Improving FDI, Accelerating Credit growth, RBI Gold holdings and more...

This Week In Data #167

In this edition of This Week In Data we discuss:

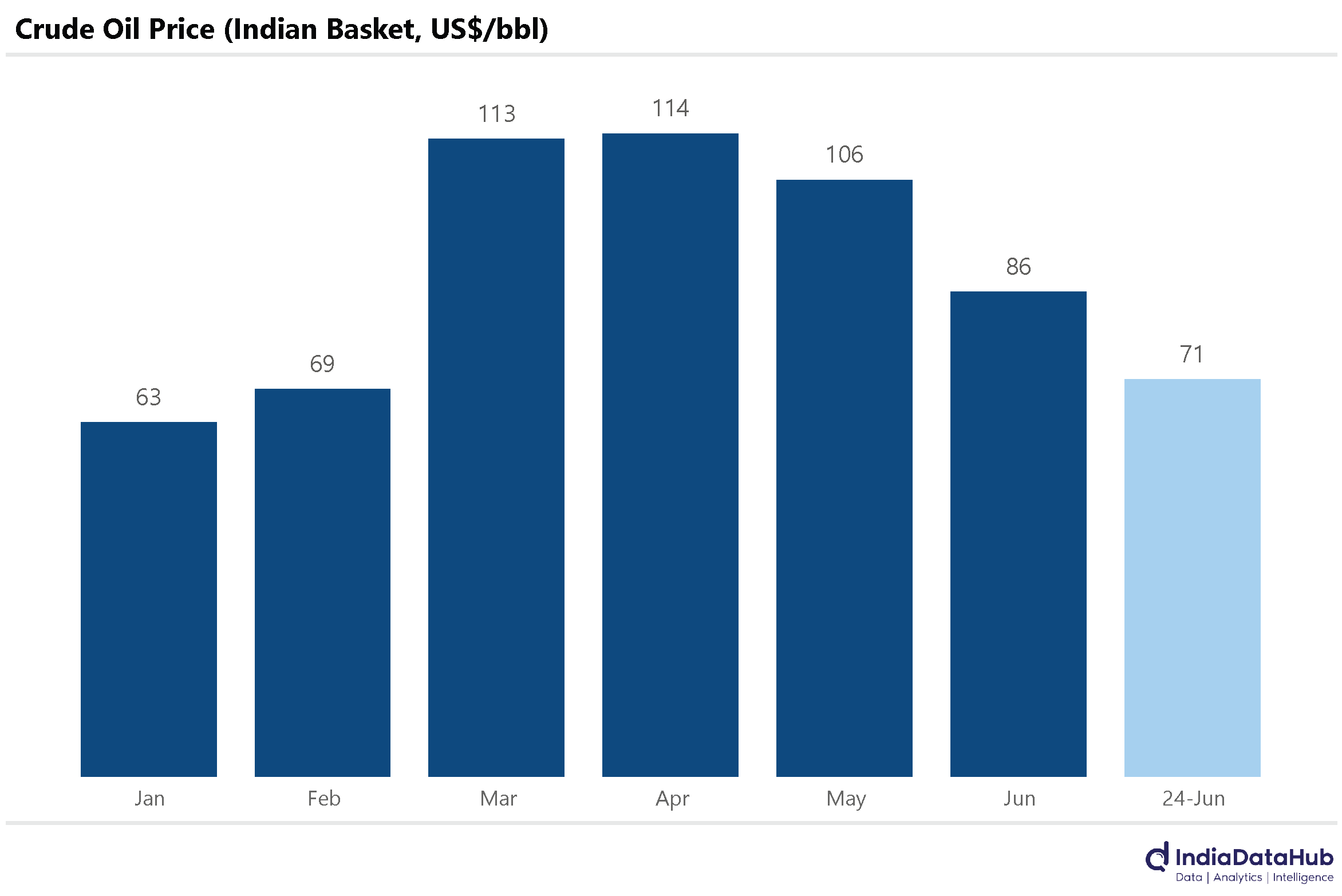

Oil prices almost back to pre-war levels

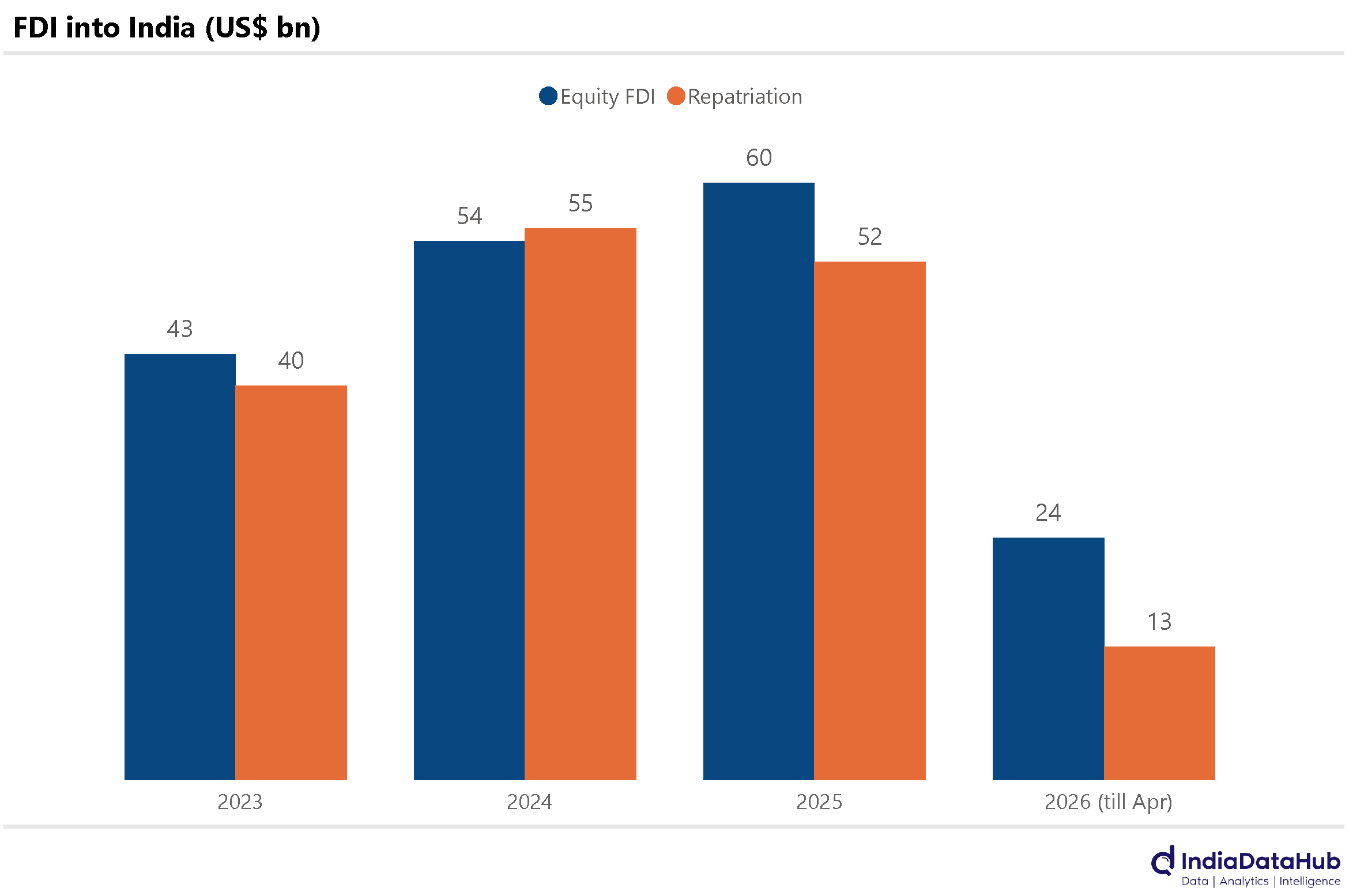

April saw the second highest FDI inflow on record

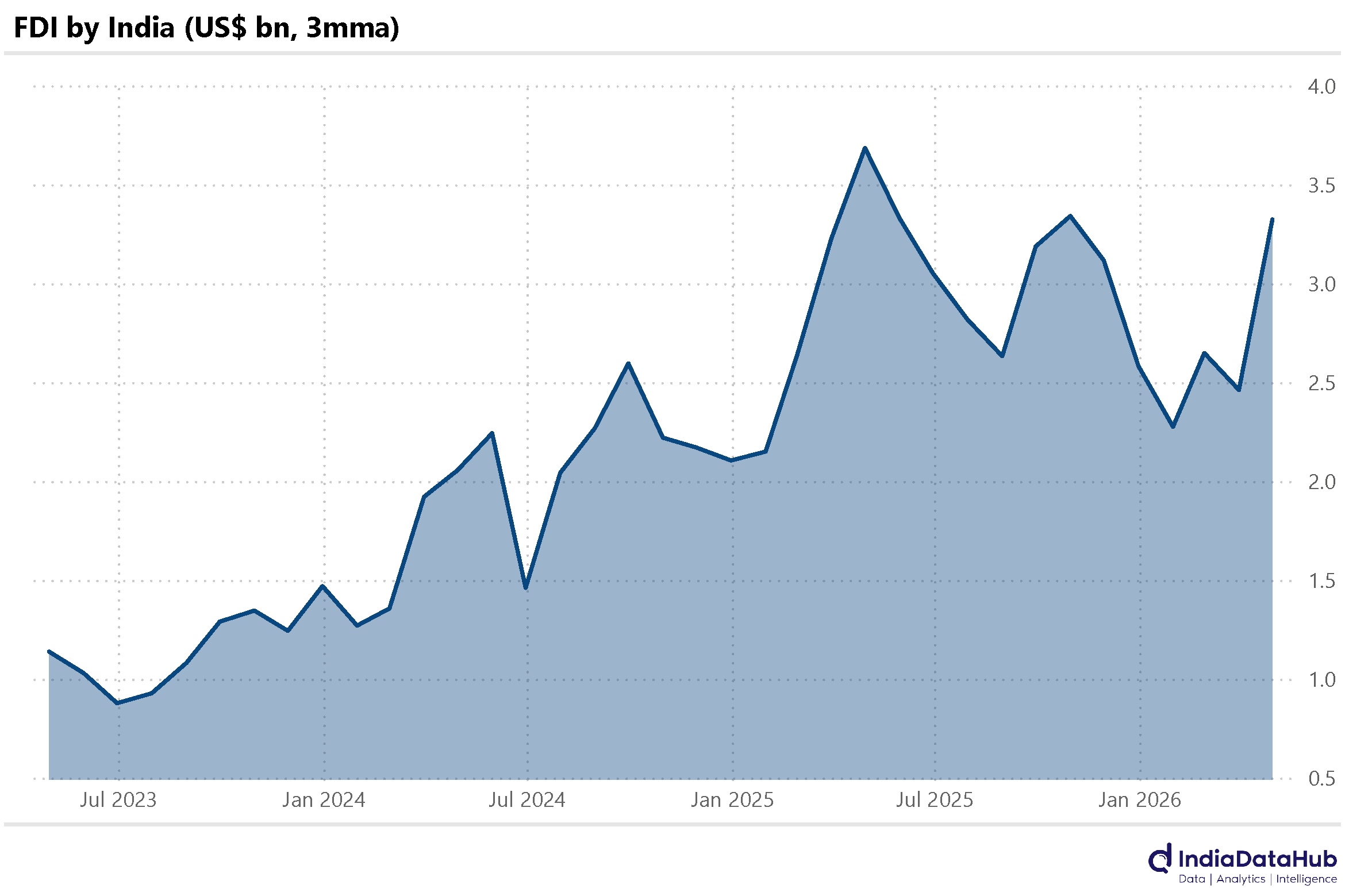

Outward FDI also picked up in April but the trend is decelerating

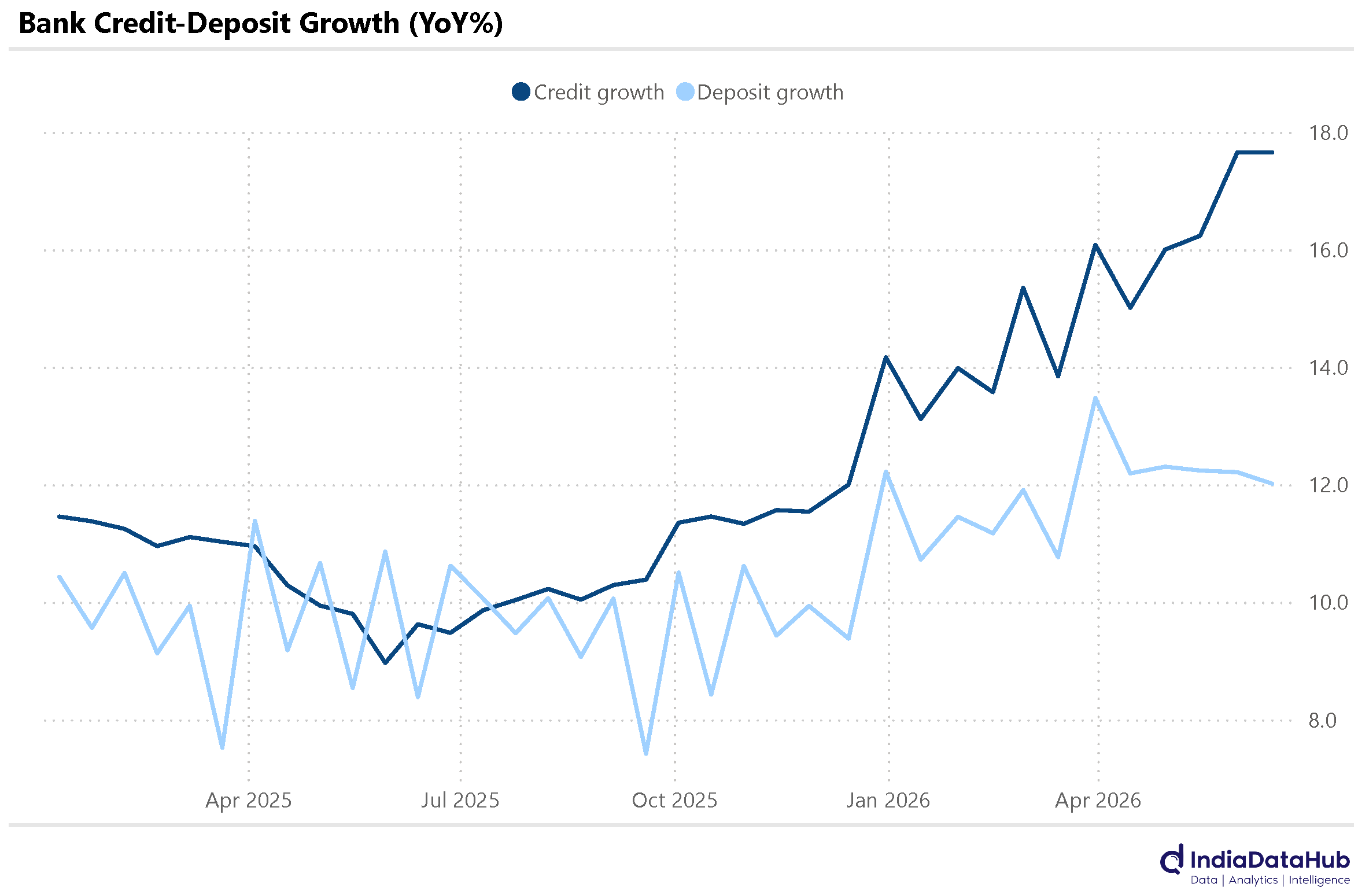

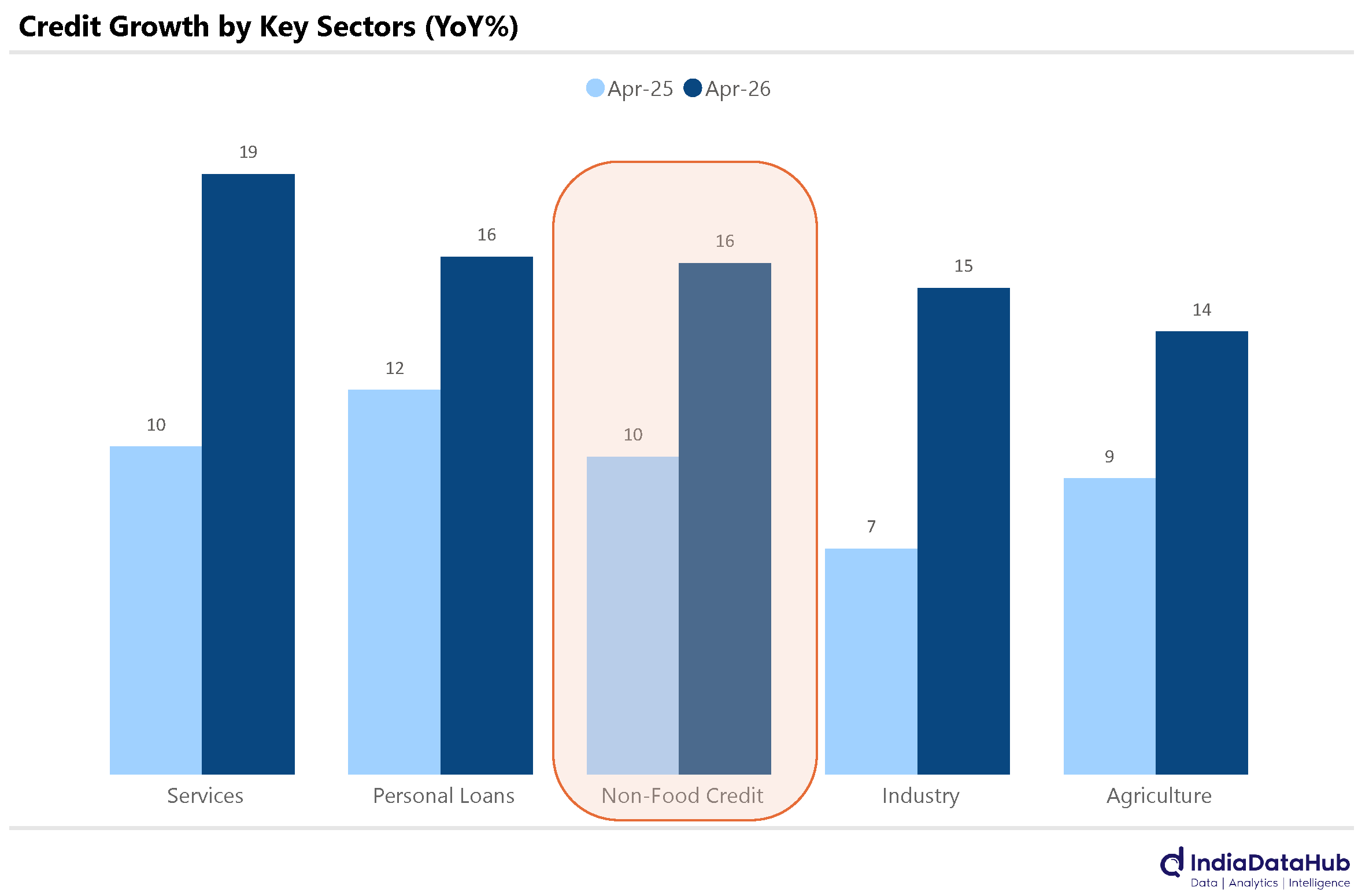

Credit growth continues to accelerate, across sectors

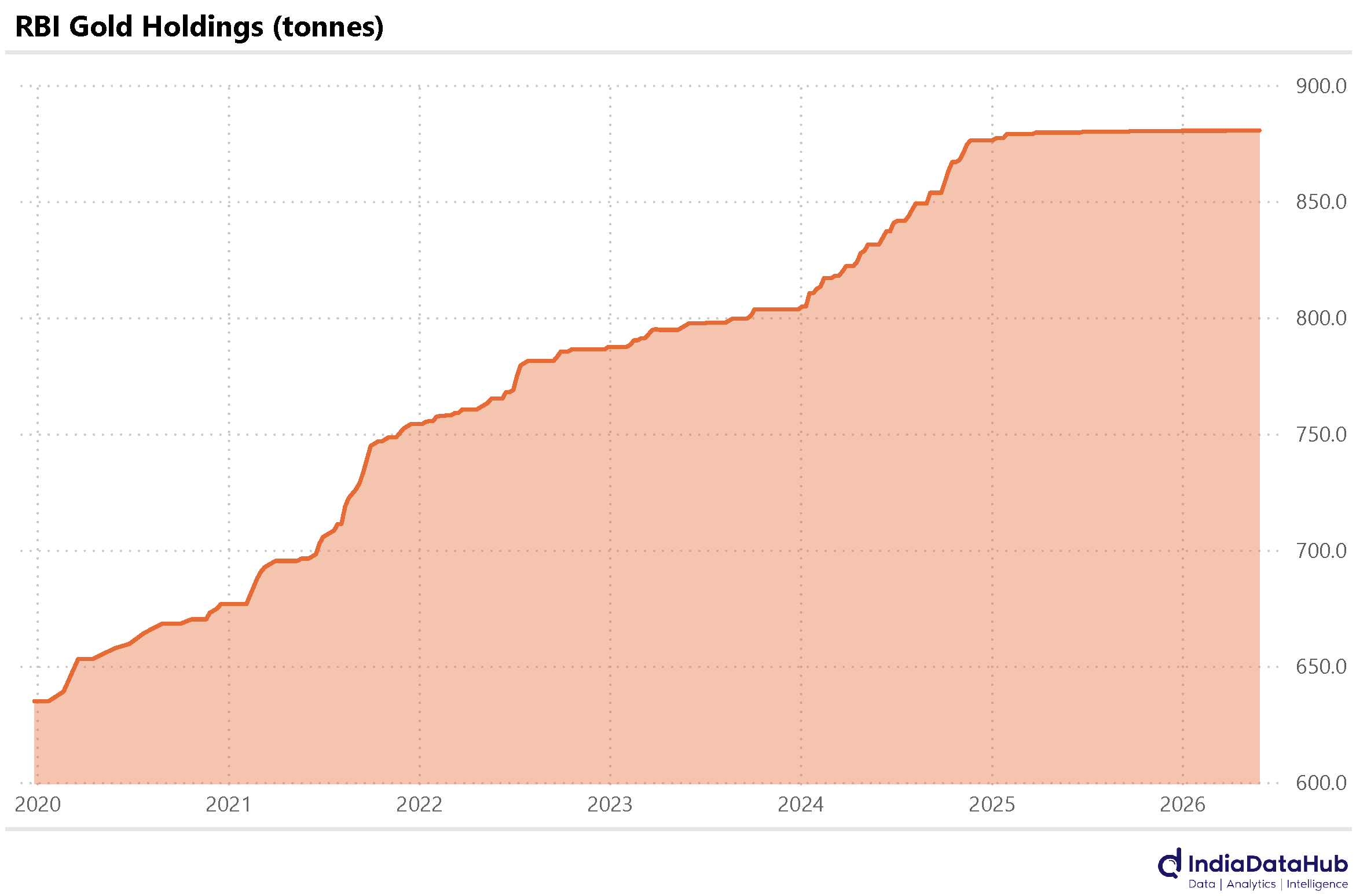

RBI’s Gold holdings data for May is out!

Strength in formal business creation continues

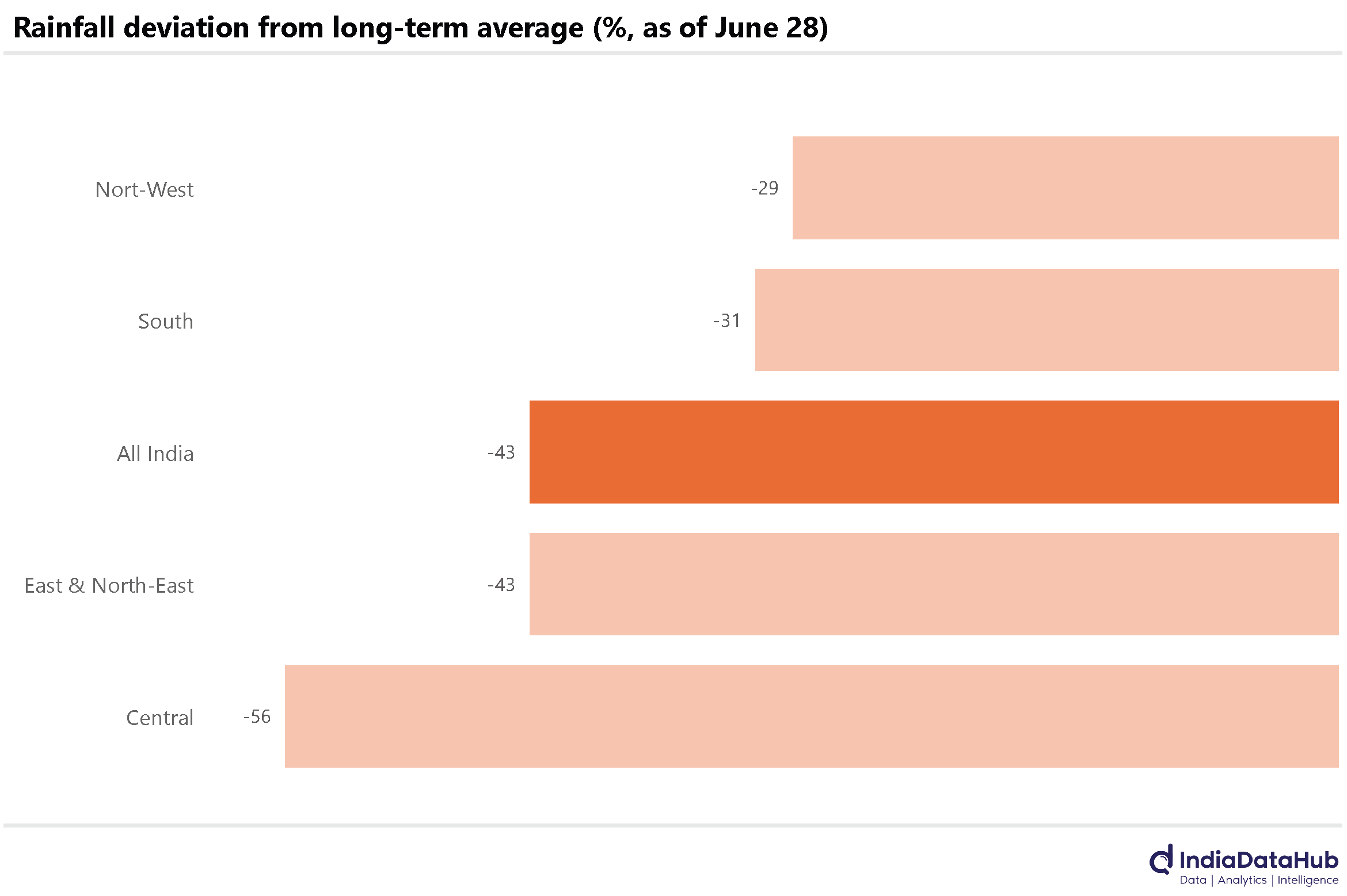

Rains now replace Oil as the macro worry

International oil prices continue to trend down. So far in June, the Indian basket of crude oil has averaged US$86/bbl, down from ~US$90/bbl as of last week. And on Friday, the price was US$71/bbl, just 10% higher than the pre-Iran war price. So oil prices, if they stay at these levels, have all but normalised to pre-war levels. And while the rupee has depreciated in the meantime, the stress on inflation, current account and the fisc should substantially reduce, if not fully normalise. And that is good news.

And April was a record month for FDI. The actual equity FDI inflows totalled US$12.4 bn in April, the second highest on record. The highest was in August 2020 when Reliance Jio raised equity. And in the three months before April (Jan-Mar quarter), FDI inflows were up 50% YoY. At the same time, repatriation of existing FDI has plateaued off. Annualizing the outflow during the first 4 months suggests, total repatriation for the full year 2026 will be flat YoY for the second consecutive year.

On the flipside, the strong momentum on outward FDI has continued. April saw almost US$5bn of outward FDI by Indian businesses, up 50% YoY. However, in general, outward FDI seems to be moderating. In the first 4 months of 2026, outward FDI has actually declined modestly on YoY basis. So, while the large inflow in April is probably an outlier, FDI has been trending up, on both gross and net basis. That said, this recovery is from a low base and thus this trend needs to sustain for several quarters before FDI gets to a reasonable share of GDP.

Credit growth continues to accelerate. As of mid-June, credit growth stood at almost 18% YoY, almost 4ppt higher than at the start of the year. Deposit growth, however, continues to remain stable at ~12% YoY, and thus, credit growth is outpacing deposit growth by a wide margin.

And while data on the sectoral composition of credit growth, as of the end of April, the drivers were fairly broad-based. Thus, while Industrial sector credit growth has picked up from 7% to 15% over the past year, the Services sector has picked up from 10% to almost 19%. And personal loans from 12% to 16%. Even Agriculture has seen credit growth pick up from 9% to 14% over the past year.

There was a bit of a brouhaha a few weeks ago over the RBI’s Gold holdings and whether the RBI had sold gold, which it holds as part of its FX reserves. While the RBI had issued clarification that it had not done so, data released this past week on the actual physical gold holdings should finally put the matter to rest. As of May 29th, the RBI held 880.52 tonnes of Gold, unchanged since early April and slightly higher than its holdings as of the end of March, which were 880.34 tonnes. So that is that.

But the bigger question is, if RBI routinely uses its reserves to intervene in the FX market, how does it matter whether it uses its holdings of US Treasuries or Gold? Reserves are reserves and intervention is intervention…

The strength in formal business creation has continued through into this year. In the first 5 months of this year, around 160k new formal businesses were set up. This is an increase of almost 20% on a YoY basis. Note that 2025 itself had seen over 30% growth in formal business creation. At this rate, 2026 will see almost 400k new formal businesses being created. For reference, a decade back in 2016, India had seen just 120k new formal businesses being created.

Lastly, the monsoon. And it has got off to a fairly poor start. Till yesterday, the cumulative rainfall so far in June is 43% below normal, with Central India (Maharashtra, Gujarat, Madhya Pradesh, Chhattisgarh, Odisha) seeing the biggest deficit in rainfall.

The region has received rainfall 56% below normal, while South India has also seen a 31% deficit in rainfall so far in June. East India has also seen over 40% deficit in rainfall so far. So, even as one risk to the economy (Oil prices) has receded, another (rains) is rearing its head.

That’s it for this week. See you next week…