Liquidity, Power Demand, Remittances and more...

This Week In Data #44

In this edition of This Week In Data, we discuss:

The tightness in domestic liquidity and its causes

Region dispersion of the sharp increase in power demand in recent months

Another strong month for outward remittances in October

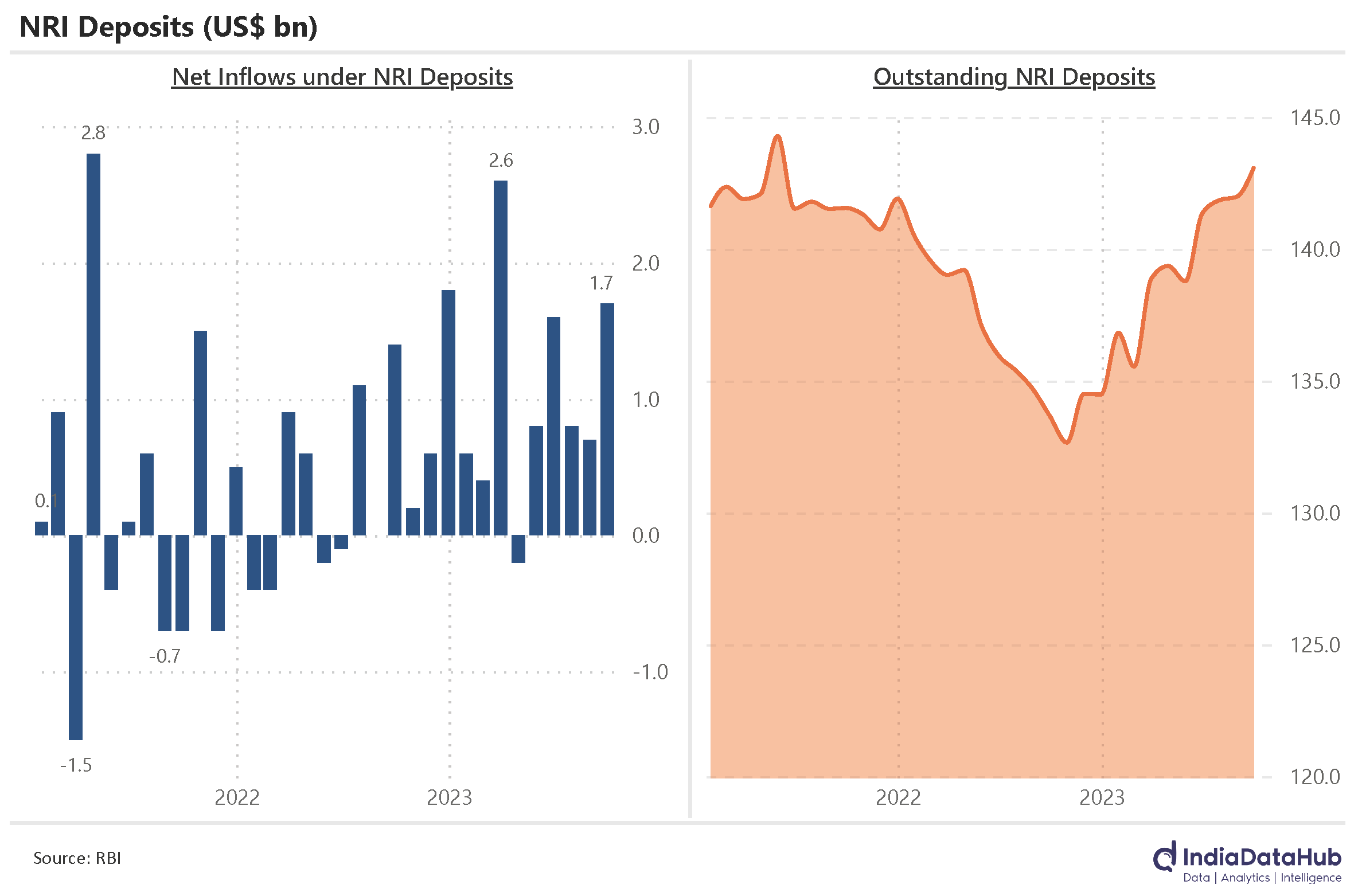

Pickup in inflows under various NRI deposit schemes

Domestic money market liquidity deficit has increased sharply in the last few days. This week (till Thursday), the deficit in the domestic money markets had averaged ₹1500bn, 2x of last week, which the RBI was supplying to balance the demand-supply. A fair part of this though is the Diwali effect as currency in circulation tends to increase leading up to Diwali and then gradually normalizes subsequently. And this year the increase in currency in circulation has been higher than last year. In the last three weeks (27th Oct – 17th Nov) the currency in circulation has increased by 1.7% or ₹520bn. During a similar period last year (7th Oct – 28th Oct), currency in circulation had increased by 0.8% or ₹250bn. And in 2019, during the Diwali period (11th Oct – 1st Nov) the currency in circulation had increased by 1.4% or ₹310bn.

This increase in currency in circulation will normalize over the next few weeks and this will ease the current liquidity tightness. The added unknown this year though is that currency in circulation is depressed due to the return of ₹2k notes to the banking system. Consequently, the currency in circulation which had been growing ~8% YoY in the middle of the year even after the uptick in November is still growing at just 4% YoY or half the pace. The experience of the demonetization of 2016 suggests that eventually currency in circulation will catch up to the trend and in that case, this will more than offset the return of festival-related seasonal increase in currency in circulation back to the banking system.

Power generation has seen strong growth in the last couple of months. And a fair bit of it has been attributed to erratic rains, seasonality in Diwali and so on. But now we have a regional composition of where the demand is coming from and that suggests another factor at play – Politics! To rejig memories, in the last 3 months (Aug – Oct) overall power demand in the country has grown by 17% YoY. In contrast, the prior three-month period had seen demand growth of 6% YoY.

This surge in demand has come largely from a handful of states. The three states that are going to elections currently – Rajasthan, Madhya Pradesh, and Telangana – have seen the fastest growth in power demand. Rajasthan has seen 20% growth while Madhya Pradesh and Telangana have seen ~25% growth. Andhra Pradesh, which is headed for election early next year has also seen a 20% growth in demand. But the biggest swing in power demand is from Karnataka, the state that just went to polls earlier this year. The last three months have seen 46% YoY growth in power demand. Among the states with no immediate elections, Gujarat and Maharashtra have seen strong demand growth at 20% and 25% respectively.

The new TCS regime on outward remittances under the RBI’s Liberalised Remittance Scheme or the LRS kicked in on the 1st of October. Not surprisingly, September, the last month before the new regime, was another strong month for outward remittances. Resident Indians remitted US$3.5bn under the LRS during September, 30% higher than last year. Cumulatively, in just the last 4 months, resident Indians remitted US$13bn outside India, an increase of 40% or almost US$4bn over the same period last year. Travel continues to remain the key head of these remittances with over half the remittances in the last 4 months being for overseas travel (~US$6.7bn).

It will be interesting to see if this surge in remittances simply reflects the preponement of remittances to avoid the TCS (most likely scenario). In such a case, remittances should drop significantly in the next few months.

NRI Deposits have been seeing strong inflows this year. Till September this year (FY), net inflows under the various NRI deposit schemes totaled US$5.4bn, almost 2x of the inflows last year and the highest since 1HFY19! As of the end of September this year, outstanding NRI deposits with Indian banks totaled US$143bn. While this is higher than last year, this is practically the same as in 2021. Though the second half of 2021 and most of 2022, India had not received much by way of inflows under the NRI deposit schemes.

That’s it for this week.