Power generation, Power capex, Weak Diesel demand and more...

This Week In Data #64

In this edition of This Week In Data, we discuss:

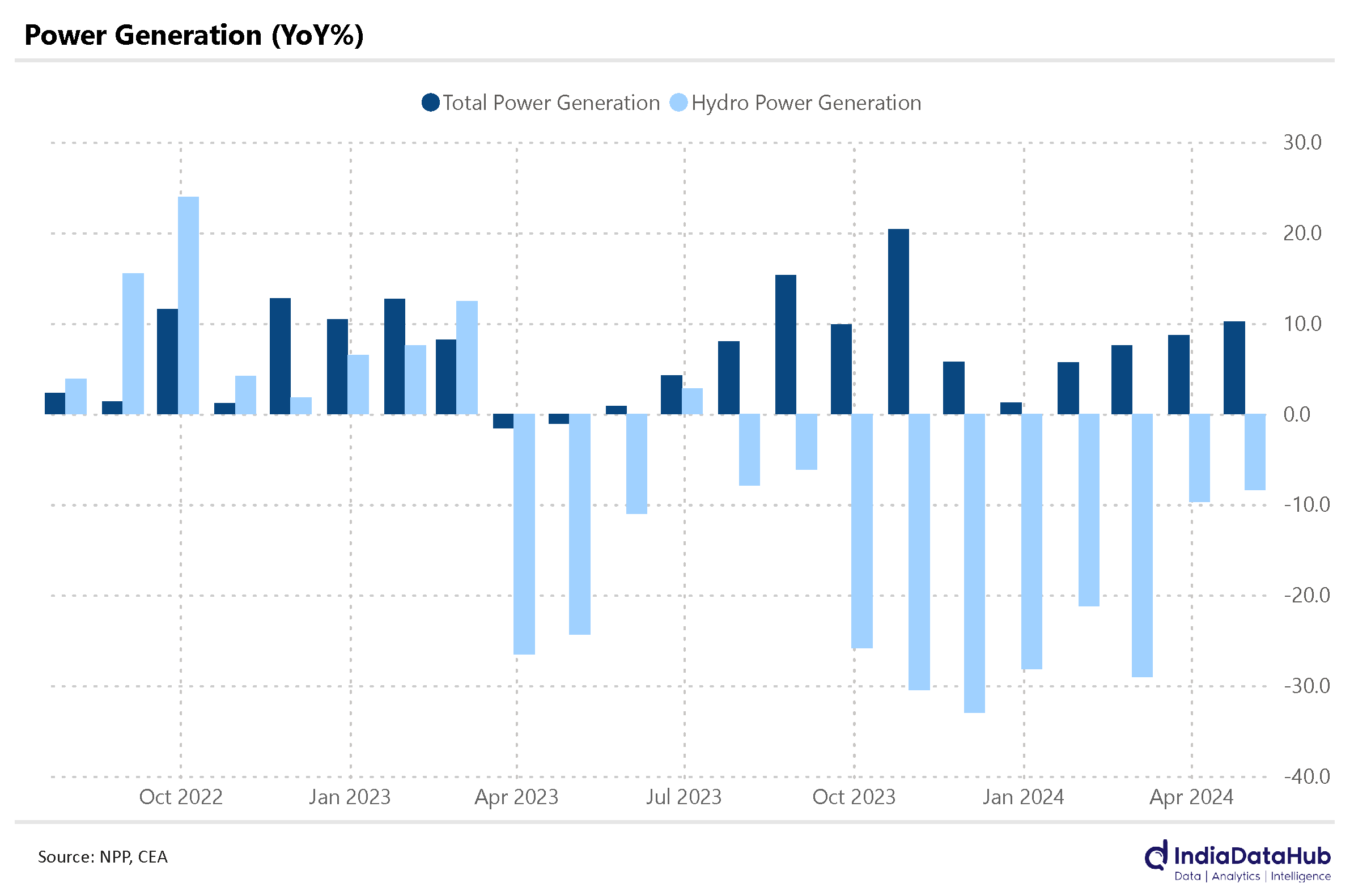

Strong power generation in April despite continued decline in Hydro

Sharp recovery in Thermal PLFs

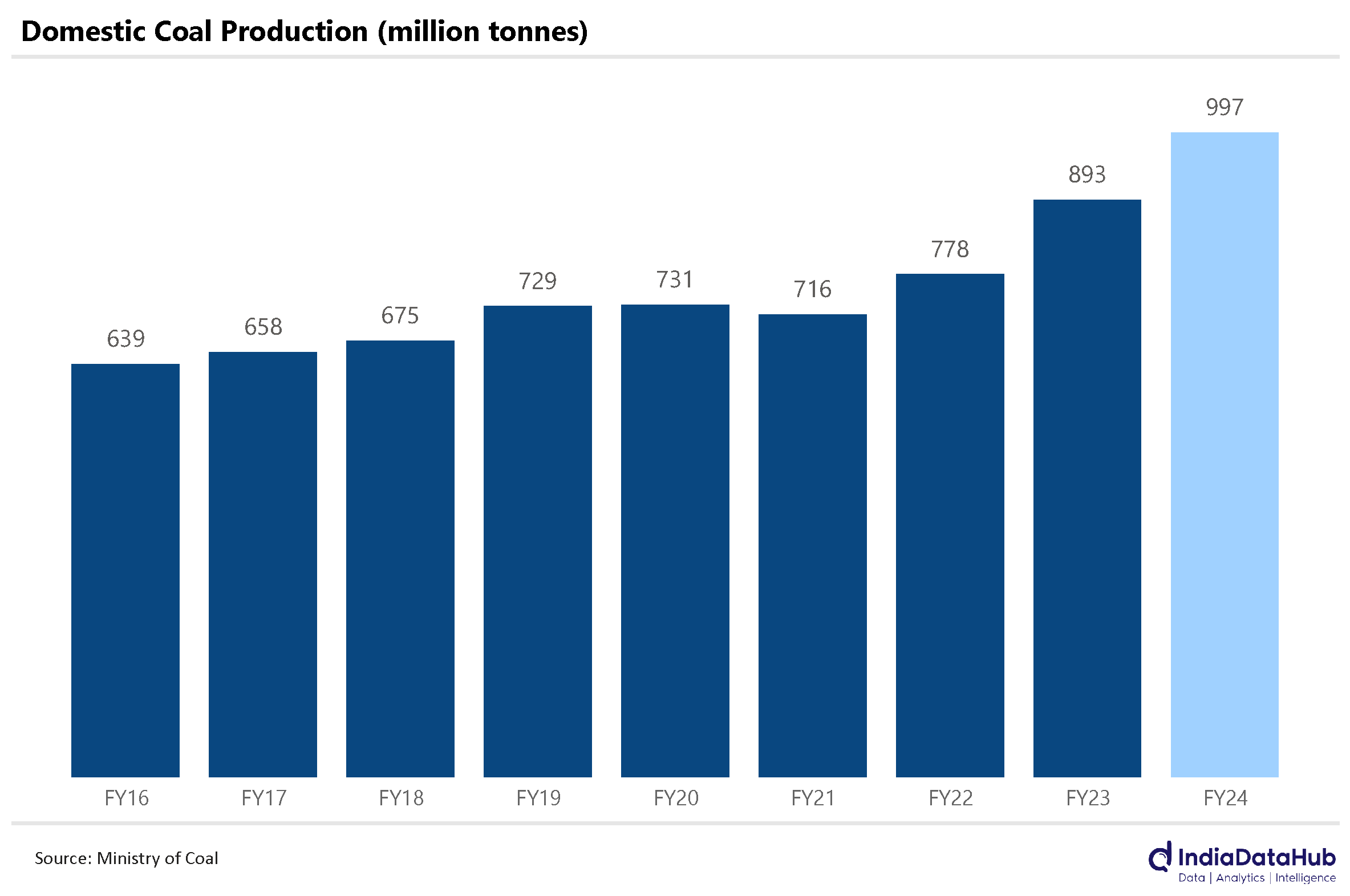

Strong growth in domestic coal production in last few years

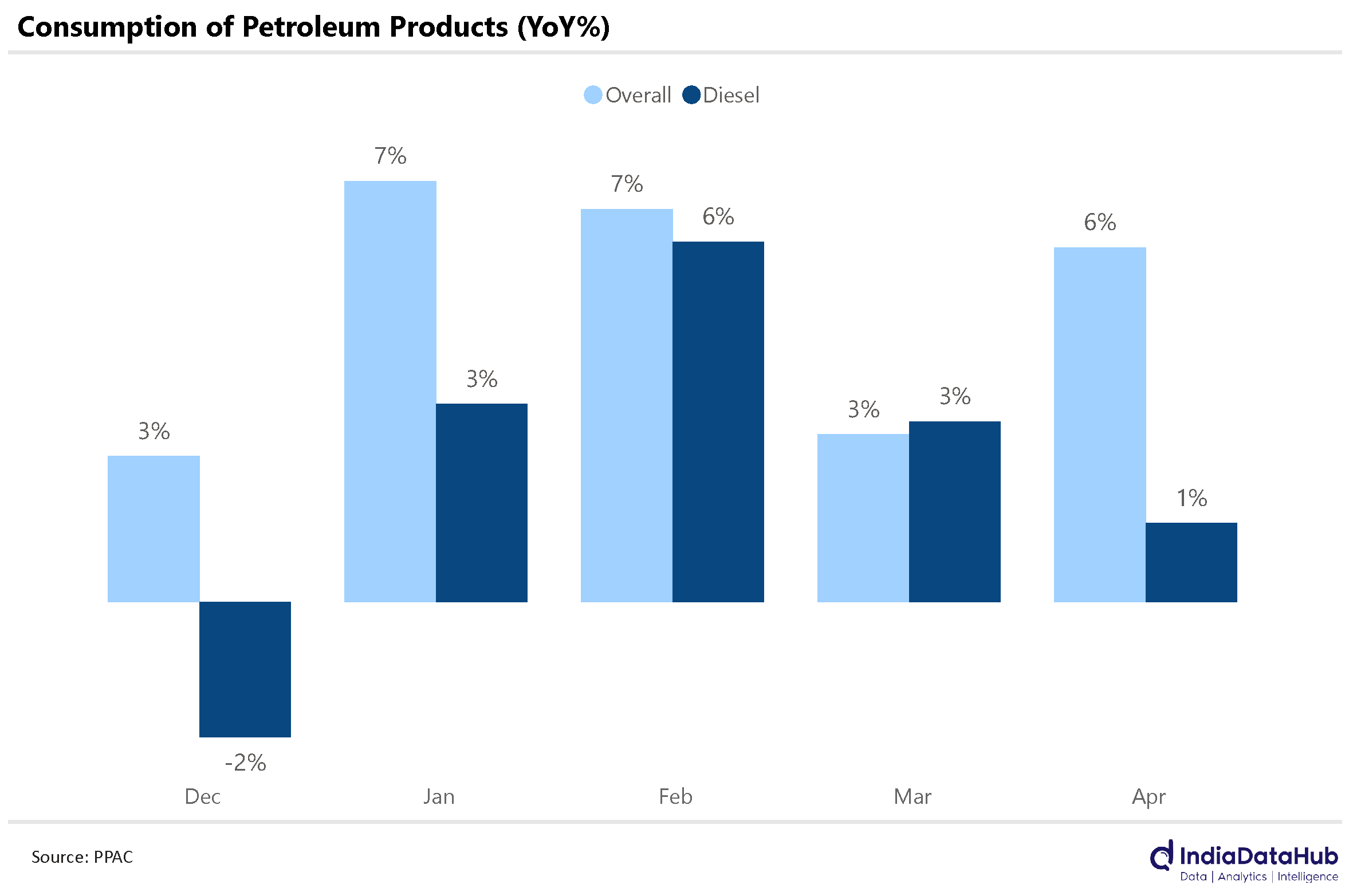

Weak diesel demand in April

Moderation in Railway freight and Port traffic in April

Continued strong growth in EWay bills

Continued decline in Naukri JobSpeak Index

More high-frequency data for April! First, power. The overall power generation in April grew 10% YoY, the highest since October last year. A few weeks back we had highlighted the decline in hydro generation and that has continued in April also. Hydropower generation declined 8% YoY in April this year. This is on top of a 24% decline in April last year. Hydro generation in April this year is the lowest since 2018! A flip side of this is that thermal generation (almost entirely Coal), has had to pick up this slack and in April thermal generation grew 11% YoY.

For a long time, thermal power plants in India were operating at subdued PLF (Plant Load Factor). And because thermal power plants operate with a fixed cost structure, some of the independent power plants (IPPs) were financially stressed. But power demand has been robust in the last 4 years and coupled with the decline in hydro generation in the last few quarters has meant that thermal PLFs are now above the long-term average. The trailing 12-month average thermal PLF is now the highest in over a decade. In the mid-2000s thermal capex took off in a major way when PLFs were in the early 70s, around 4-5ppt higher than where they are currently. Another year of strong power growth and thermal PLFs will reach there.

Concomitantly, the strong growth in thermal power generation is translating into strong domestic Coal production. Although the growth slowed down a bit last month. In April domestic coal production grew 7% YoY, the slowest since May last year. Overall domestic coal production grew almost 12% YoY in FY24 on top of an almost 15% growth in FY23 and a 9% growth in FY22. But for this, the higher demand for coal from thermal power plants would have had to be met through imports which would have pressured the external sector and the currency.

Petroleum product consumption saw a modest growth of 6% YoY in April. This is broadly the same growth as in the previous few months. So, there is no change in trend. The growth in April was driven by strong (double-digit) growth for Petrol, ATF, and Pet Coke. LPG also saw strong growth at 9% YoY. Diesel demand however saw only a modest 1% growth. Diesel consumption has remained subdued for the past few months growing in low single digits in the last two quarters.

And while the weak diesel consumption was partly explained by the strong growth in Railway freight (implying shift of freight to Railways from Roads) which had grown by 9% YoY during the March quarter, April saw a modest 1.6% YoY growth in Railway freight. Even the major ports saw a 4-month low growth of 1.3% YoY in the volume of Cargo handled in April.

On the flip side, however, EWay bills continue to see strong growth. In April, the number of EWay bills issued grew by 17% YoY, the 5th consecutive month of double-digit growth. Interestingly Interstate EWay bills have been consistently seeing stronger growth than Intrastate EWay bills. Interstate EWay bills would largely be for the movement of import/export goods as well as the movement of goods from factories to distributors. So, the broader freight data for April is a bit counterintuitive.

Lastly, the Naukri Job Speak Index, which tracks the number of job postings on Naukri.com declined in April this year compared to April last year. Worryingly, this is the 12th month of YoY decline in the last 13 months.

The Naukri Job Speak Index tracks white collar job postings which should be a leading indicator of the urban labour market. Till the December quarter at least the urban labour market picture, as per the quarterly PLFS, was still strong. The data for the March quarter will be released later this month so we will see if the PLFS is also picking up any stress in the urban employment scenario.

That’s it for this week. We lost Jim Simons yesterday. While the investment track record and philosophy of Charlie Munger and Warren Buffett is widely discussed and appreciated, Jim Simons has had an equally enviable record. But perhaps because his approach is far more esoteric, he remains an enigma (pun intended)! But at the end of the day, a long-term track record of alpha is all that matters. And on that metric, Jim Simons is right up there. So, RIP Jim. You were a torch bearer.