Rupee depreciation, CPI, Weak Exports China slowdown and more...

This Week In Data #97

In case you missed it, we released climate data on IndiaDataHub this week. We start with rainfall and temperature data with history going back to several decades. We publish this data at a weekly and monthly frequency, both in absolute terms as well as deviations from long-term average (defined as trailing 30 years). While the utility of rainfall is easily appreciated, we show that temperature is also an important cyclical variable in many sectors such as Agriculture, Power and Consumption. Read more from here. We are also collaborating with Great Lakes Gurgaon in creating a SCORE Index that tries to quantify the relative importance to sustainability and related topics in popular discourse. Read more from here.In this edition of This Week In Data we discuss:

The rupee has remarkably stable against the USD in recent months

However, the rupee has depreciated sharply against other major currencies, notably CNY

CPI inflation rose in September primarily due to higher food inflation

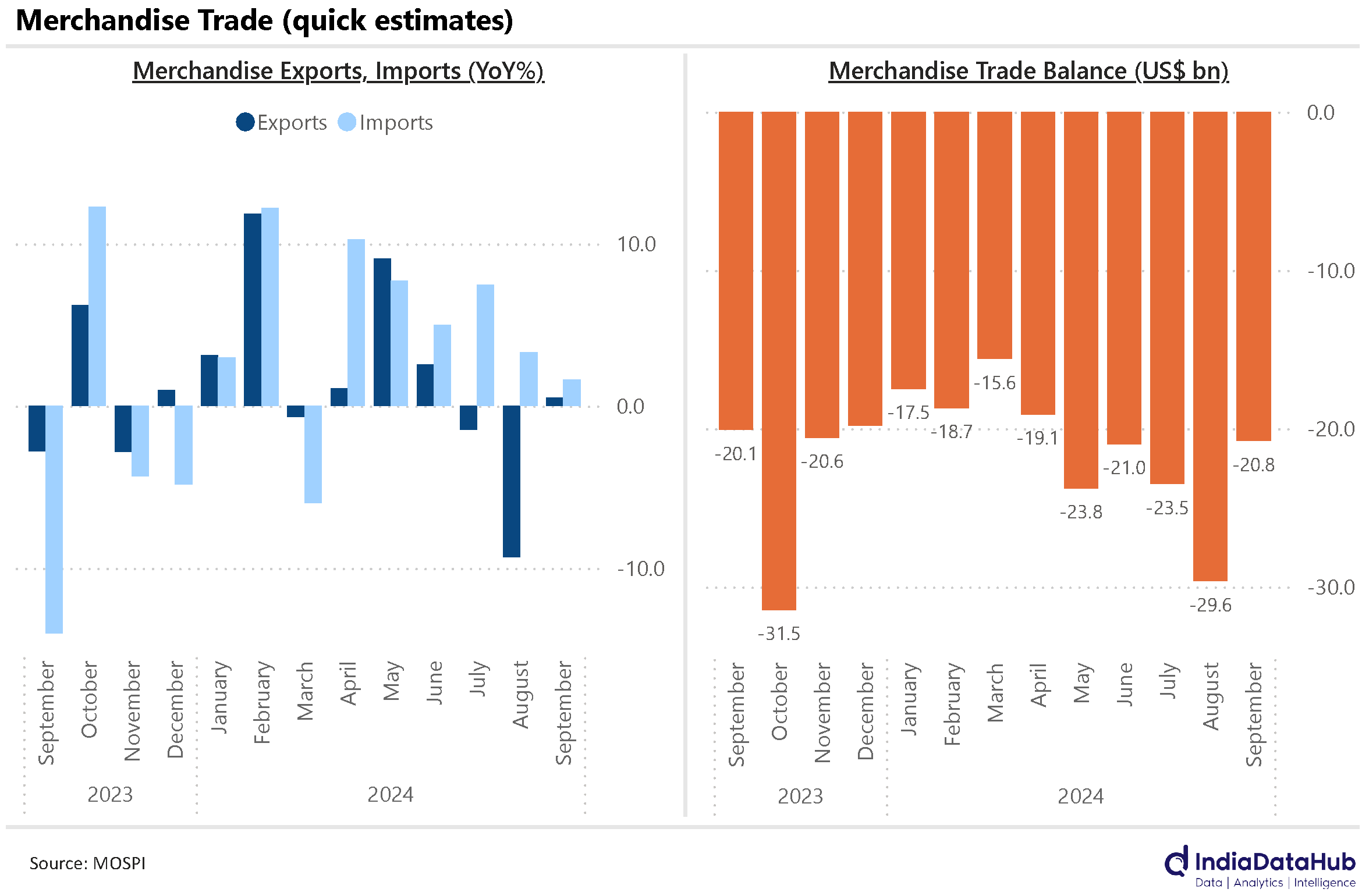

September was the third consecutive month of weak exports

Electronic exports are no longer the fastest growing category of exports

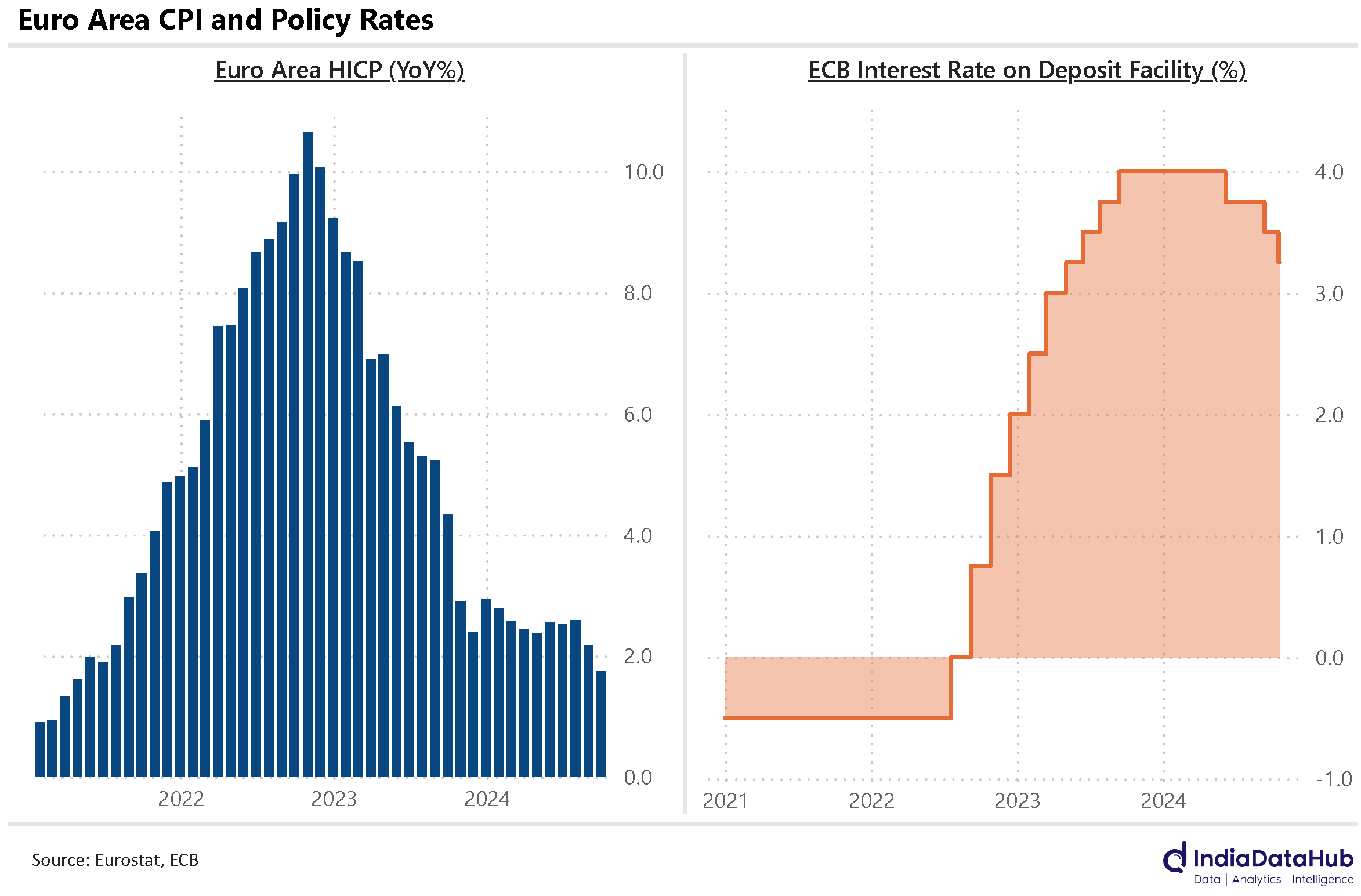

Inflation continues to moderate in Euro area and the ECB if following through with rate cuts

GDP growth continues to moderate in China with real estate being the biggest drag

The rupee hasn’t been depreciating sharply in recent weeks as is made out to be. In absolute terms, the rupee has crossed 84 to the dollar this month reaching an ‘all-time low’. This is of course factually true. But the bigger story is how remarkably stable the rupee has been in recent months, including so far in October. Despite crossing 84 this month, the rupee is down less than 1% against the US Dollar over the past year. Indeed, even on a 2-year basis, the rupee has depreciated less than 2% against the US Dollar. Over the past 2 decades, the median depreciation in the rupee against the US Dollar over 2 years was 7%.

However, what has gone unnoticed is that while the Rupee has remained fairly stable against the US Dollar, it has depreciated against other large currencies. Over the past year for instance, the IDH INR Index (a weighted average of INR’s performance against 5 currencies – USD, EUR, GBP, JPY, CNY) has fallen by almost 3%. Especially worth noting is the almost 5% depreciation against the CNY over the past year as this links back to core inflation given the high reliance on Chinese imports.

Speaking of inflation, CPI Inflation ticked up sharply in September – from 3.65% in August to 5.5% in September. This was of course expected and is largely due to the spike in food inflation due to the base effect. Food inflation rose from 5.3% in August to 8.4% in September. Core CPI was thus largely unchanged, but it did tick up 10bps to 3.5% and has now risen by 40bps in the last 3 months – it was 3.1% in June. At 3.5% core inflation remains low so we are splitting hairs over the 40bps increase. But given the fall in the rupee, especially against the CNY, it seems as if the core inflation trajectory is likely to continue to gradually trend upward in the next few months.

India’s merchandise exports saw sluggish growth for the third consecutive month in September. Exports grew, but by a modest 0.5% YoY as per the quick estimates. Exports had declined 9% in August and 1.5% in July. Growth in imports moderated for the second consecutive month in September. Imports grew 1.6% in September, down from 3.3% in August and 7.4% in July. With growth rates in imports and exports broadly converging, the trade deficit narrowed sharply on a sequential basis to US$21bn in September, down from almost US$30bn in August.

A large part of the moderation in exports in recent months is due to lower petroleum exports. Petroleum exports declined 25% YoY in September excluding which total exports grew 7%. Even YTD petroleum exports have declined in double-digit terms and excluding them exports have grown just over 4% YoY. For the last few years now, electronic goods have been the fastest growing category in exports. However electronic exports have seen a slowdown. They grew 8% YoY in September after growing 7% in August. Exports of Engineering goods, Textiles, Plastic products as well as Chemicals grew faster than that of electronic goods in September.

Globally, inflation has been trending down in most countries in recent months. Euro Area's HICP declined to a 41-month low of 1.7% in September and it is now lower than the 2% medium-term target for the European Central Bank. In sync with falling inflation, the ECB reduced its policy rate by 25bps. The UK also saw inflation moderate sharply to 1.7% YoY in September from 2.2% in August. UK’s inflation is now the lowest since April 2021. Japan and China also saw inflation moderate in September.

Lastly, China’s GDP growth moderated to a 5-quarter low of 4.6% YoY during the September quarter. Real estate continues to be the biggest drag on growth. The sector saw a decline during the September quarter which was the third consecutive quarter of negative growth in the sector.

That’s it for this week. See you next week…