Inflation, MF Flows, Aviation, Insurance and more...

This Week In Data #116

In this edition of This Week In Data, we discuss:

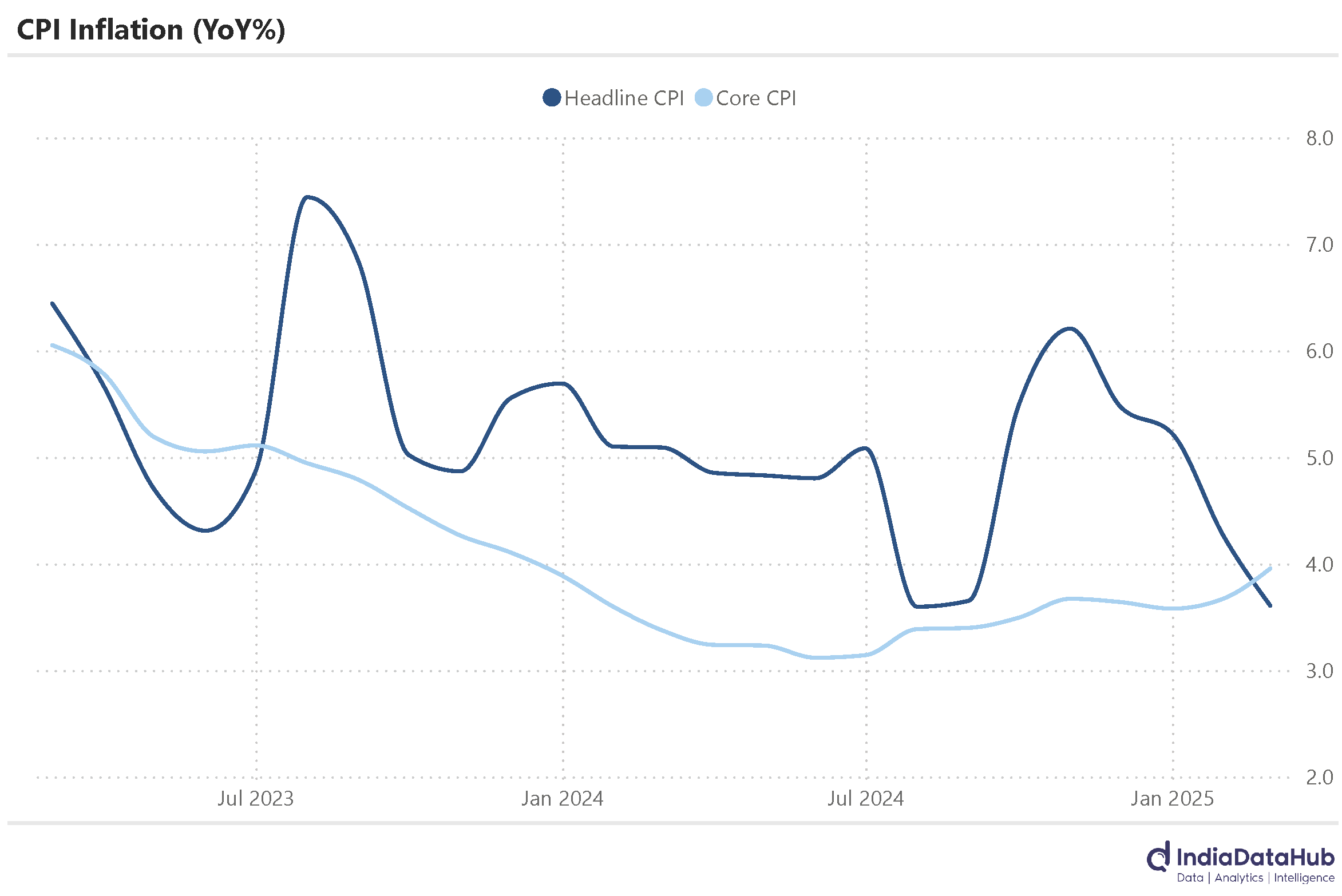

Low February inflation almost seals another rate cut next month

Inflows into equity funds moderate but remain strong

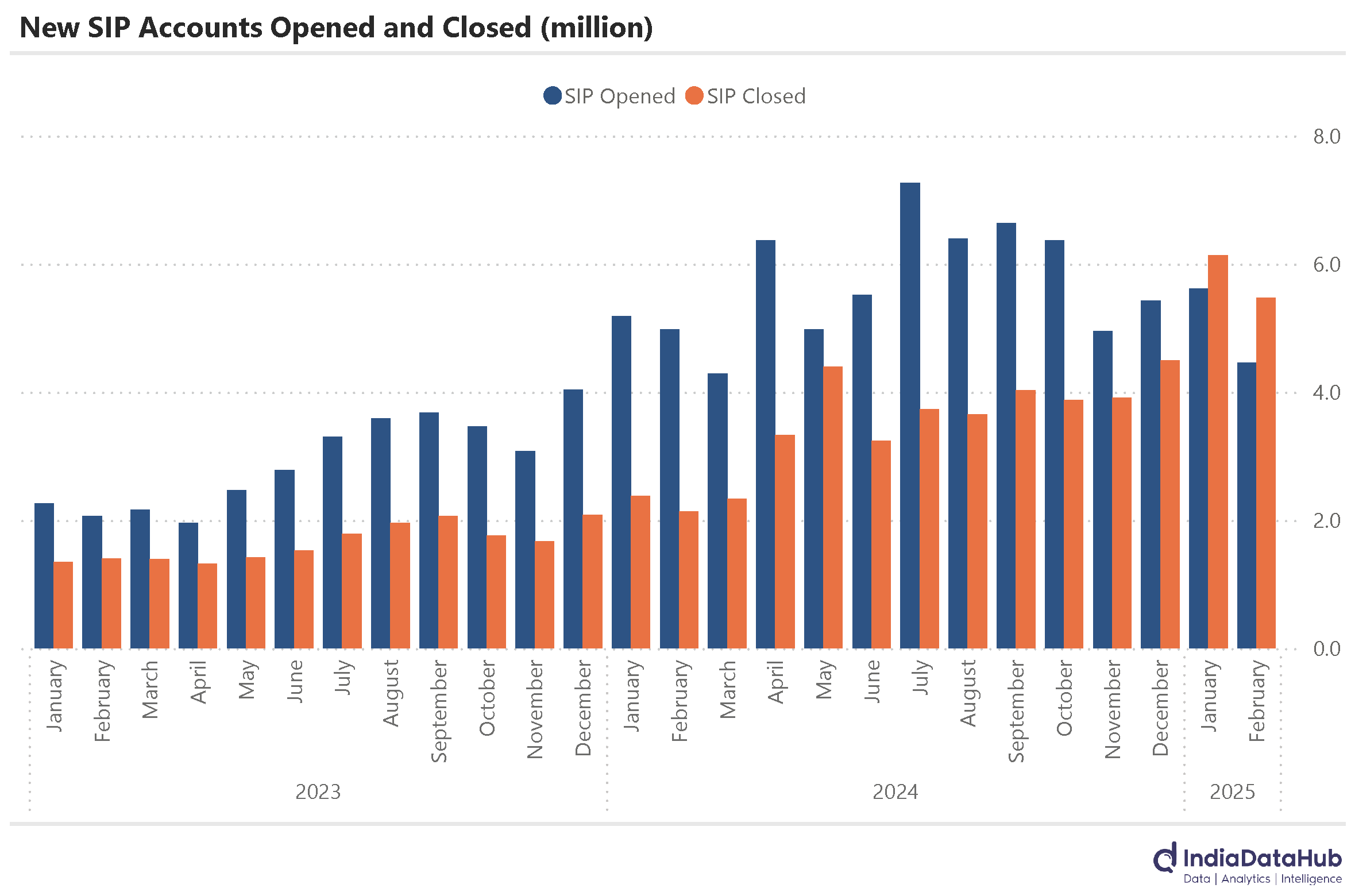

Addition to Equity folios and SIPs slows down

Recovery in domestic aviation sector and Indigo continues to gain

Life Insurance sector continues to see a slowdown driven largely by LIC

Wireless telecom sector returns to normalcy in December with Jio and Airtel gaining subs

Inflation declined further in February to a 7-month low of 3.6% YoY. However, after remaining stable for several months, core inflation ticked up almost 30bps to 3.95% and is the highest since November 2023 – but still comfortable at below 4%.

Most of the increase in core CPI is due to higher gold prices as the core-core CPI which strips out gold and retail fuels rose only 10bps in February. So, the uptick in core inflation is not disconcerting. Consequently, this low February CPI print effectively seals another rate cut from the RBI in April and possibly also brings another 25bps rate cut in June into play.

Mutual fund inflows dipped in February. Net inflows into equity funds totalled ₹292bn, the lowest since April last year. More importantly, while the equity schemes saw a 1.8m increase in folios in February, this is the lowest growth in the last 15 months.

Even SIP flows moderated to a three-month low and the SIP closure rate was above 100% for the second consecutive month. The volatility in markets has resulted in a moderation in retail flows. However, despite markets being down in double digits, flows are still positive.

The domestic aviation sector is seeing strong growth. January saw a double-digit increase in the number of flights (11%), the highest growth in the last few quarters. At this rate March will over 100,000 domestic flights in the country – that’s an average of over 100 flights taking off in the country every hour!

The passenger traffic has also seen double digit growth, the second time in the last 3 months that this has happened. Over the past three months domestic passenger traffic has grown by 10% YoY, the fastest growth since 2018 (adjusted for the strong growth during Covid recovery).

The one thing that has not changed though is the continued rise of Indigo. Indigo’s market share, in terms of passengers carried, rose to 65% in January, the highest ever and a 5ppt increase over the past year! And post the merger, AirIndia (+Vistara) has lost share in the last couple of months. In January this year, Air India carried 17% of the passenger traffic, down from 20% last year in January (Air India + Vistara).

The life Insurance sector continues to struggle. The number of new policies sold in February declined 22% YoY, the fifth consecutive month of decline. And while the decline has largely been due to LIC, even the private insurers have seen weak growth – almost 0% growth in new policies in the last 5 months.

Cumulatively over this period, the number of policies sold has declined 15% YoY. Assuming this continues in March, FY25 will see the lowest number of life insurance policies sold since FY17!

Normalcy has returned to the wireless telecom sector. After 5 consecutive months of subscriber loss, December (yeah, the data comes with a BIG lag) saw a net increase of 2 million subscribers. Both Jio and Airtel gained subscribers while Vi and BSNL lost subscribers. So status quo is restored.

Cumulatively in the past 6 months (2H2024), the wireless operators lost 20m subscribers and the majority of the loss was in rural areas, which is not surprising given that the loss was triggered by steep price increases. Rural areas saw a 12m or a 2% decline in the wireless subscriber base in the last 6 months. Urban areas saw an 8m or a 1% decline in the wireless subscriber base during this period.

That’s it for this week. See you next week.