Lower CPI, WPI, Trade balance and more

This Week In Data #53

In this edition of This Week In Data, we discuss:

The decline in CPI inflation in January

WPI Inflation and commodity prices

Decline in merchandise trade deficit

Sticky US CPI

Headline CPI Inflation moderated to a 3-month low of 5.1% YoY in January from 5.7% in December. There have been two moving parts of inflation in recent months. Food inflation has been volatile. It had moderated to 3% in May last year from where it spiked to 10.6% in July. It moderated to 6.3% by October but then again spiked to 8.7% by December. In January food inflation moderated to 7.6%. But the non-food inflation has been steadily moderating. In January CPI excluding food and beverages declined to 3% YoY, the lowest in the last few years.

The lowest that the non-food CPI has been (under the current series), was 2.8% for a couple of months in 2019. So, it is hard to say how much further the non-food CPI can moderate, especially if growth remains strong. But food inflation is still elevated relative to its long-term average and thus even if non-food inflation may not moderate further, food inflation can moderate and thus there is further downside to headline CPI inflation. A 2ppt moderation in food inflation will push down headline CPI by ~1ppt.

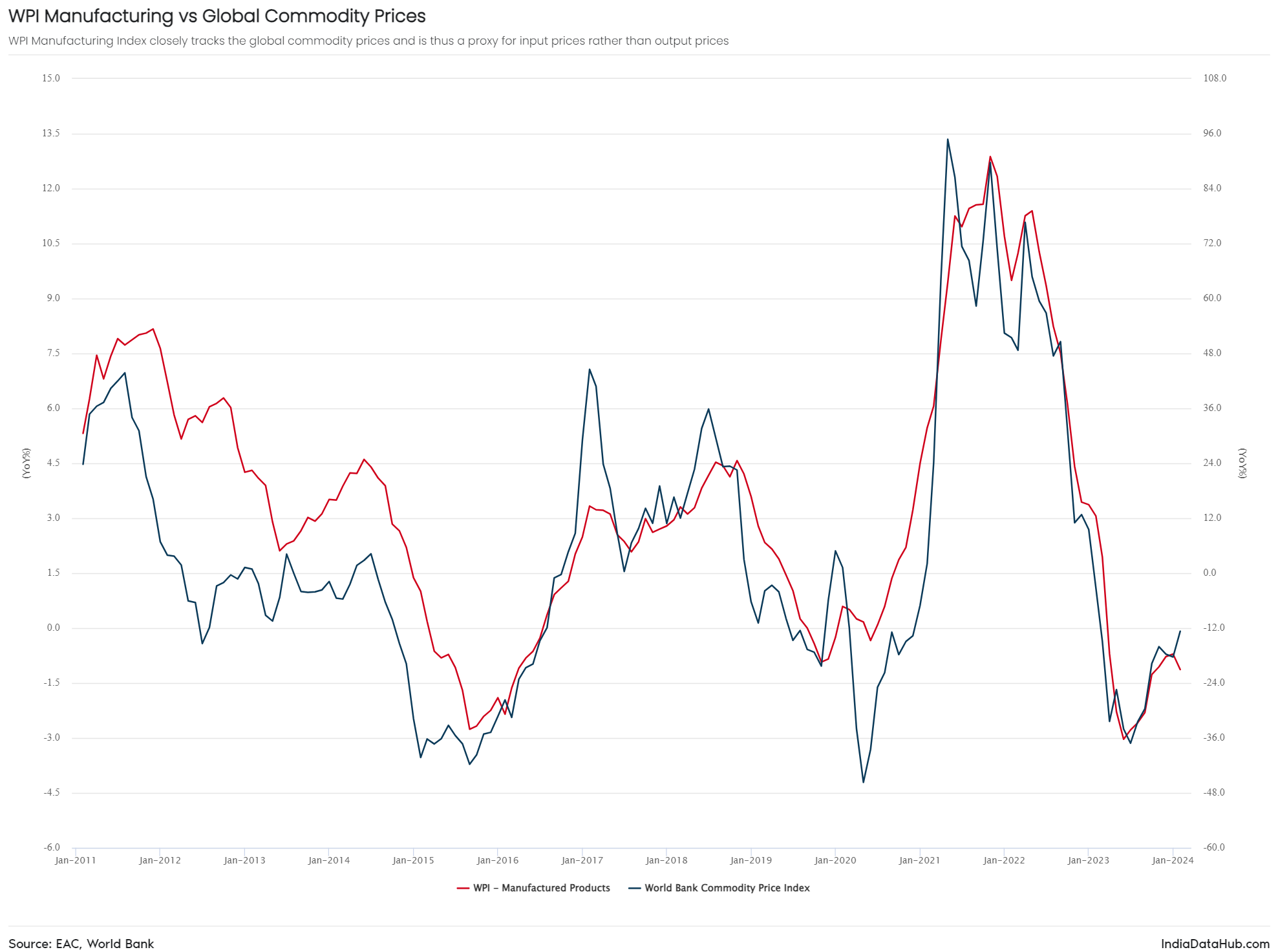

The other inflation metric in India is the Wholesale Price Index or the WPI. Before we shifted to the inflation targeting framework, based on the CPI, in 2016 the RBI would use the WPI as an important price gauge. The problem with the WPI though is that it largely mimics the commodity prices which are entirely outside the realm of monetary policy. Even in the case of manufactured goods, as you can see in the chart below. The correlation between the World Bank’s commodity price index and the WPI Manufactured goods has averaged almost 90% since 2011. So, all that the WPI tells us, from a price perspective, is what the commodity prices are doing and thus what cost pressures the businesses are facing.

But because it tells us what cost pressures businesses are facing (from commodity prices), it in a sense becomes an input for the CPI inflation. Both the headline WPI as well as its manufacturing component (~65% weight) have been hovering around 0% on a YoY basis for the past few months. Effectively, implying that the commodity price environment remains benign and that is positive from a CPI perspective.

Both (merchandise) exports and imports grew in January and they both grew by broadly the same amount, 3% on a YoY basis. The trade deficit moderated to US$17.5bn in January, the lowest since April last year, and almost flat on a YoY basis. From a currency perspective, this is a positive.

Electronic goods continue to be the key driver of export growth. But the growth rates have moderated from the 40-50% YoY seen at the start of last year to just 9% YoY in January 2024. Engineering goods, Pharmaceuticals and Iron ore were the other categories that saw strong growth in exports in January. On the flipside, electronic imports grew by over 25% YoY in January suggesting robust domestic consumption demand. However, imports of machinery declined. Gold imports more than doubled and Coal imports also rose over 20% YoY.

Globally also it was an inflation week. The US Bureau of Labour Statistics reported that the US CPI declined by 30bps to 3.1% in January. While CPI has dropped sharply from the first half of last year, it has remained sticky at around 3% since the middle of 2023. US CPI Inflation was last below 3% in March 2021 – almost 3 years ago. The UK also reported CPI inflation of 4% for January, almost unchanged from December. It is not just the US where CPI inflation has remained sticky.

Not surprisingly, this sticky inflation has meant that markets are no longer expecting a rate cut from the US Fed in May. And partly because of this (along with resilient domestic growth), the Monetary Policy Committee in India is unlikely to cut rates anytime soon even though the domestic inflation trajectory is reasonably benign now.

That’s it for this week. Have a good weekend.