RBI policy, UPI Duopoly, Mixed Sept data and more...

This Week In Data #96

In this edition of This Week In Data, we discuss:

RBI maintains status quo on rates but changes its stance

A more hawkish (or less dovish) MPC?

RBI remains optimistic on growth, even marginally revises up its growth forecast

September was another weak month for Petroleum consumption

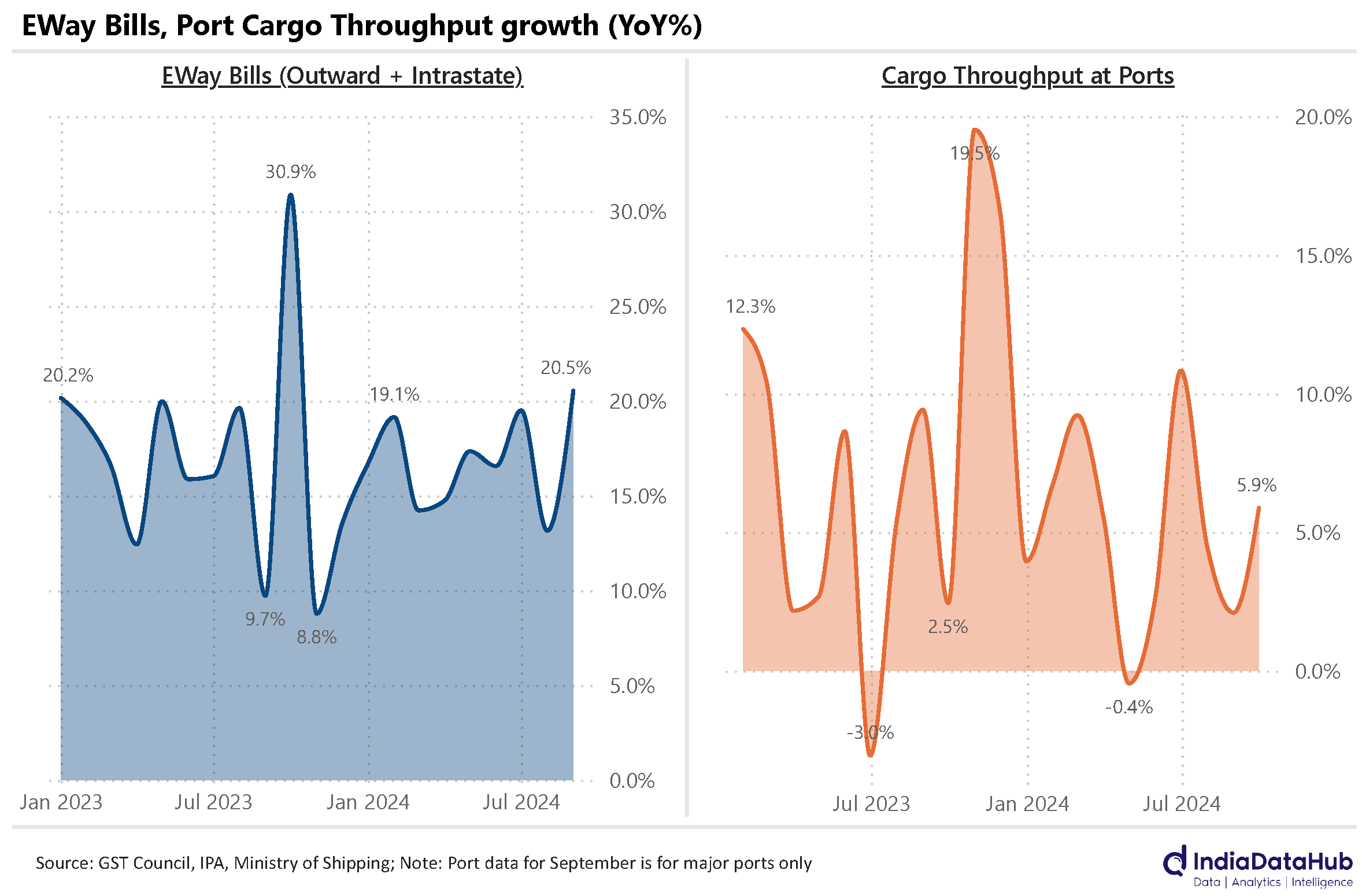

EWay bills and Port traffic however remain resilient

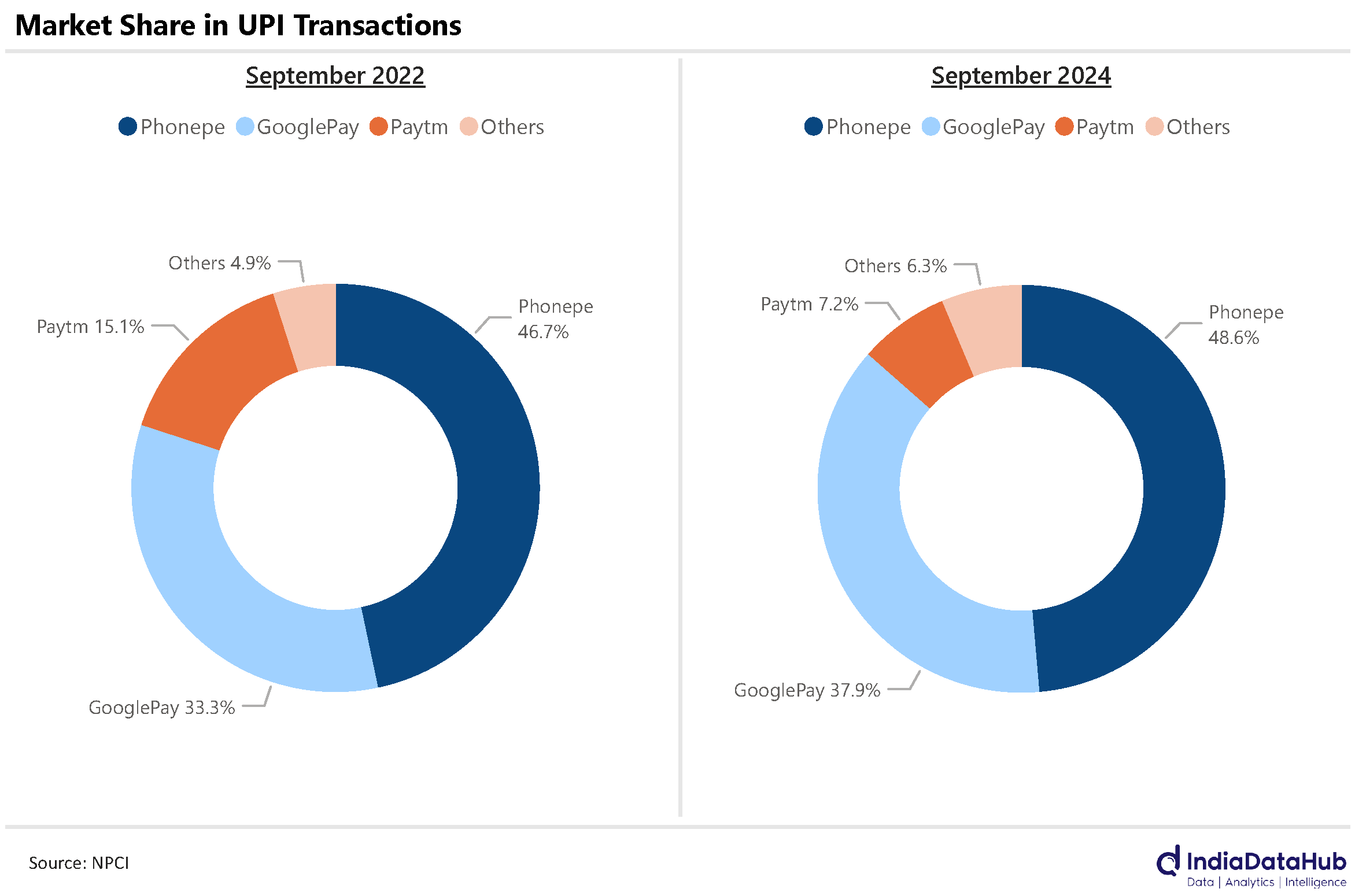

Paytm’s loss in UPI payments is Phonepe and GooglePay’s gain

So the RBI or the MPC did what was generally expected. It kept rates unchanged. So the Repo rate remains at 6.5%, the MSF rate remains at 6.75% and the SDF rate remains at 6.25%. The repo rate has remained at this level now since February last year. But some things did change. For one, we had 3 new members on the MPC as the term of the external members of the MPC had ended and the Government has nominated new members. Recall that 2 of the 3 external members had been dissenting arguing for a rate cut AND a shift in the stance of monetary policy to neutral. In last week's policy, there was only 1 dissention. So effectively, one can argue that the MPC’s composition is now a bit hawkish than before.

The MPC also unanimously changed its stance to neutral which is sort of a preparation for a rate cut. Going from its earlier stance which was for withdrawal of accommodation to a rate cut in one go would have been odd. So, this sort of prepares the ground for a rate cut. But this does not, ipso facto, mean a rate cut is likely in December. For one, the RBI has marginally become more confident in the growth outlook. Accordingly, it has increased the GDP growth estimate for the March 2025 quarter by 20bps to 7.4% from 7.2% in the August policy. For the June quarter next year, it has increased its growth projection by 10bps to 7.3%. So, the RBI doesn’t think the growth outlook has worsened.

So, whether a rate cut will happen in December or not, largely depends on the data flow between now and the next MPC meeting in early December. Over to data then!

And while we are discussing growth data, some additional data for September that we received was also weak. September was the second consecutive month that consumption of petroleum products declined. Petrol consumption moderated sharply to 3% YoY from high single-digit growth in August. While diesel consumption declined for the second consecutive month. LPG consumption also moderated sharply to 1.6% YoY in September.

However, Cargo throughput at the major ports remains resilient. Total cargo throughput grew 6% YoY in September, only modestly slower than the growth in the preceding 3 months. Similarly, eWay bills grew 20% YoY in September. This is the highest growth in eWay bills since October last year.

As we discussed last week, end consumption was impacted in September due to seasonality but if underlying demand is still strong consumption should rebound in October. The eWay bills data and the port throughput data are in sync with this.

Lastly, the duopoly in UPI payments between PhonePe and Google Pay has only gotten stronger over the past couple of years. Paytm which is the third largest UPI app is facing difficulties due to regulatory issues. Over the past two years, its market share in the number of UPI transactions has fallen by more than 50% – from just over 15% in September 2022 to just over 7% in September this year. Almost this entire decline has been picked up by Phonepe and Google Pay. Their combined market share has increased from 80% in September 2022 to 86% in September this year.

Back in 2022, the fourth largest UPI app was that of Yes Bank. Its share in September 2022 was 0.9%. Its share last month was less than 0.5%. The 4th largest UPI app currently is Cred which processes less than 1% of UPI transactions. Recall that NPCI was considering capping the market share of any UPI app at 30% with December this year being the deadline. This certainly looks unlikely to be implemented at the current juncture.

That’s it for now. See you next week…