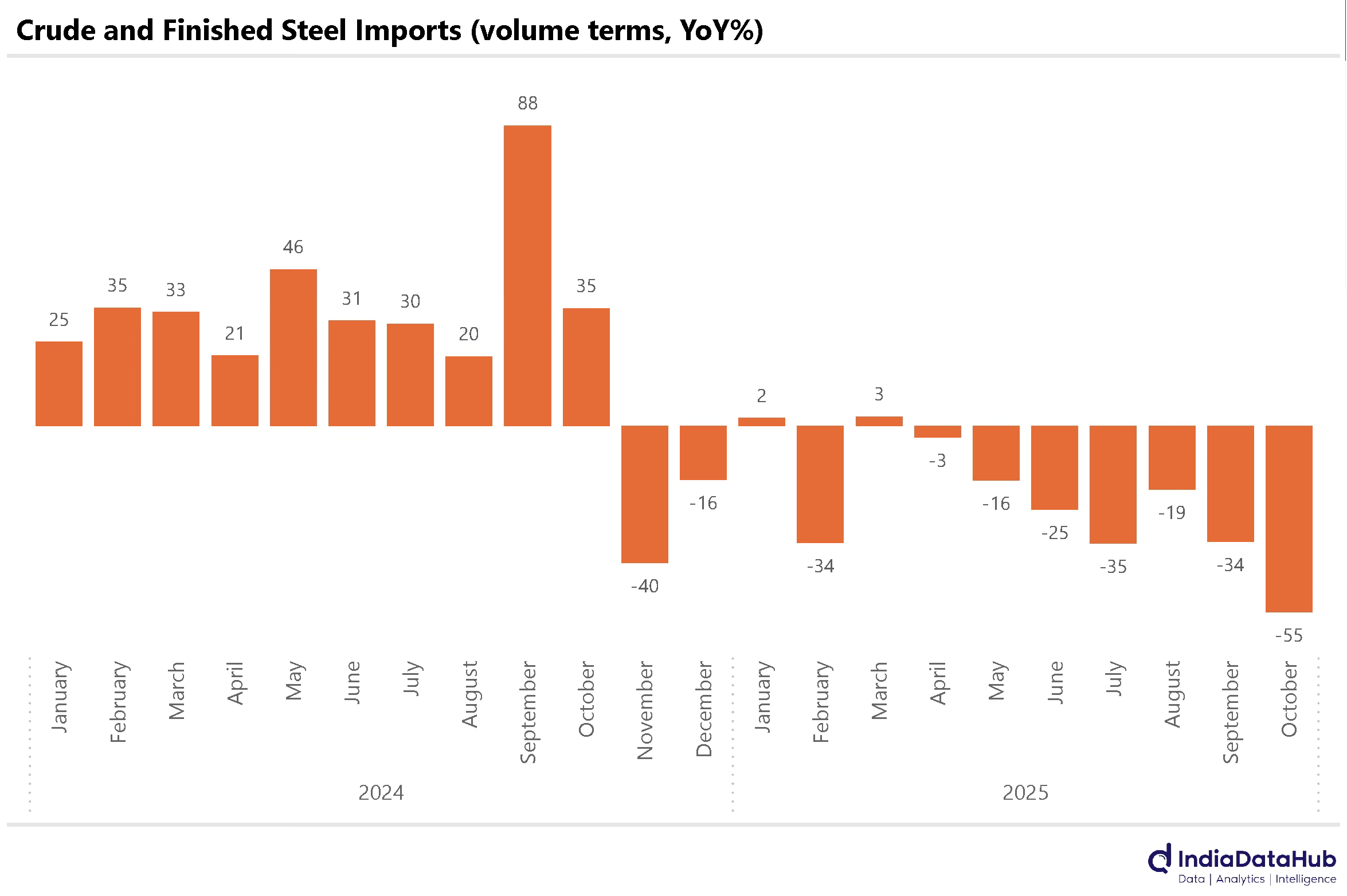

Domestic steel production and imports are seeing a slowdown

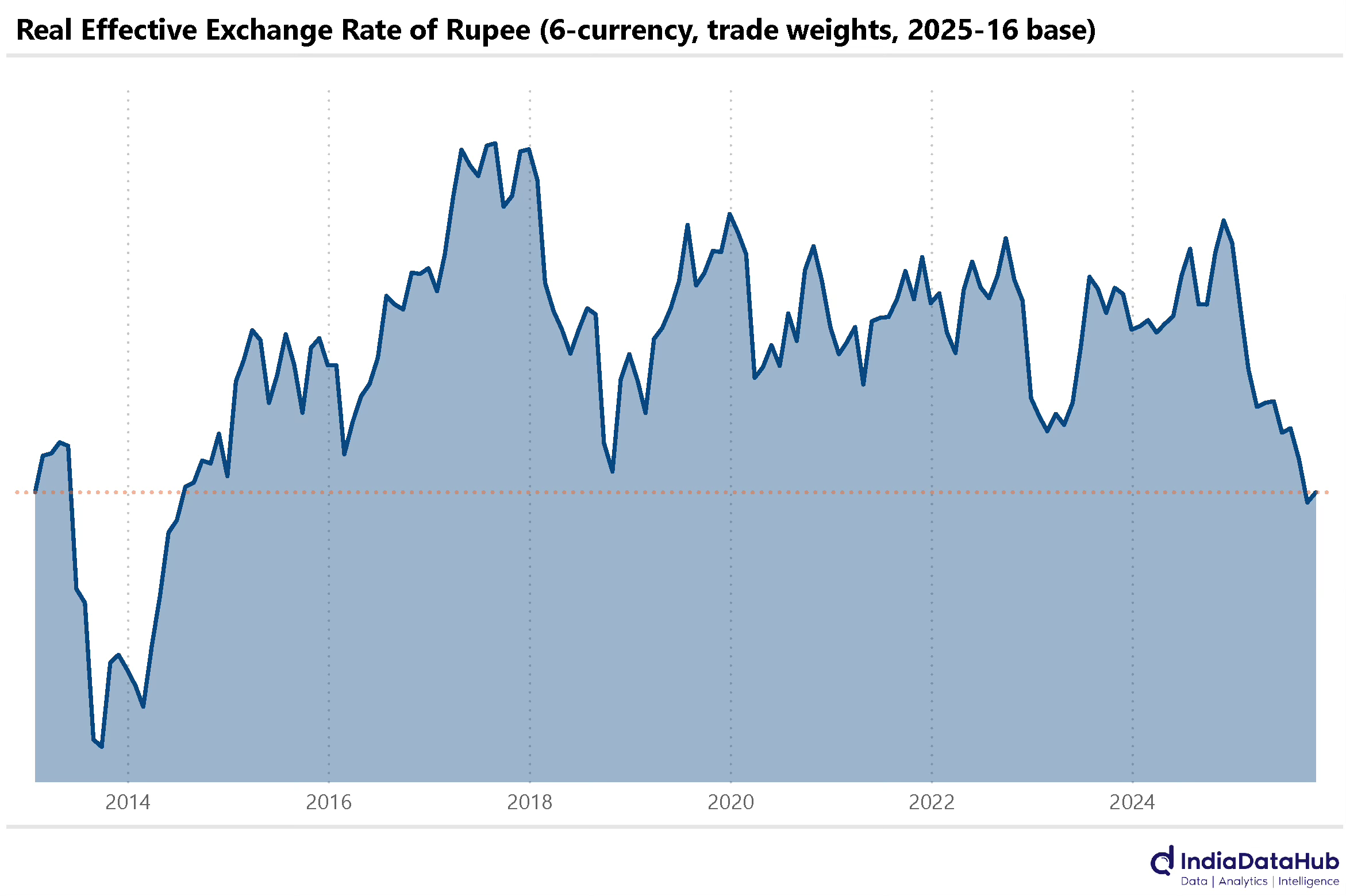

Rupee is at a decadal low on REER basis

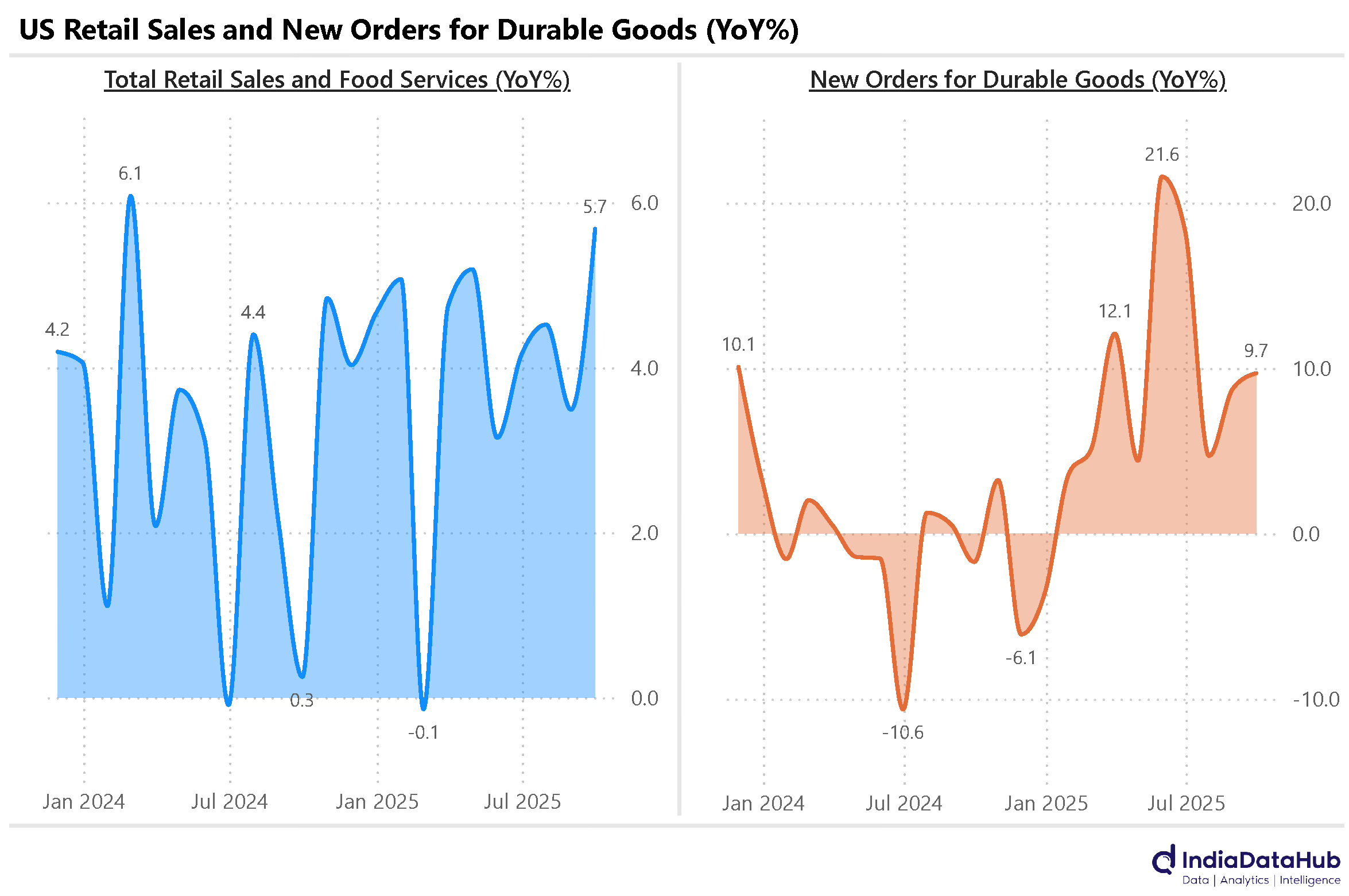

US retail sales accelerate to multi-month high in September

US durable goods orders also recover in September

India’s GDP grew by 8.2% YoY during the September quarter, the fastest growth in the preceding 6 quarters. This was well above the market expectation and is obviously good news. That said, our GDP data is not without its issues and so it is only reasonable that while we rejoice at 8% GDP growth, we also dwell over some of the issues with the data. And it is the same bugbear with this quarter’s data - GDP deflator and Statistical discrepancies.

Thus for instance, all the components of GDP – Private consumption, Government consumption, Gross capital formation, Net exports – grew slower than 8%! So what has driven this growth is ‘statistical discrepancies’, which swung from a small negative number to a large positive number. Statistical discrepancies is the factor used to align the GDP estimate as per the expenditure approach and the supply side (or sectoral) approach of estimating economic growth. Excluding discrepancies (admittedly not the right metric, but still) GDP growth for the quarter was just 4%.

The bigger picture is that nominal GDP growth was a modest 8.7% YoY, on top of a modest 8.3% growth in the September quarter last year. So the GDP deflator was close to 0% and this comes because a large part of the deflator estimation is basis the WPI which has no services component. Over the past few quarters, nominal GDP growth has averaged ~9% YoY. Outside of the COVID-19 pandemic, nominal GDP has very rarely grown in the single digits in the last two decades. And in the short run, it is nominal GDP that matters more than real GDP as most of the metrics we care about – corporate revenues and profits – are nominal metrics.

So while the 8.1% real GDP growth number is impressive, in practical terms, it is far less useful. But we are about to say goodbye to this series of GDP, which is well beyond its useful date. The new GDP series with 2022-23 as the base year and expanded data coverage debuts in February, along with the December quarter data. It has taken long for the data to migrate to the new series – the current series with 2011-12 base migrated much quicker from the earlier series with base year 2004-05. But hopefully, the new series has far fewer quirks of data than the outgoing series. So long GDP, hello GDP…

Domestic steel production has seen a slowdown in the last few months, although the growth remains healthy in absolute terms. Crude steel output grew 6% YoY in October, the lowest in the last 5 months, while finished steel rose by 8% YoY, the slowest pace in four months. Pig iron production contracted by 15% YoY, recording its steepest annual decline since March 2023.

Steel imports have also declined – finished steel imports declined for the seventh consecutive month in October, falling over 50% YoY - the sharpest drop since August 2020. Crude steel imports also fell for the second consecutive month in October, contracting 43% YoY, marking the steepest decline in the past seven months. Given the linkage between the Steel and the Construction sector, this makes us wonder - is the construction seeing a slowdown?

The rupee has been falling in recent months against all major currencies. And a consequence of this is that on a REER basis, the rupee is now at its lowest in over a decade. Effectively, the fall in the rupee has been more than what the inflation differentials between India and the other large currencies would warrant. And this means that the rupee has gained an element of competitiveness. In theory, this should boost exports (and offset some of the tariffs) and discourage imports. And this should reduce India’s trade deficit. Will theory translate into practice? We shall see…

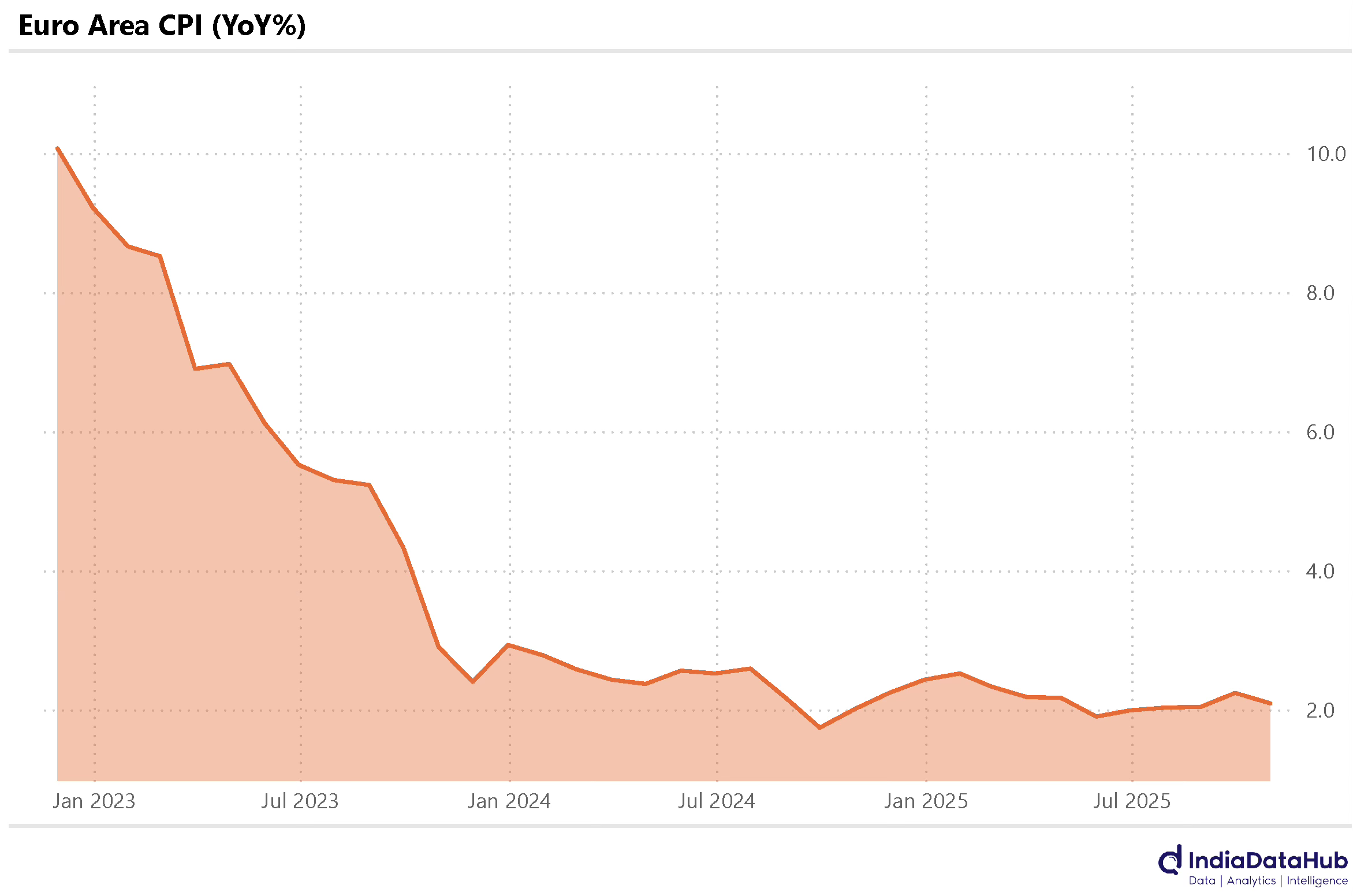

Inflation declined modestly in Euro area as per the flash estimate for November. The HICP fell to 2.1% YoY from 2.2% in October. This is broadly the same level the HICP was a year ago. Germany recorded a 2.3% rise in prices in November, slightly higher than the same month last year, while consumer prices increased by 0.9% in France and 1.2% in Italy.

In the United States, the Census Bureau reported a 9.7% year-on-year increase in new orders for durable goods in September, the fastest growth in three months and higher than the 1.7% decline in September 2024. Excluding defence, durable goods orders rose 9.5% year-on-year. Additionally, U.S. retail sales grew 5.7% year-on-year in September, the fastest pace in 32 months, based on non-seasonally-adjusted data. So while the labour market data is softening, the real data is not yet seeing a material softening. Growth remains reasonably robust.

That’s it for this week. See you next week…

Good article