Lower Capex, Weak Auto sales, Resilient power generation and more...

This Week In Data #70

In this edition of This Week In Data, we discuss:

Lower government capex in the first two months of the year despite strong tax growth

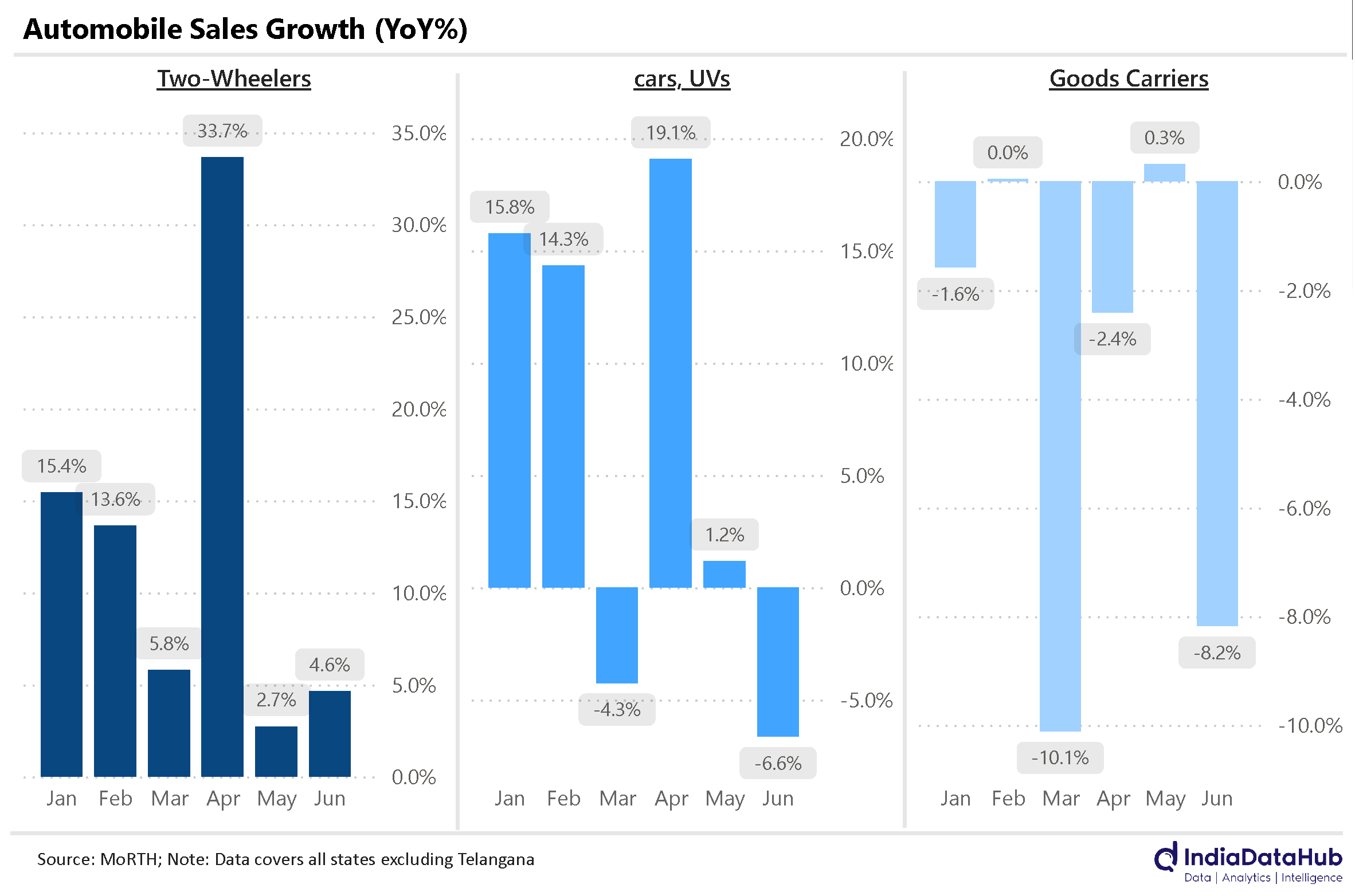

Automobile sales were generally weak across the board for the second consecutive month in June

Petrol and Diesel consumption growth remained soft in June

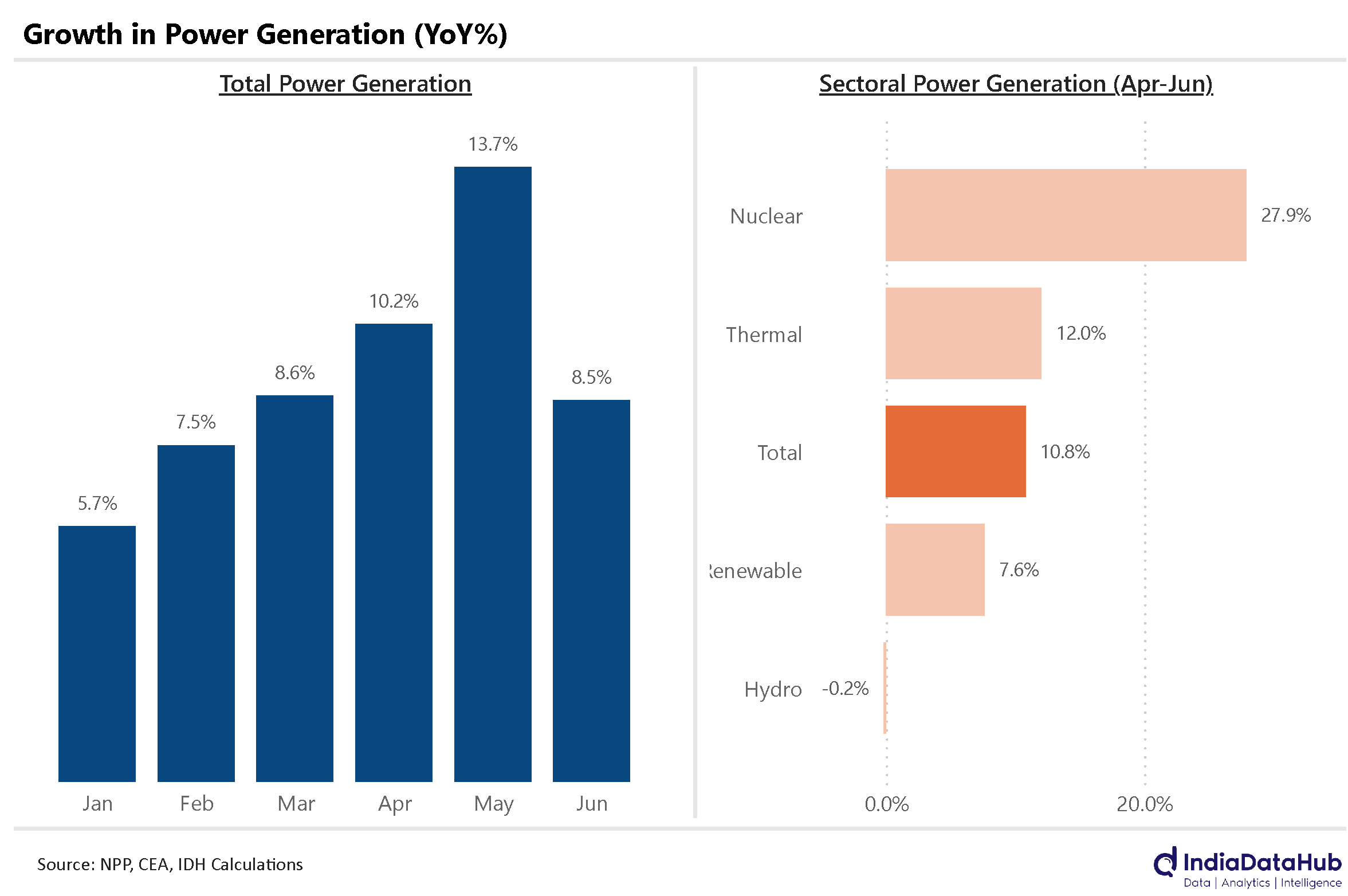

Power generation remains strong driven by thermal and nuclear

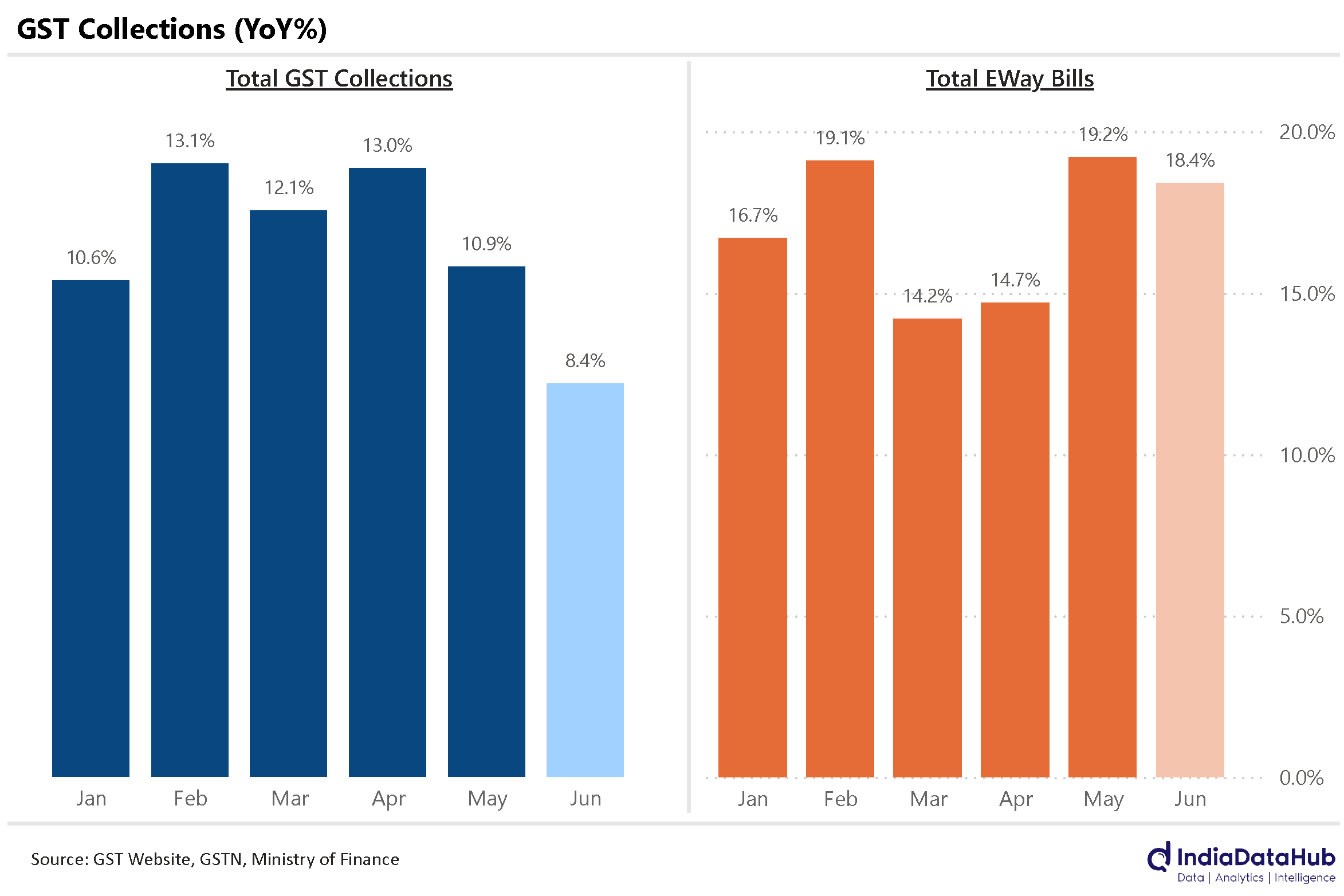

While GST collections softened, EWay bills continue to see strong growth

Continued strong labour market data in the US

Turning point (finally!?) in the interest rate cycle?

First week of the month and that means a lot of data to cover. We start with government capex. And it has got off to a slow start, largely due to the elections. The combined capital expenditure of the Central and the State governments (basis the data for 18 states), declined 14% YoY in the first two months of this financial year with both the Centre and States seeing double-digit declines. This is despite tax revenue growth remaining strong in the low teens.

This decline is most likely to have been caused due to the disruption to normal government working due to the elections. If revenue growth remains strong through the year, and there isn’t a big shift towards populism, capex growth will pick up, and potentially, make up for the decline in the first two months of the year. The central government will present its budget later this month and that will set the context for what to expect for the rest of the year. We shall see…

Auto sales were disappointing in June as well. While 2W sales grew, Car sales declined. 2W sales grew just under 5% YoY, the second consecutive month of low single-digit growth. However, because sales were strong in April (34%), sales for the quarter were 13%, higher than during the March quarter when sales had grown 11%.

Car sales declined 7% in June and despite the close to 20% growth in April, sales for the quarter grew a modest 4% YoY, down from 8% during the preceding couple of quarters. Sales of Goods carriers also declined in June. And for the quarter as a whole also sales of Goods carriers have declined in the low single digits, the second consecutive quarter of decline. Similarly, sales of Buses and Construction vehicles also declined in June. Pretty much across-the-board softness in growth.

Petroleum consumption data was also soft in June. Both Petrol and Diesel consumption grew in single digits. Indeed, Diesel consumption has now grown in single digits for the third consecutive month. As we discussed here, almost 90% of the diesel consumption is now towards transportation. So softer growth in diesel consumption in an environment where diesel prices haven’t changed for over a year would imply softer growth in goods movement across the country. And to that extent, it is in sync with the decline in the sales of goods carriers in recent months. And it is perturbing.

Power generation though remains strong, although sequentially growth decelerated to ~8% YoY in June. For the quarter as a whole, power generation grew ~11% YoY, almost 4ppt higher than during the March quarter. After rising in May, hydro power generation declined sharply in June. Hydro power generation in June this year was the lowest since June 2018! While thermal power generation continues to grow faster and pick up this slack, nuclear generation has also picked up sharply in recent months. Nuclear power generation has grown over 25% YoY in the last three months. This has been driven by a 1400MW (~20%) addition in nuclear capacity since May last year.

GST collections also moderated in June to single digits, the lowest growth since the early part of the pandemic. That said, the GST collections in June pertain to economic activity in May and given that May data was soft across the board, this is not particularly surprising. What is surprising though is that even as recent economic data has generally been soft, the one exception to this is the GST EWay bills. GST EWay bills grew 18% YoY in June and they had grown 19% in May. This is higher than the growth in the first 4 months of the year when it had averaged 16% YoY.

So, on balance, June has so far also seen soft data prints with EWay bills being a notable exception. This will flow through to the reported GDP growth for the quarter (end of August). More importantly, though the next MPC meeting is a month down the line and early data for July will be available for the MPC members before they make their rate decision. If data for July also remains soft, then this will almost certainly result in a change of policy stance from the MPC. And possibly also reflect in the corporate results for the June quarter resulting in some earnings downgrades.

Ok, let's shift gears to the rest of the world. The U.S. Bureau of Labour Statistics (BLS) released the non-farm payroll data yesterday. The US economy added 206k non-farm jobs in June on a seasonally adjusted basis as against a market expectation of 191k. So the US job market continues to churn out jobs.

But lo and behold, despite this, the US markets now strongly expect a rate cut from the Fed in September. The Fed fund futures are now implying a 78% probability of a rate cut in September – a month ago, the implied probability was below 70%. So the rate cycle might finally be starting to turn.

But before we close here’s some food for thought. We had a change of government in the UK this week and the exit polls were surprisingly accurate. The exit poll predicted that the Labour Party would win 410 seats – they won 412 seats! And this is despite the UK also having the first past the post system which makes conversion of vote share into seats a tricky business in what was a 3 or 4-cornered race this time. The key reason as per a report in the NYTimes seems to be that since the early 2000s, there have been no competitive exit polls in the UK. All three major broadcasters (BBC, Sky and ITV) pool resources and conduct a single exit poll with a fairly rigorous methodology. The methodology is also different in that the focus is not on estimating vote share but rather on change in the vote share. Head over to the NYT for more.

That’s it for this week. Have a good weekend folks. And if you are where it is raining a lot, binge on cutting chai and pair it with a vada pav or two (or three😊)…

Thanks for putting in all these efforts.