Oil prices at pre-war levels, Electronics exports moderating, record decline in LPG and more...

This Week In Data #166

In this edition of This Week In Data, we discuss:

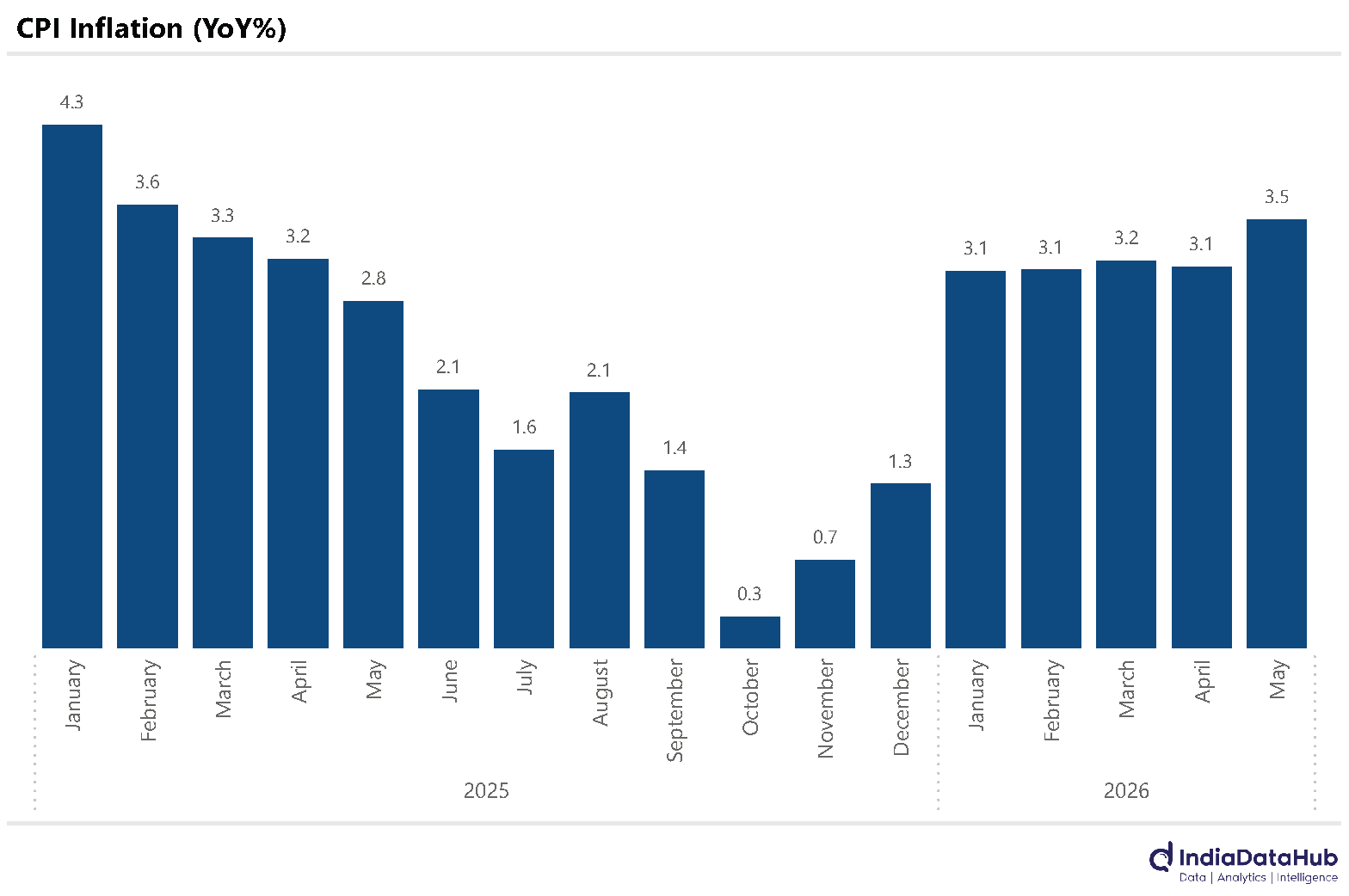

CPI Inflation rises with both Food and Non-Food ticking up

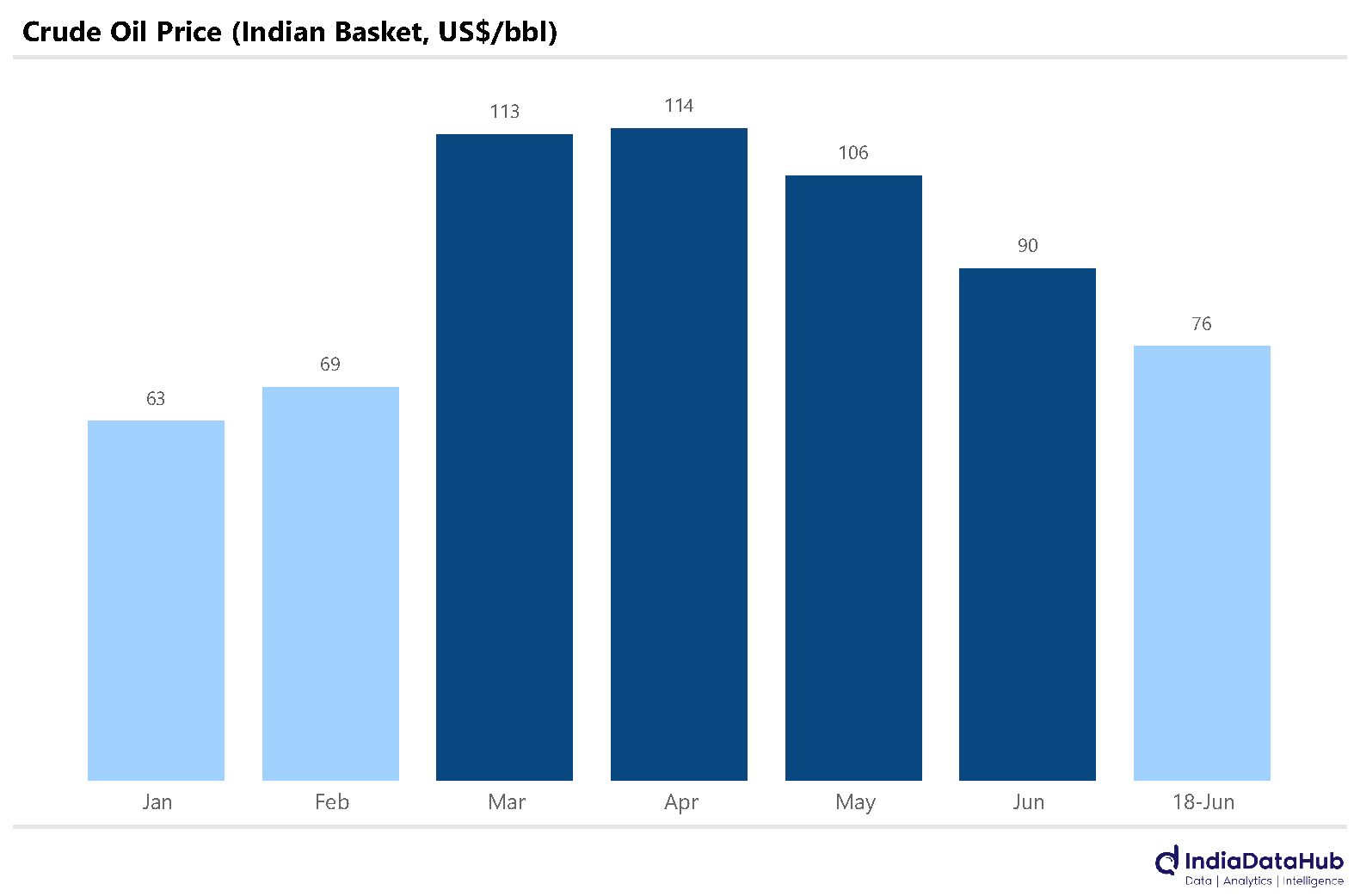

Oil prices are now almost back to pre Iran war levels

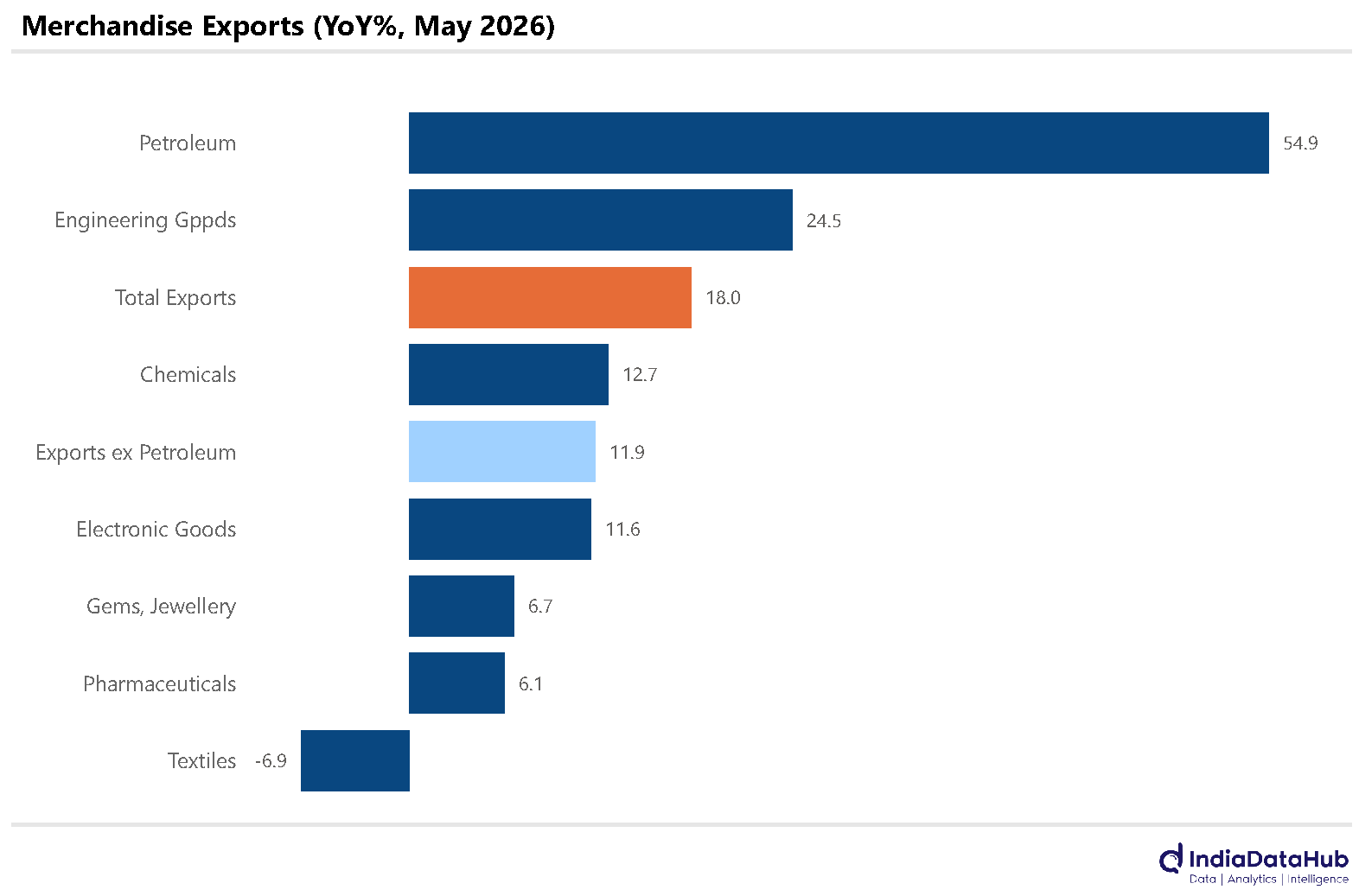

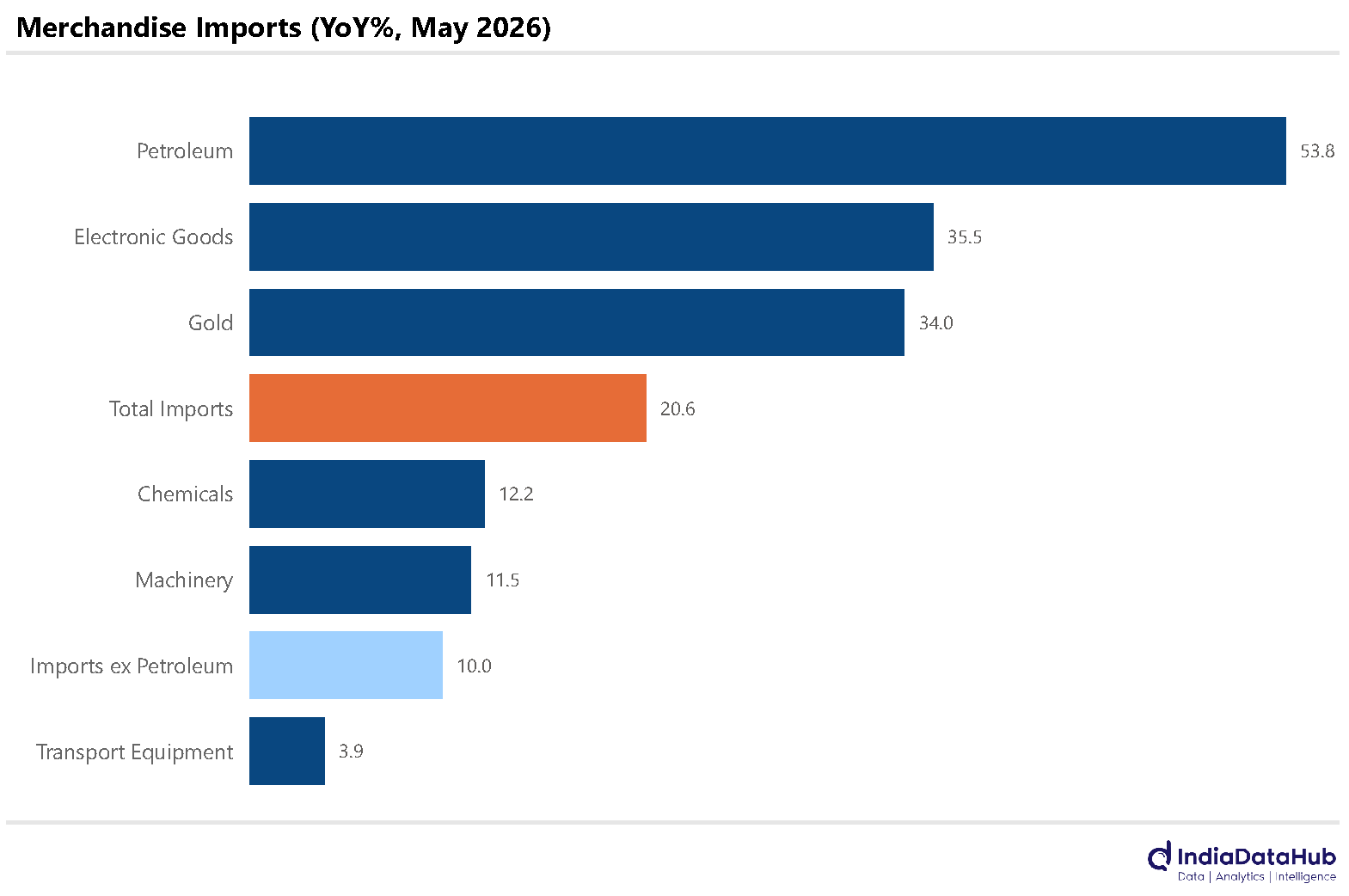

Exports and Imports grow strongly in May driven largely by Commodities - Oil and Gold

Electronics exports saw a slowdown and have grown slower than imports in Apr-May

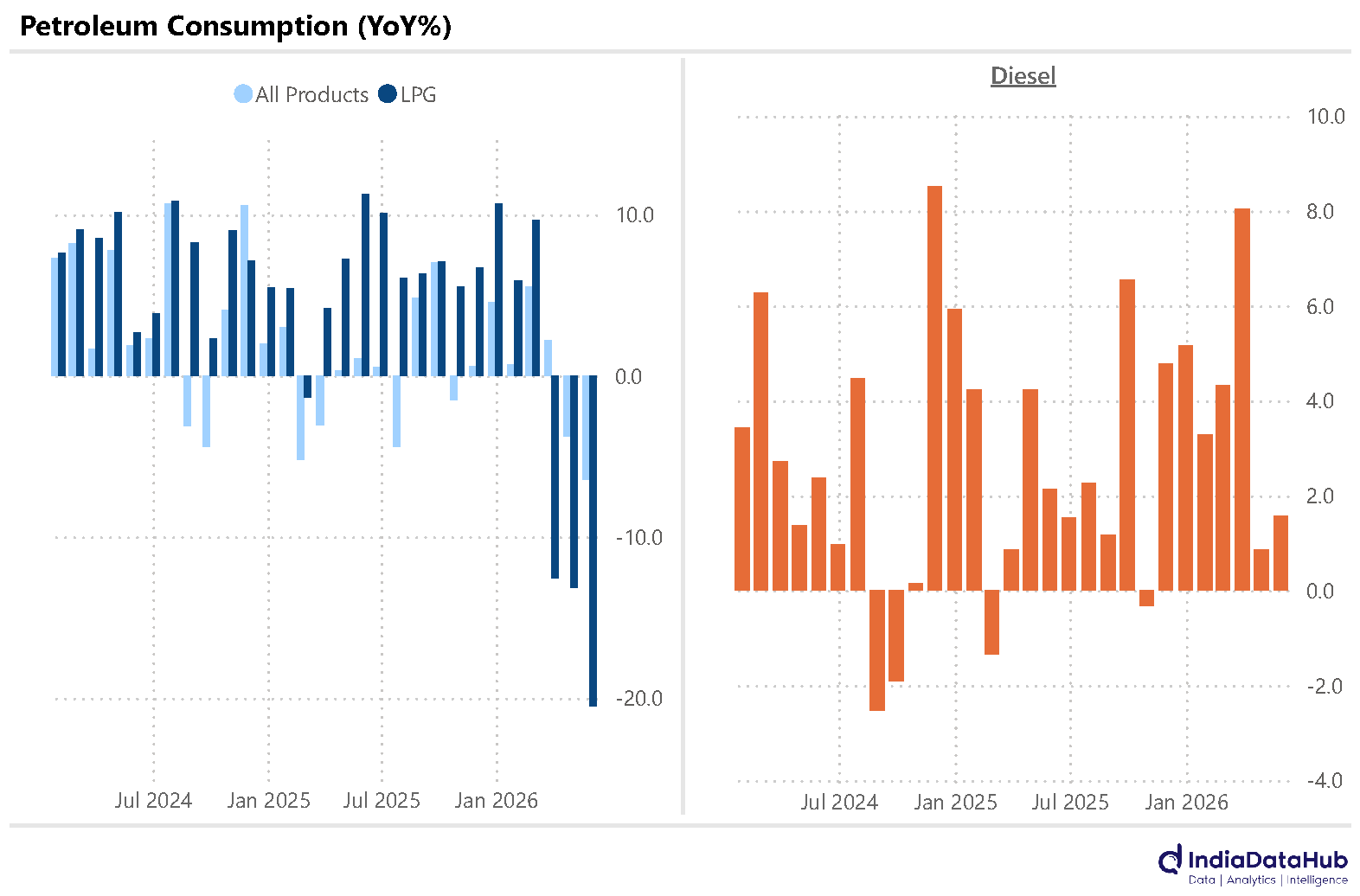

Consumption of petroleum products declined by over 7% in May, the shrpest decline in two decades driven primarily by LPG

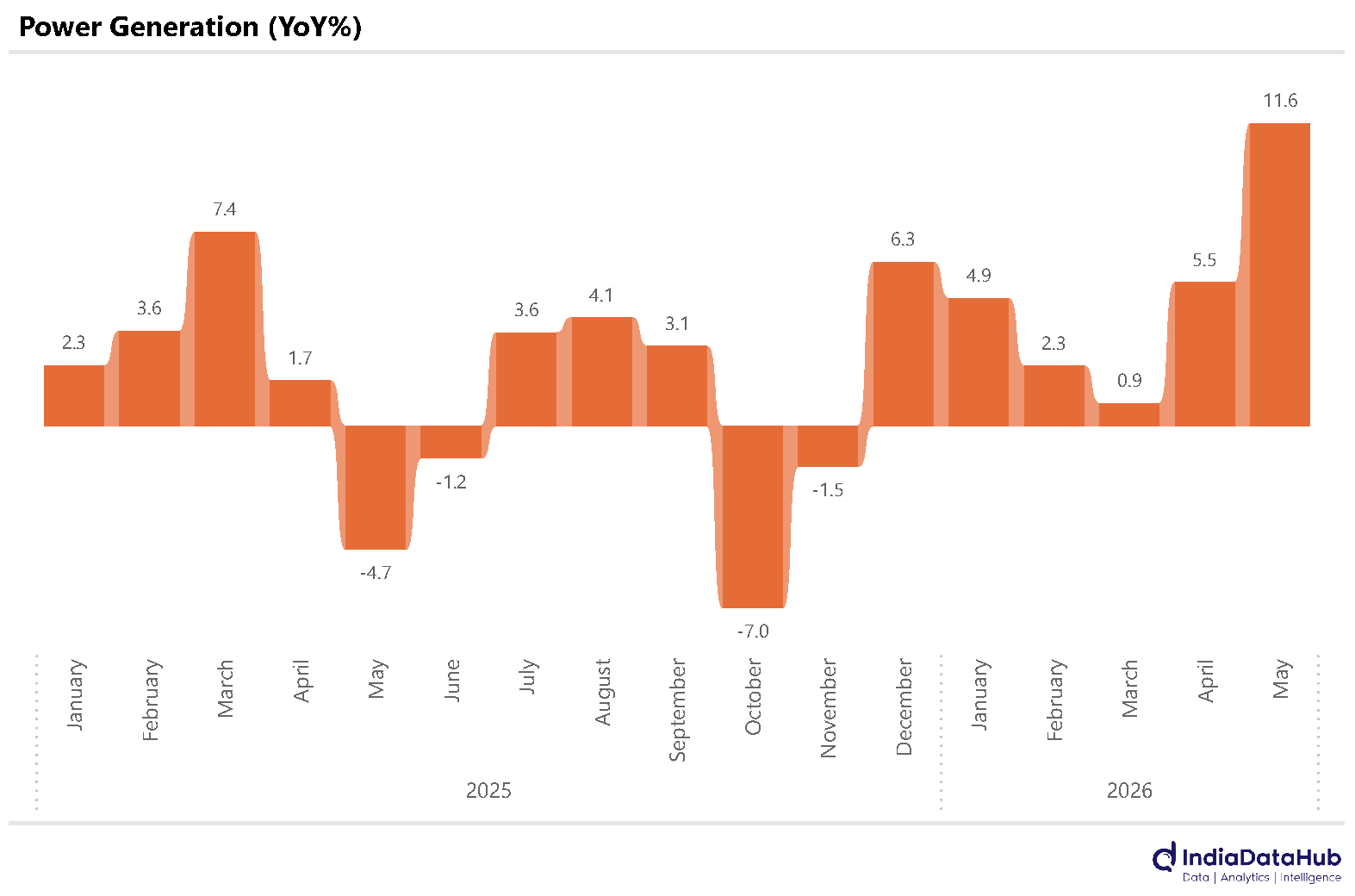

Power generation grew in double digits in May, driven by both renewable and thermal power

CPI inflation edged towards 4% YoY in May, rising to 3.9% YoY from 3.5% YoY in April. This is the highest level since February last year. Food inflation continues to be the key driver of headline inflation – it rose 50bps to 4.5% YoY in May. However, non-food inflation, which had remained stable around 3% for the last few months, also rose to ~3.5% YoY in May.

The good news, though, is that oil prices have corrected significantly in recent days. The price of the Indian basket of Crude oil, which had averaged ~US$115/bbl in March and April, has fallen to under US$90/bbl so far in June, and on Friday was closer to US$75/bbl. Before the hostilities started in the Middle East, the price of the Indian basket or crude oil was averaging US$60-65/bbl.

So, oil prices are now just 10-15% away from their pre-Iran war levels. Assuming this trajectory holds, this removes a key upside risk to inflation and the economy. The other risk – below normal rains – remains, and we will see how it plays out over the next few weeks.

Merchandise exports rose 18% YoY in May, the strongest growth in the last few months. This was driven by over 50% growth in Petroleum exports, excluding which export growth was a relatively modest 12% YoY. Engineering goods exports also saw strong growth of almost 25% YoY; exports of Electronics goods saw only a modest growth of 12% YoY. Textile exports declined YoY and were the key drag on export growth.

Imports saw an even stronger growth at 20% YoY in May driven largely by over 50% growth in Petroleum imports. Excluding Petroleum, imports grew 10% YoY. Gold imports rose by over 30% YoY in May, and even imports of electronic goods grew by over 30% YoY, a faster growth than the growth in exports.

Consequently, the trade deficit widened by over 25% YoY. That said, with Oil prices having fallen sharply now, as mentioned earlier, some of the worries over the trade deficit have subsided. The current account balance will still increase in FY27, but not as sharply as previously anticipated.

Domestic consumption of petroleum products declined almost 7% YoY in May. Outside of the Covid19 pandemic, this magnitude of decline was last seen in 2003, more than 20 years ago! And LPG continues to be the key drag – LPG consumption declined 20% in May, the third consecutive month of double-digit YoY decline and the sharpest decline on record. Outside of the last 3 months, LPG consumption has never declined in double digits in the last 3 decades for which we have monthly data – not even during the COVID-19 pandemic.

But the slowdown is across the board. Naphtha consumption has declined in double digits, as has Bitumen in the last two months. And while Diesel consumption has not declined, it has slowed to ~1% YoY in April and May, down from 5% growth during the Jan-Mar quarter. Even the growth in petrol consumption halved to just over 3% in May from almost 7% between January and April.

Lower petroleum consumption and soaring temperatures are driving up power generation. Power generation grew 12% YoY in May as per provisional data, the highest growth in recent years. While renewable power generation grew over 30% YoY, even thermal power generation grew by almost 9% YoY, once again, the highest in recent months.

Given that monsoon rain is delayed this year, June also promises to see strong growth in power generation.

That’s it for this week. See you next week…