Moderating Current Account, Weak Tax Revenues, Accelerating payment infra and more

This Week In Data #12

In this edition of This Week In Data we cover:

Moderation in Current Account Deficit

Weak Tax collections

Health core sector growth

Drivers of credit growth

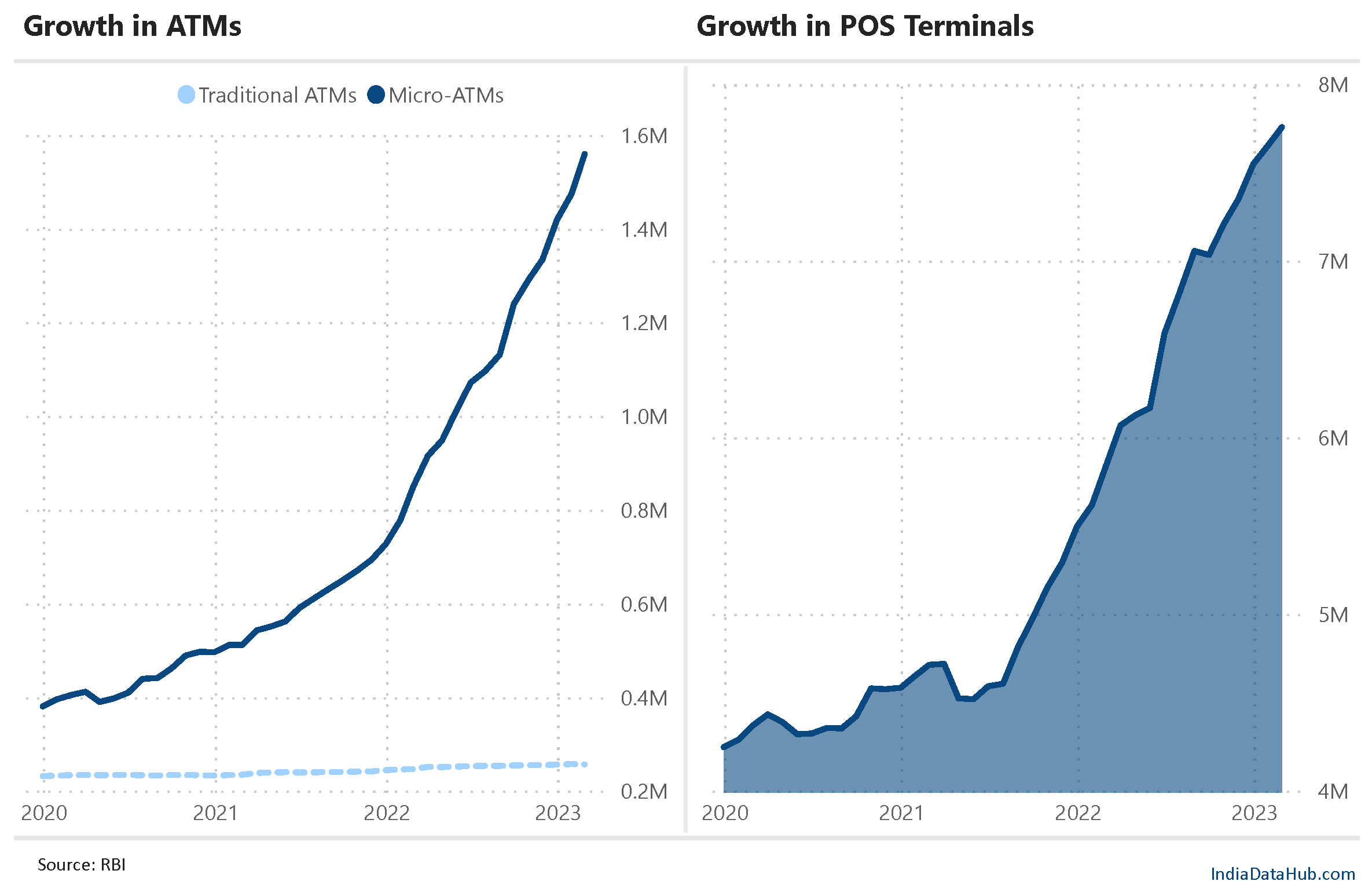

Accelerating payments infrastructure

Today’s edition of TWID is delayed. But that is because today happens to be a Friday as well as end of the month. And that means flurry of data releases in the evening. So, it has taken some time for us to process everything and brew this newsletter for you. There is a lot to cover, so let us get started…

The current account deficit moderated sharply to 2.2% of GDP during the December quarter from 3.7% in the preceding quarter. This moderation directly reflects the sequential moderation in the merchandise trade deficit and the improvement in the services balance. Given the current trajectory of the trade deficit, the current account balance is likely to turn into a surplus. However, as we discussed last week, the challenge is capital flows which are subdued and this is reflected in the relative underperformance of the rupee.

February was a weak month for tax revenues. Gross tax collections for the Central government grew a modest 4.5% YoY. Tax revenues have remained weak for 4 consecutive months during which growth has averaged 3% with no month seeing double-digit growth. Corporate taxes have declined by 1.5% during this period. Excise collections have also been declining and this has been offset by growth in Personal Income Tax, GST and Excise collections. And not surprisingly as revenue growth has slowed down, discretionary expenditure has taken a hit. Over the past 4 months, the Central government’s capital expenditure has declined 20% YoY.

Core sector growth grew 6% YoY in February. Like with other indicators, this is slower than the growth in January but higher than the growth in the second half of last year. The growth in February was driven by strong growth in Fertilisers (22%) and ~7% growth in Steel and Cement. Power generation also grew a strong 8% YoY. Over the past three months, core sector growth has averaged 7% YoY, the highest since August last year.

Credit growth has stabilised at ~16% YoY for the last few weeks. However, sectorally the trends are very divergent. The industrial sector is seeing the weakest growth. As of February, the sector has seen credit growth of 7% YoY. A year back when overall non-food credit growth was at 9%, Industrial sector credit growth was still at 7%. So over the past year, while overall non-food credit growth has picked up by ~7ppt, Industrial sector credit growth has remained stable.

What is driving credit growth is Services and Personal loans. Both sectors are seeing credit growing ~20% YoY. Over the past year, services sector credit growth has increased by 14ppt while personal loans growth has picked up by 8ppt. The uptick in services sector credit growth is largely due to Banks lending to NBFCs – and most of NBFCs lending is directed towards consumption rather than to the Industrial sector. So, on balance, it is consumption which is driving credit growth currently. Agriculture credit growth remains below average at ~15% but it has also ticked up by ~4ppt over the past year.

Earlier in the week the RBI released the payments data for February. We track the monthly trends in payments across categories and as expected overall payments growth moderated in February to 17% from 20% growth in January. This however is still higher than the low teens' growth in the last quarter of 2022. Transactions continue to grow faster than the value of payments. In February, overall transactions grew almost 50% YoY. And UPI continues to be the fastest mode of payment growing over 50% in value terms and 66% in volume terms in February.

The more interesting data, from a slightly longer-term perspective, though is on the Payment infrastructure. As the economy has recovered from the pandemic, the growth in payment infrastructure has also picked up. Since December-2021 for example the number of micro-ATMs has risen by 2.5x. There are now 1.55 million micro-ATMs in the country as against less than 300k traditional ATMs. Micro ATMs are deployed primarily in rural or semi-urban areas and thus are important from a financial inclusion perspective.

Similarly, the number of POS terminals has grown by 40% since the end of 2021. There are now almost 8 million POS terminals in the country as of February up from 5.5 million as of the end of 2021 and just over 4 million as of the end of 2019. POS terminals make it easier for merchants to accept different payment modes. Given that the major cities already have a reasonable penetration of card acceptance infrastructure, the incremental growth must be coming from smaller cities and towns. This thus also points towards the deepening of the payment’s revolution in the country.

That’s it for this week. More to cover next week. See you in FY24!