Liquidity, Credit growth, Interest Rates and more...

This Week In Data #51

In this edition of This Week In Data we cover:

Tight money market liquidity

Uptick in credit growth

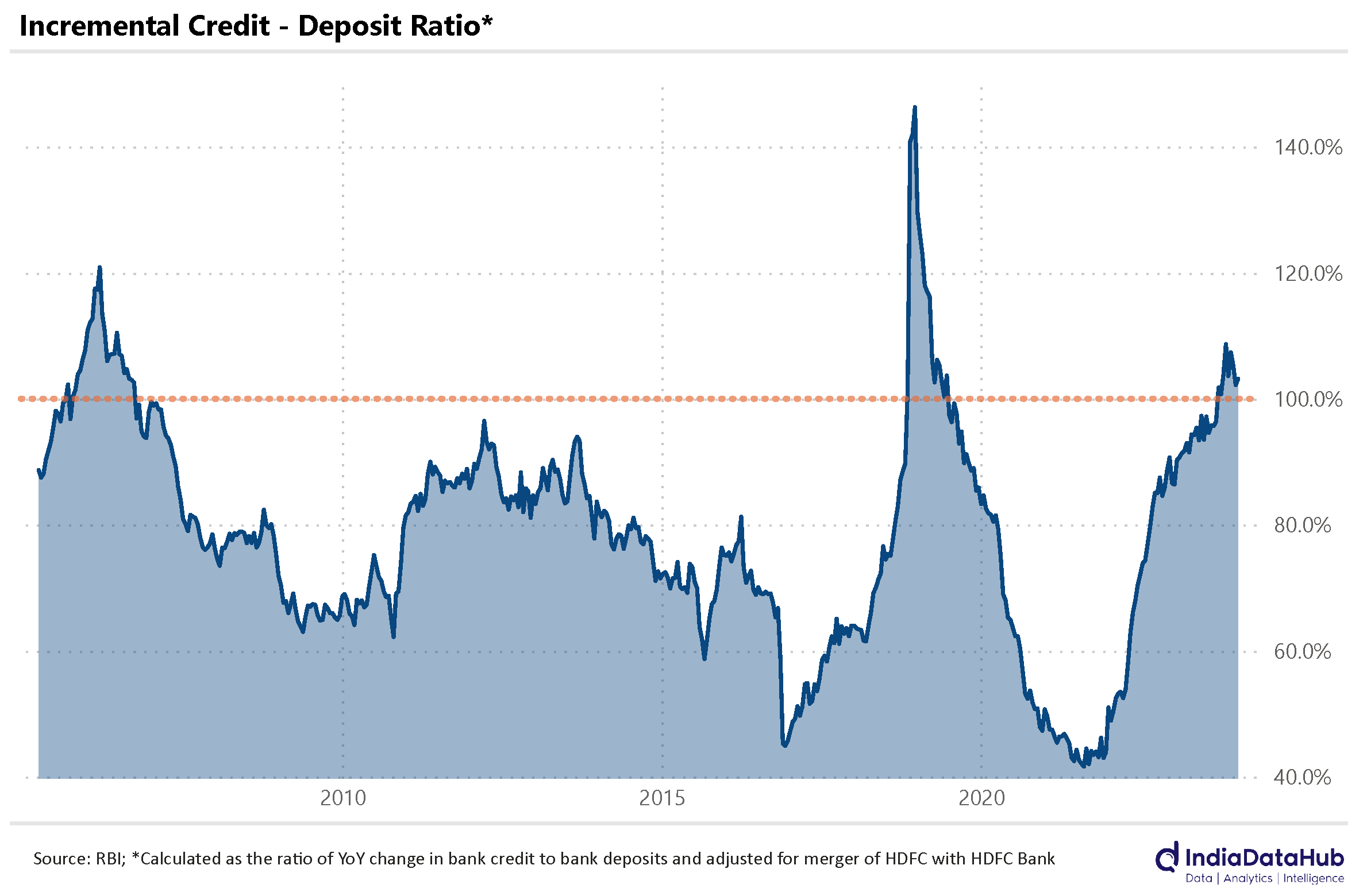

Elevated credit-deposit ratio

Sectoral credit growth

European rates

US GDP growth

In case you missed, we launched a major update to your Mutual Funds app where we now cover portfolios of almost 1200 individual schemes, covering all large fund houses. We will cover the remaining 250 odd schemes by March and start building analytics from next month. You can get a quick overview from this linkSo, liquidity. Domestic money market liquidity has become unusually tight in the last few days. The overall liquidity deficit crossed Rs3 trillion in this past week, the highest on record. The overnight money market rates have thus continued to remain above even the MSF rate at ~6.8%. While the spike in liquidity in the last week was unusual, the overall liquidity deficit has been trending upward for the past three months. Accordingly, January will be the third consecutive month when overnight rates will be higher than even the SDF rate.

The RBI has responded by offering Rs2.5 trillion under a 15-day repo auction last week which was oversubscribed by over 20%. The weighted average yield at the auction was 6.73%, only 2bps lower than the MSF rate. So, this auction will by itself not materially reduce either the size of the deficit or the level of the overnight interest rates. The only thing it will do, temporarily at least, is reduce the size of the daily borrowings under the MSF – effectively banks will not have to scramble daily to borrow from the RBI.

Repo auctions though are though just a temporary source of liquidity. The liquidity added through this auction will reverse after 15 days. Open market operations and FX intervention are the two permanent sources of liquidity infusion. And we have not seen much by way of either recently. In October and November, the latest period for which we have data, the RBI was a net seller of USD. Its FX operations were thus adding to the liquidity deficit. And RBI hasn’t done any OMOs since the 1st of November.

And this brings us to credit growth. Credit growth has ticked up to 16% in the last few weeks, from just under 15% in October. Deposit growth meanwhile has decelerated to 12.4% YoY as of the first fortnight of January, the lowest since September.

Consequently, the incremental loan-deposit ratio (LDR), on a YoY basis, has crossed 100%. Effectively, the Banks are giving loans more than 100% of the deposits they are collecting. And the LDR has been above 100% since September. So banks have been giving out more loans than the deposits they have been collecting (on a YoY basis) since September.

As the chart above shows, incremental LDR being above 100% is not very common. The last time this happened was in late 2018 and early 2019 and before that in 2006. The only way to keep on lending more than deposits is by first running down your investments if they are more than the regulatory minimum and then, borrowing. So, this in a sense is why the liquidity deficit has increased. And as explained earlier, the RBI has been unwilling, so far at least, to add durable liquidity to ease this deficit. Worth recalling is that in the last cycle (mid-2000s), the RBI used to frown upon banks running sustained high LDRs going as far as virtually singling out banks in public statements.

And the context for this is the sustained growth in personal loans, specifically the unsecured personal loans. Non-housing personal loans from Banks for example have been growing over 20% YoY for 18 consecutive months now (latest data as of November). And this is something the RBI has already flagged. In contrast, credit to Industry is growing in single digits and has been growing in single digits for the past year. So it is largely consumption which is driving credit growth.

So, if you add everything together, it does appear that the tight liquidity is in large part by design. After all, while we generally restrict the RBI’s mandate to be limited to inflation and growth, the legal mandate before the RBI is broader as the preamble to the RBI Act makes clear (emphasis ours). If anything, the preamble to the RBI Act, puts monetary stability above inflation and growth…

"...to regulate the issue of Bank notes and keeping of reserves with a view to securing monetary stability in India and generally to operate the currency and credit system of the country to its advantage; to have a modern monetary policy framework to meet the challenge of an increasingly complex economy, to maintain price stability while keeping in mind the objective of growth."Onto the rest of the World. The European Central Bank (ECB) held its Main Refinancing Operation Rate unchanged at 4.5% while the Bank of Turkey hiked its key interest rate again by 250 basis points to 45% to battle inflation. The latest inflation print in Turkey was 77% as of December.

The US Economy grew at a faster-than-expected in the fourth quarter. Real GDP increased at an annual rate of 3.3 % in the fourth quarter of 2023 (market expectation was for 2% SAAR), according to the advance estimate released by the Bureau of Economic Analysis. In the third quarter, real GDP increased 4.9 %.

So the US economy keeps chugging along even as the Fed has raised rates from close to 0% to 5.5%. This is once again likely to push out the expectations of a rate cut from the Fed. Not surprisingly, the Fed Fund futures are now assigning a less than 50% probability of a rate cut by the Fed in March.

Alright, the biggest event on India’s economic calendar, the Budget will be presented next week. It is also the event that has the highest noise-to-signal ratio. And given that the general elections will be in May, this will be an interim budget, so limited scope for substantial changes. So the odds are that this will be a non-event largely. But we shall see. We will do a high-level review next week.

Lastly, we are sad. Yes, we jinxed it for Novak. But every Mufasa has to eventually give way to Simba. And every Simba has to one day become a Mufasa. Djokovic is Mufasa. And in a philosophical sense, as long as this cycle is playing itself out (there is no Scar), we should be saying ‘Hakuna Matata’. So, on that note, we call it a day today. See you on the other side, next month!