Lower Inflation, Declining Exports and Inflows in Fixed Income Funds

This Week In Data #13

In this edition of This Week In Data we discuss

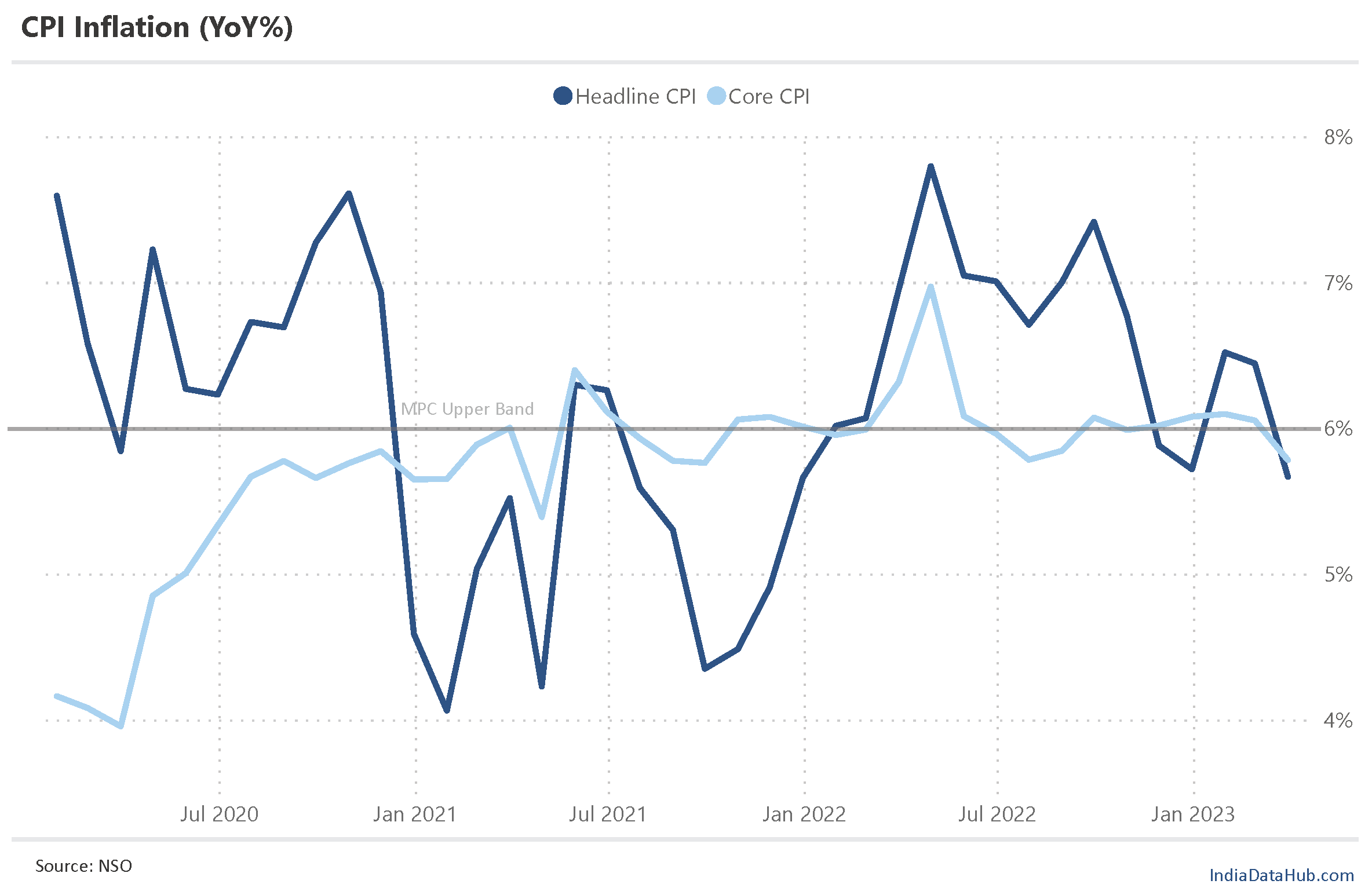

The decline in CPI Inflation in March

Decline in Exports in March and why it may be overstated!

The outsized inflows in some fixed income MF schemes in March

As expected, CPI inflation moderated sharply to 5.7% YoY in March from 6.4% in the prior month. The moderation was in line with the consensus expectation. Lower food inflation and also lower core inflation both contributed to this moderation.

Food inflation has been the key driver of volatility in recent inflation readings. And in sync with that after rising sharply in January and February, food inflation fell and is back to where it was in November-December. Of the ~70bps decline in headline inflation in March, ~50bps is attributable to lower food inflation. That said, unlike in Nov-Dec, the moderation in food inflation was broad-based. Cereals and Milk inflation which had been rising for several months saw a dip. Meat, Oils and Processed food also saw a dip in inflation. Vegetable inflation remains in negative territory and from a short-term perspective that remains the key risk given that we are approaching the summer months which could potentially see volatility in Vegetable prices.

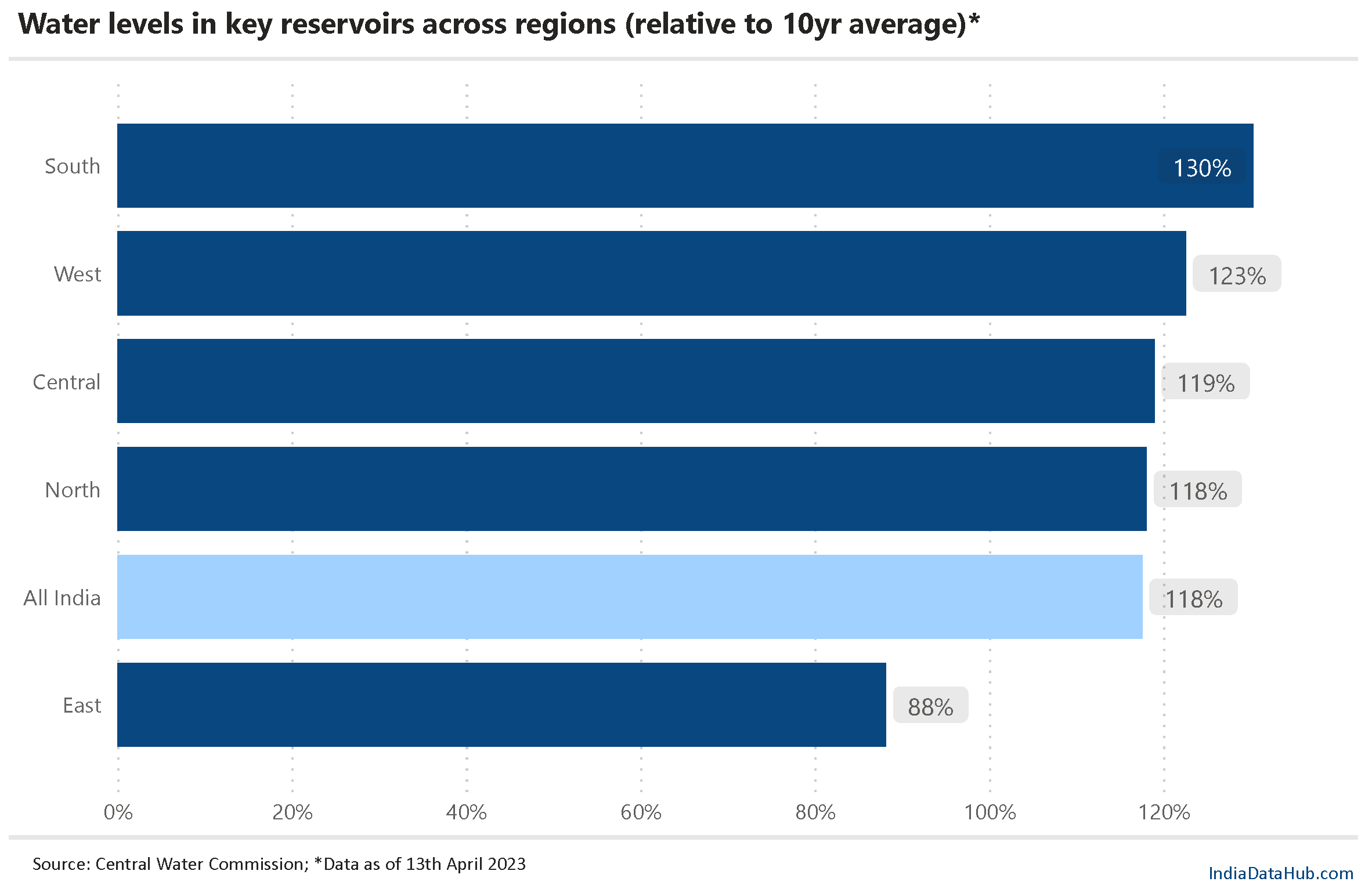

From a slightly longer-term perspective though, unfavourable rainfall is the key risk for food inflation. While the IMD has forecasted for a normal monsoon, private weather forecaster Skymet has forecasted for a below-normal monsoon. On the positive side, reservoir levels are currently 18% above the long-term average, except in Eastern areas where they are almost 12% below. To some extent, this can partially offset a lower rainfall. Further, Wheat stocks with the FCI (as of early March) are half of what they were last year and close to the buffer stock level. The FCI would thus have to step up procurement this year reducing the marketable surplus. Thus, this month's decline notwithstanding, food inflation remains a key upside risk.

Lastly, it is worth noting that despite this moderation, inflation is back at the level it was in December and is only 30bps below the upper limit of RBI's tolerance. Given that CPI had printed 7% in March last year, a 5.7% reading this year makes the 2-year Cagr in CPI well above 6%. We are thus still some way away from being in a low-inflation environment.

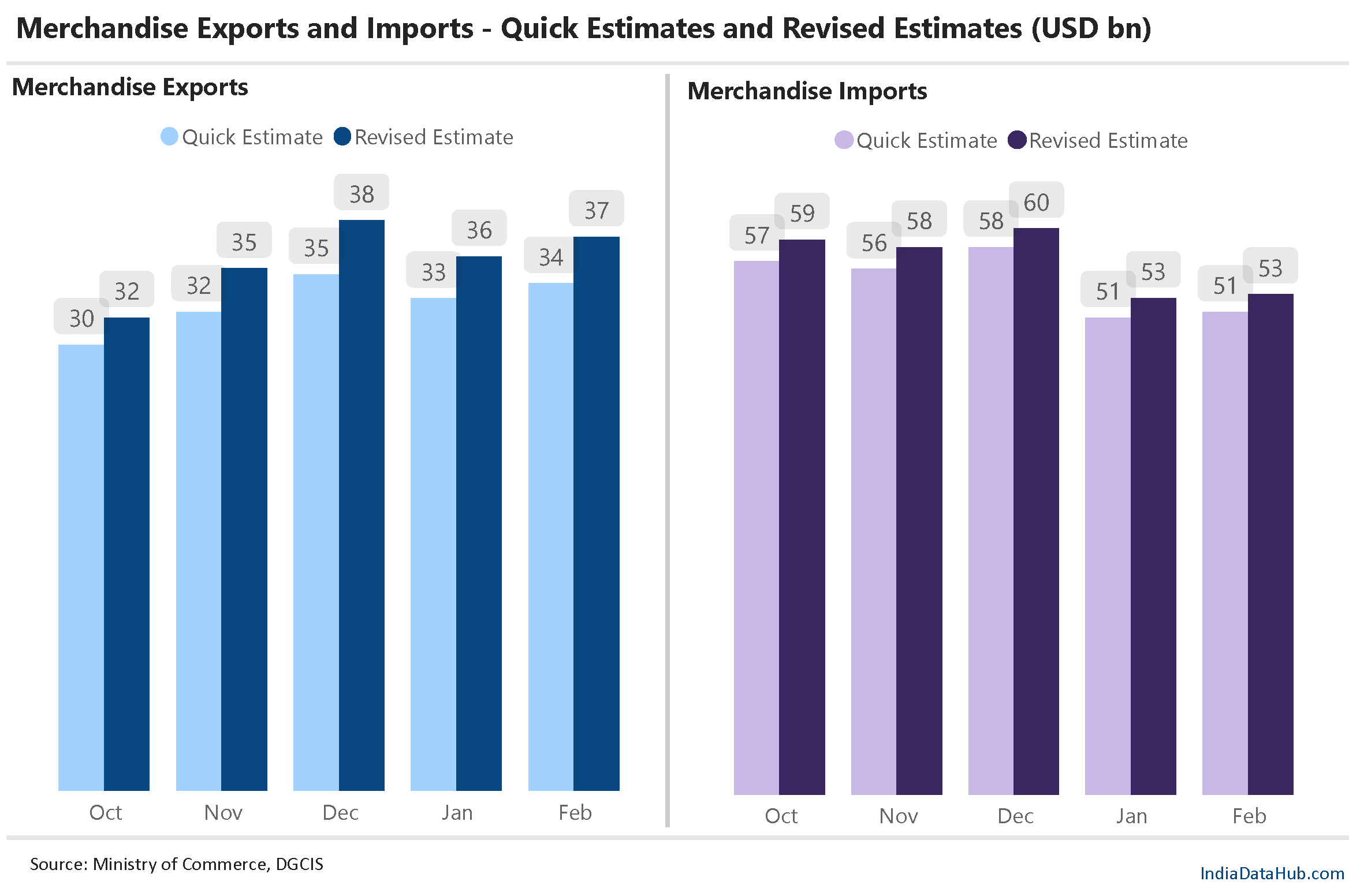

The government released the quick estimates of Merchandise trade for March yesterday. As per the release, exports declined 14% YoY to US$38bn in March. This is the 4th consecutive month of decline in exports and the 5th month in the last 6 that exports have declined. As per the quick estimates.

The reason for the emphasis on quick estimates is that this is provisional data. India’s merchandise trade data comes in two flavors – quick estimates released by the Ministry of Commerce around the middle of the month and revised but detailed data released by the Directorate General of Commercial Intelligence and Statistics (DGCIS) around 3 weeks later.

And in the last few months, the revised data for both exports and imports (as released by the DGCIS) have been consistently higher than the quick estimates data released by the Ministry of Commerce. Effectively, the preliminary quick estimates data is understating the exports (and imports) performance. Consider January and February of this year. Export data as per DGCIS for these two months is ~9% higher (~US$3bn in each month) than the quick estimates released by the commerce ministry. Consequently, what was a 7% YoY decline in January turned out to be a 1% increase and similarly, what was a 9% decline in February turned out to be a modest -0.4% decline.

Given these trends, it is quite likely that the data for March will also see an upward revision and thus the decline in exports (and imports) will be much lower than what the commerce ministry data is suggesting. In conclusion, the point is that the export performance in the last few months has been much better than what the preliminary quick estimates data suggests and March ought to be the same. But we shall see in a few weeks!

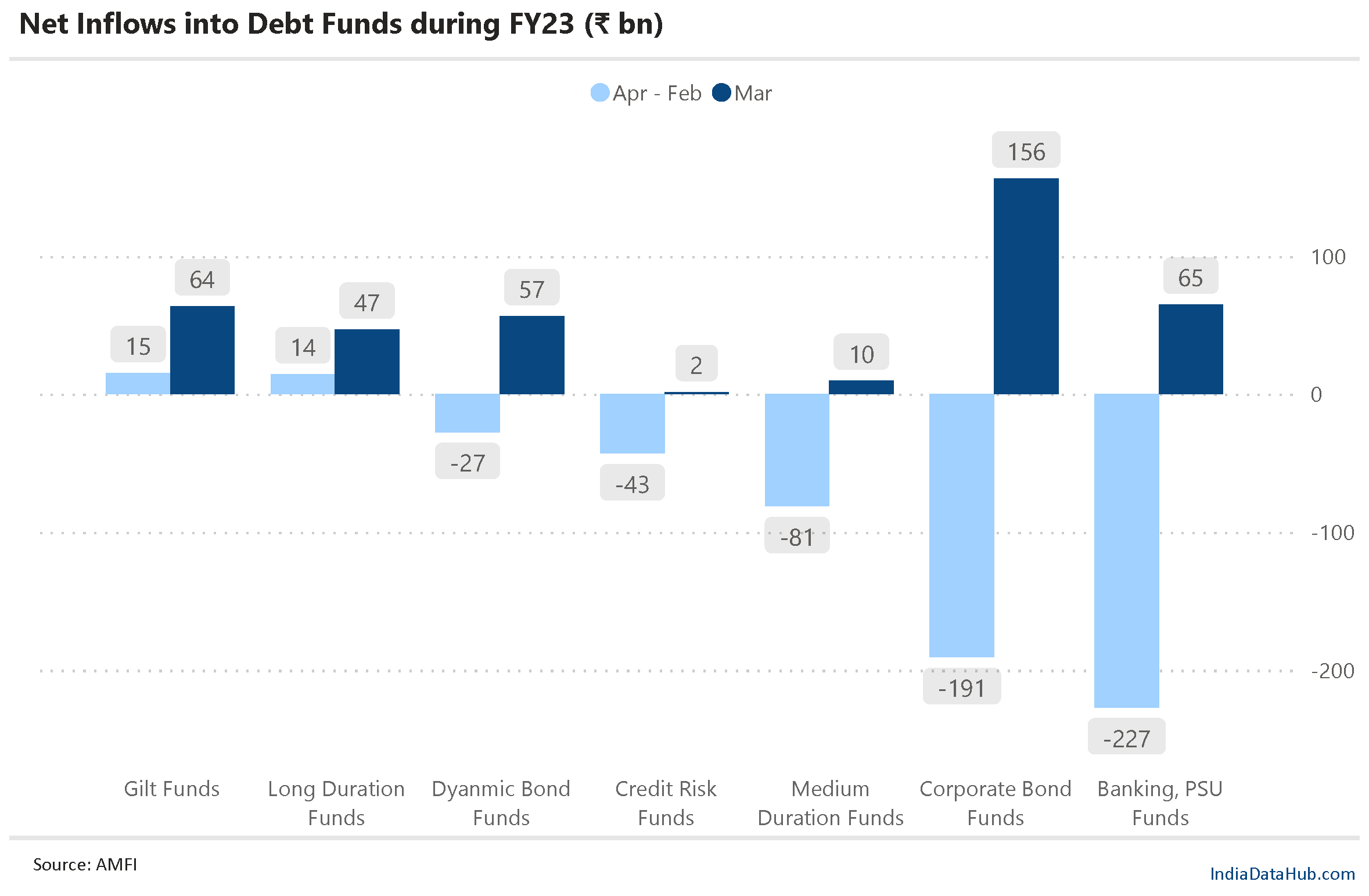

The last week of March saw a pretty big change in the taxation of fixed-income mutual fund schemes. The tax arbitrage that fixed-income mutual fund schemes enjoyed through a lower capital gains tax regime has been done away with (unfairly some would argue). The last date to enjoy the old tax regime was 31st March and the expectation was that there will be a huge inflow of funds into fixed-income schemes to lock in the old tax regime.

On the surface of it, this does not seem to have happened. Fixed income schemes saw an outflow of ₹540bn in March. This is more than the outflows in the preceding three months combined. However, there is a catch. March is a seasonally weak month for inflows in debt funds due to the large advance tax payments due in the middle of the month. So, March generally sees outflows. From that perspective, outflows in March this year were not very large. For reference last year in March (2022), fixed income funds had seen outflows of ₹1100bn or more than twice the outflows of this year.

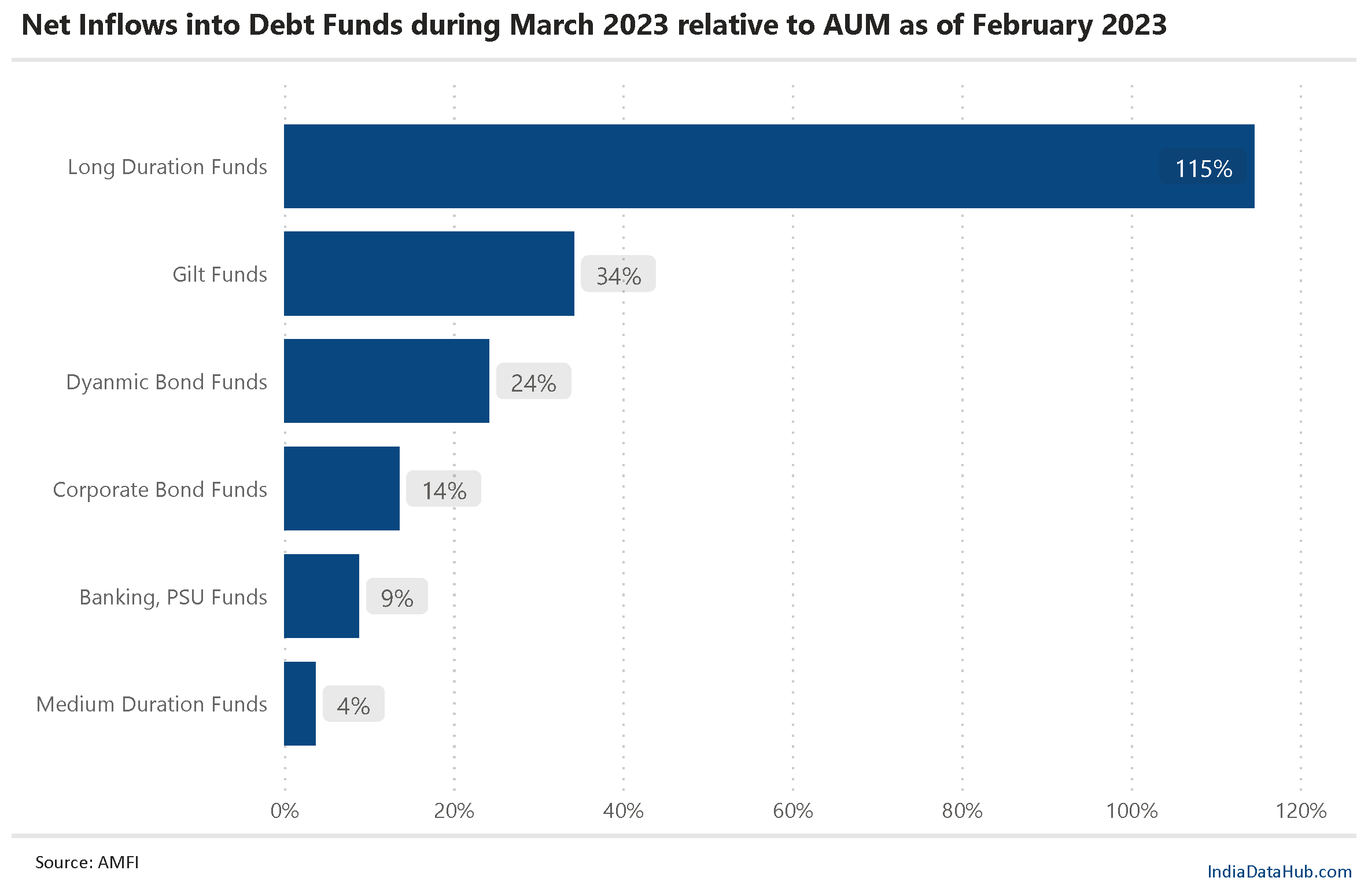

But going even a bit further, not all debt funds are the same. By and large, debt funds are dominated by short-term funds where corporates invest as part of their treasury management operations. For corporates, the change in the tax regime does not make any difference because their investment horizon is in weeks and months not years. Where the change in tax regime makes a difference is for individual investors who looked upon these funds as an alternative to bank FDs. And in these categories, March has seen a huge inflow in funds.

In Long duration schemes, for example, the inflows in March were more than the total AUM of that category as of February. In Gilt funds, inflows in March were just over a third of the AUM as of February and in Dynamic bond funds, inflows in March were a quarter of the AUM as of February. Bottom line, in the short run, the MF Industry was able to mobilise its distribution arms and get people to lock into the tax arbitrage in the last few days of the year.

Thats it for this week. See you next week!