In this edition of This Week In Data, we discuss:

RBI keeps interest rates unchanged. As expected. But things are changing. As expected.

Households are getting anxious about the economy, both in rural and urban areas.

Corporate profits saw strong growth in 4Q, driven primarily by lower financial leverage

Corporate tax collections saw strong growth in April

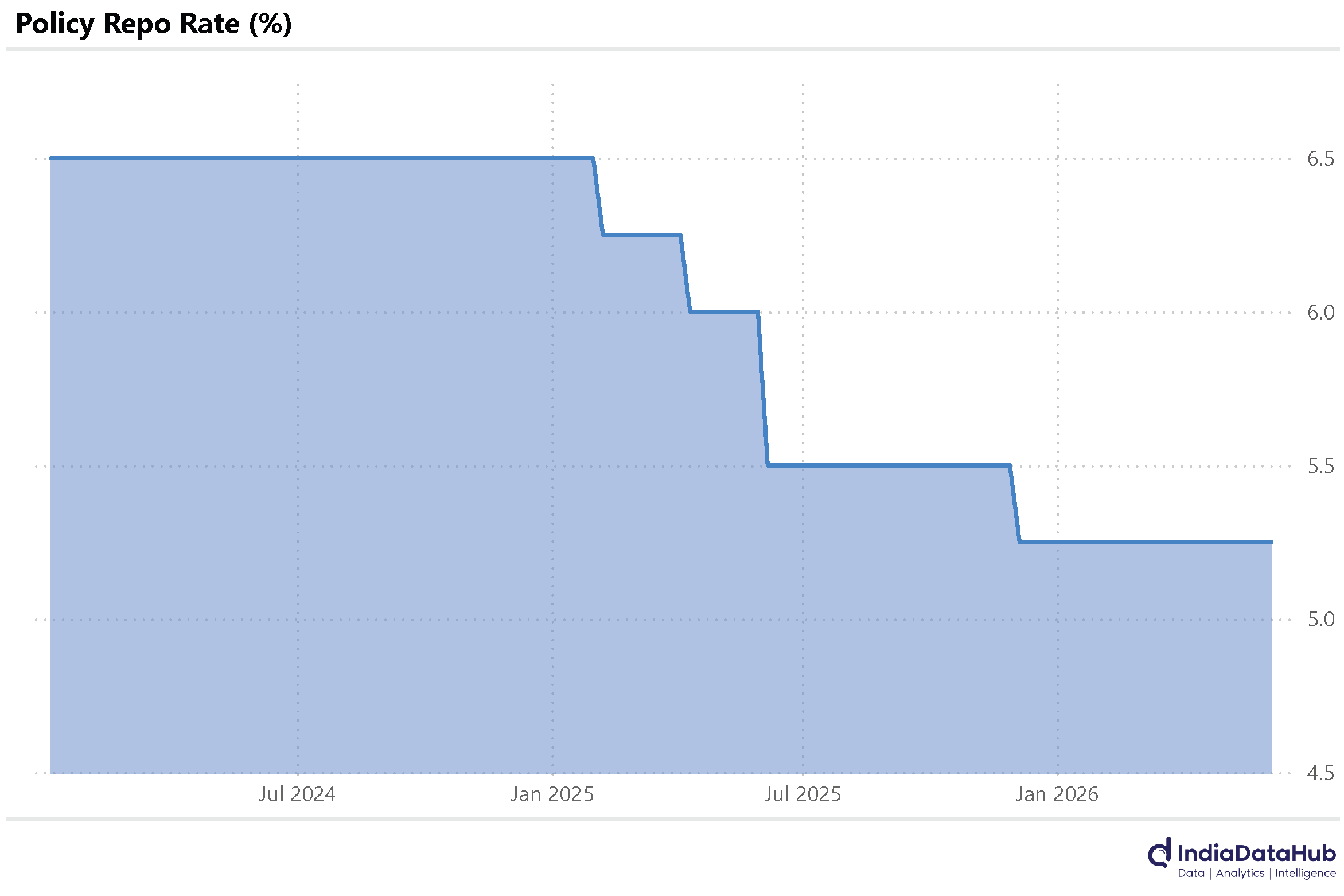

So, as expected, the RBI’s Monetary Policy Committee maintained the status quo on interest rates. The repo rate remains at 5.25%, a level it has remained since December last year. The stance of monetary policy also remains neutral, implying rates could go either way from here. And, both of these, were unanimous decisions. All as expected.

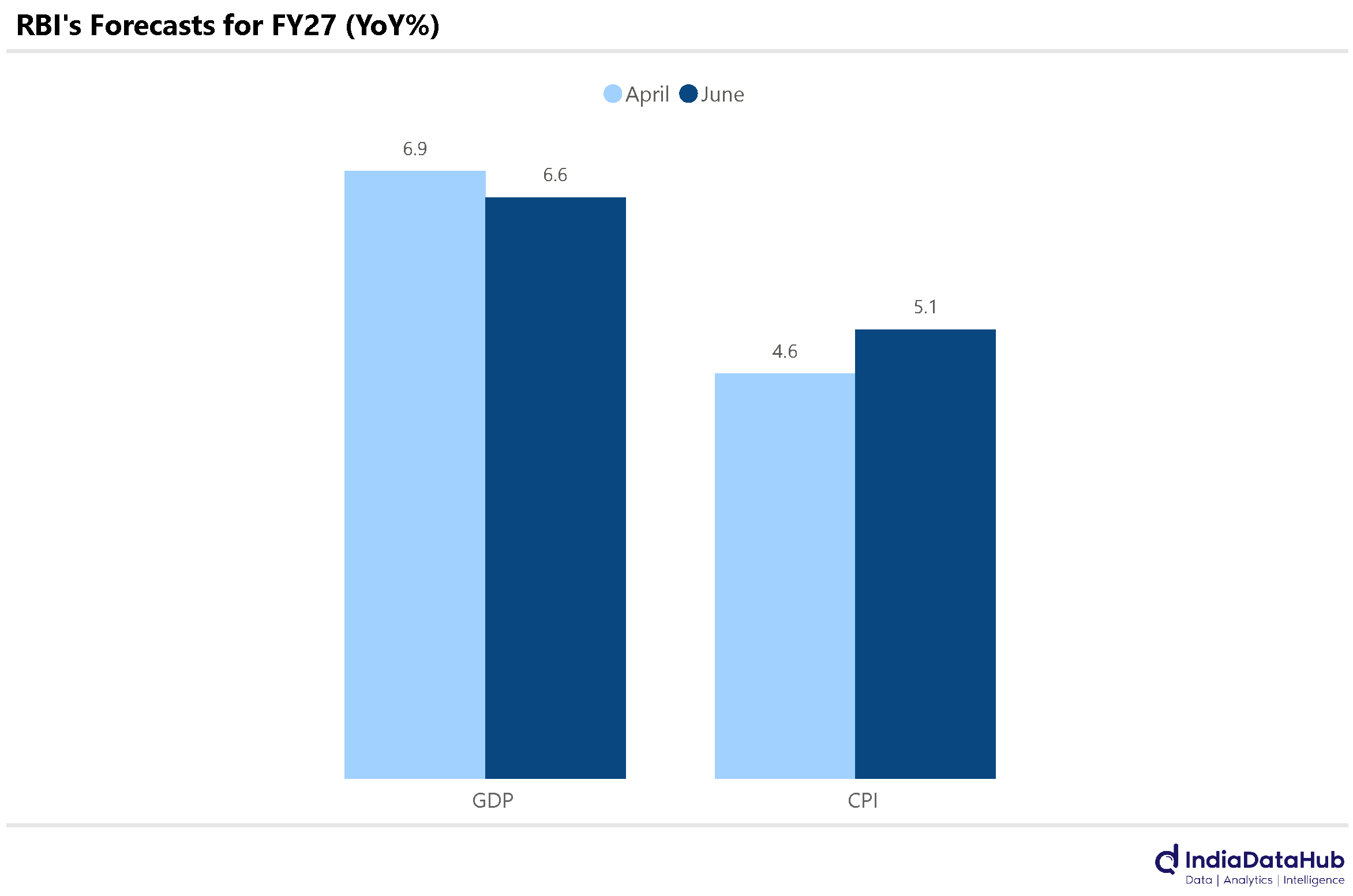

But as we have said before, under the hood, things are changing and changing in opposite directions, which creates conflicting challenges. And the RBI’s forecasts exemplify them. On one hand, the RBI has downgraded GDP growth estimate for this year – from 6.9% in April to 6.6% in June – and on the other hand, it has increased its inflation projection for this year – from 4.6% in April to 5.1% in June.

And there are two drivers for both of these changes. One, the higher commodity prices due to the conflict in the Middle East. And two, the expectation of below normal rainfall. The Middle East disruption has lasted longer than expected, when the conflict first erupted. It remains a binary event – an issue that can resolve tomorrow, but that tomorrow has, as yet, not come. And the monsoon, we shall know in the next couple of months if the forecast is likely to materialise.

One of the things the RBI does every two months is run a consumer confidence survey. And the latest results of the survey present a sobering picture. In urban areas (major cities), the perception of how robust the economic situation is, has fallen to almost a 3-year low. Their assessment of income has deteriorated sequentially, but is broadly same as it was last year. For example, the percentage of households that report that their income has increased or decreased has remained the same as last year.

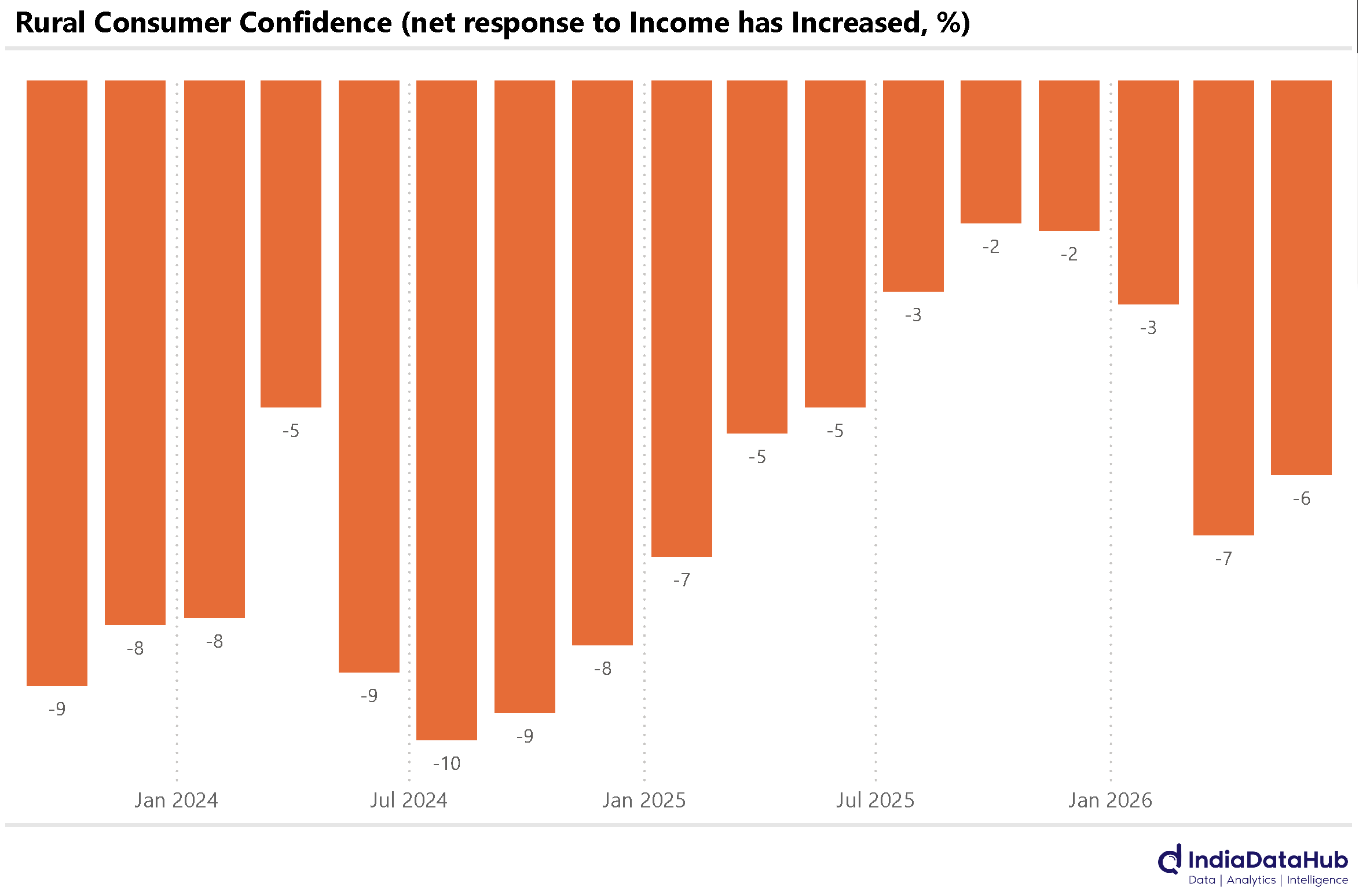

And on the rural side, a similar picture is seen. Perception about economic situation has fallen sharply, while assessment of income has similarly worsened sequentially, it is not at alarming levels. The risk, though, is that if their anxiety about the economy builds, then even if it does not immediately impact incomes, it might impact consumption, and that will cascade through to incomes and employment.

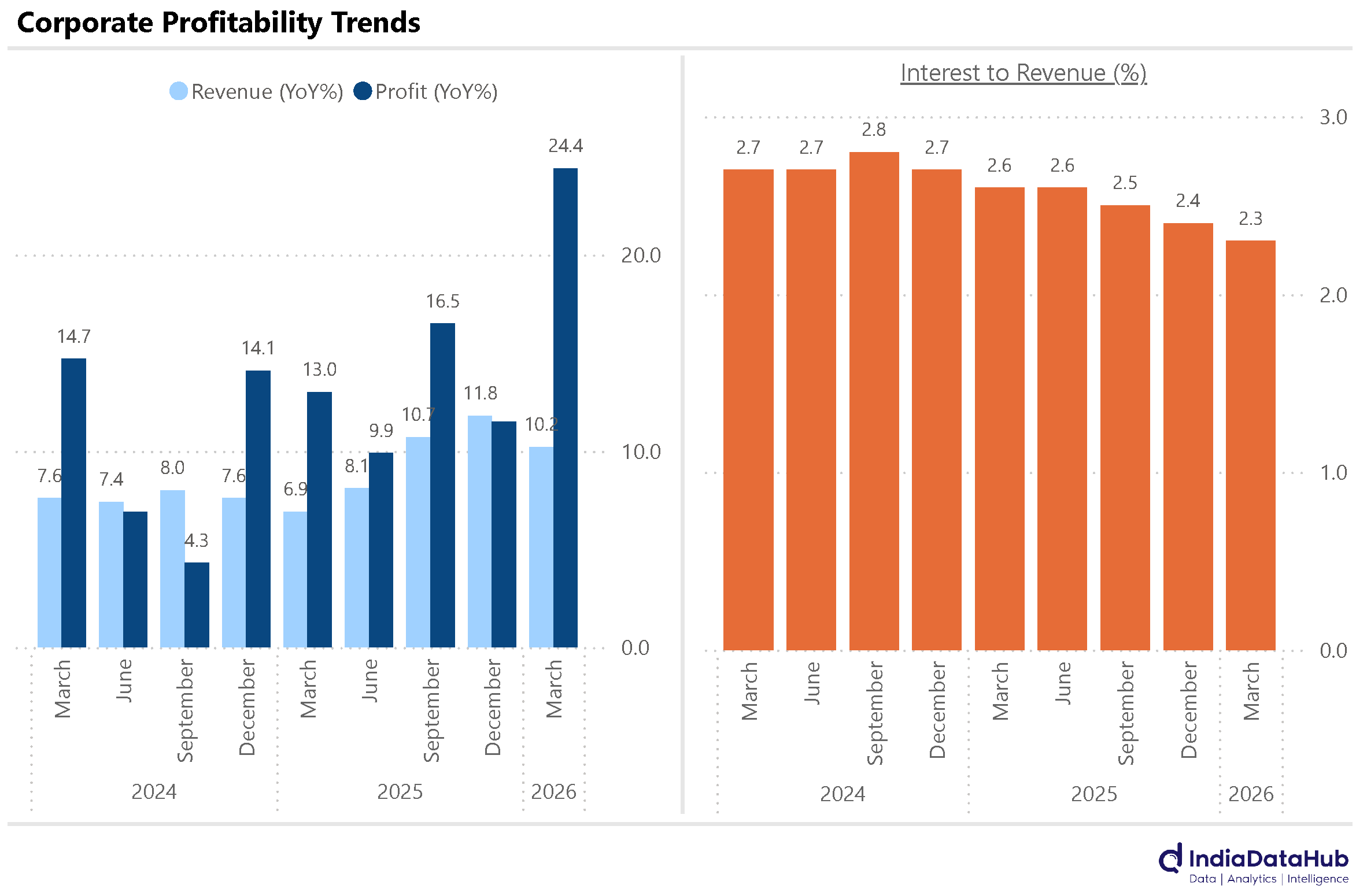

Lastly, the 4Q reporting season just ended. And on an aggregate basis, it was a fairly strong quarter. While revenue growth was modest at 10%, slower than the 11-12% growth in the preceding 2 quarters, profit growth was very strong. Reported profits grew over 20% YoY, the strongest growth in over 2 years.

This was largely driven by lower interest costs. Debt equity ratio continues to trend down, and with interest rates having fallen through FY26, it is now flowing through to P&L through lower interest expense. Interest cost declined from 2.6% of revenue to 2.3% of revenue, driving the PAT growth. Operating margins (EBITDA margin) remained almost stable on a YoY basis.

And the current quarter might also turn out to be strong for corporate profitability – corporate tax collections grew 17% YoY in April, the strongest growth in recent months. But this is just one month, so we shall see…

That’s it for this week. See you next week…