Rupee's fall, falling reserves, Strong equity flows and more...

This Week In Data #107

In this edition of This Week In Data, we discuss:

INR’s continued depreciation

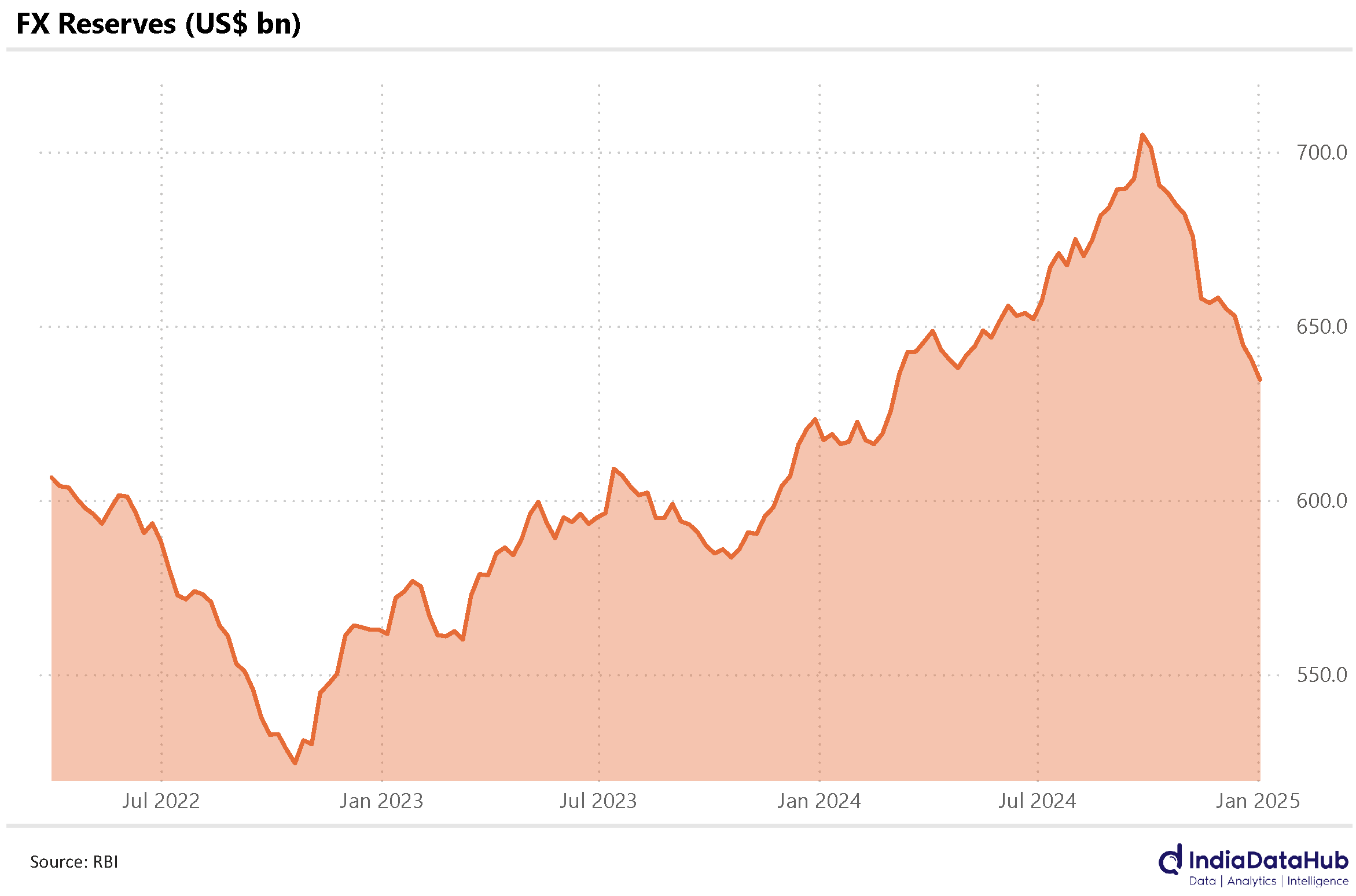

Decline in FX reserves and reserve adequacy

MFs continue to see strong equity inflows

Robust growth in equity folios

Strong labor data in the US

Higher CPI in Eurozone

The rupee continues to slip against the US Dollar making a new ‘all-time low’ almost every day. But this is more a case of the USD strengthening rather than the INR weakening. The USD is gaining against most other currencies. And in large part due to the RBI’s intervention, the INR continues to outperform most global currencies.

Over the past three months, the INR has lost 2.4% against the USD. However, most other currencies have lost a lot more against the USD during this time. The IDH US Dollar Index has risen by almost 6% over the past 3 months. The Euro, the GBP and JPY have lost ~6% against the USD. And the high beta EM currencies like BRL and ZAR have fallen 8% against the USD. The Asian currencies, except for KRW, have outperformed the other currencies against the USD. The PHP for instance has fallen just under 2% over the past 3 months and the THB and the IDR have fallen just ~3%. So relative to Asian currencies, the INR has performed broadly in line.

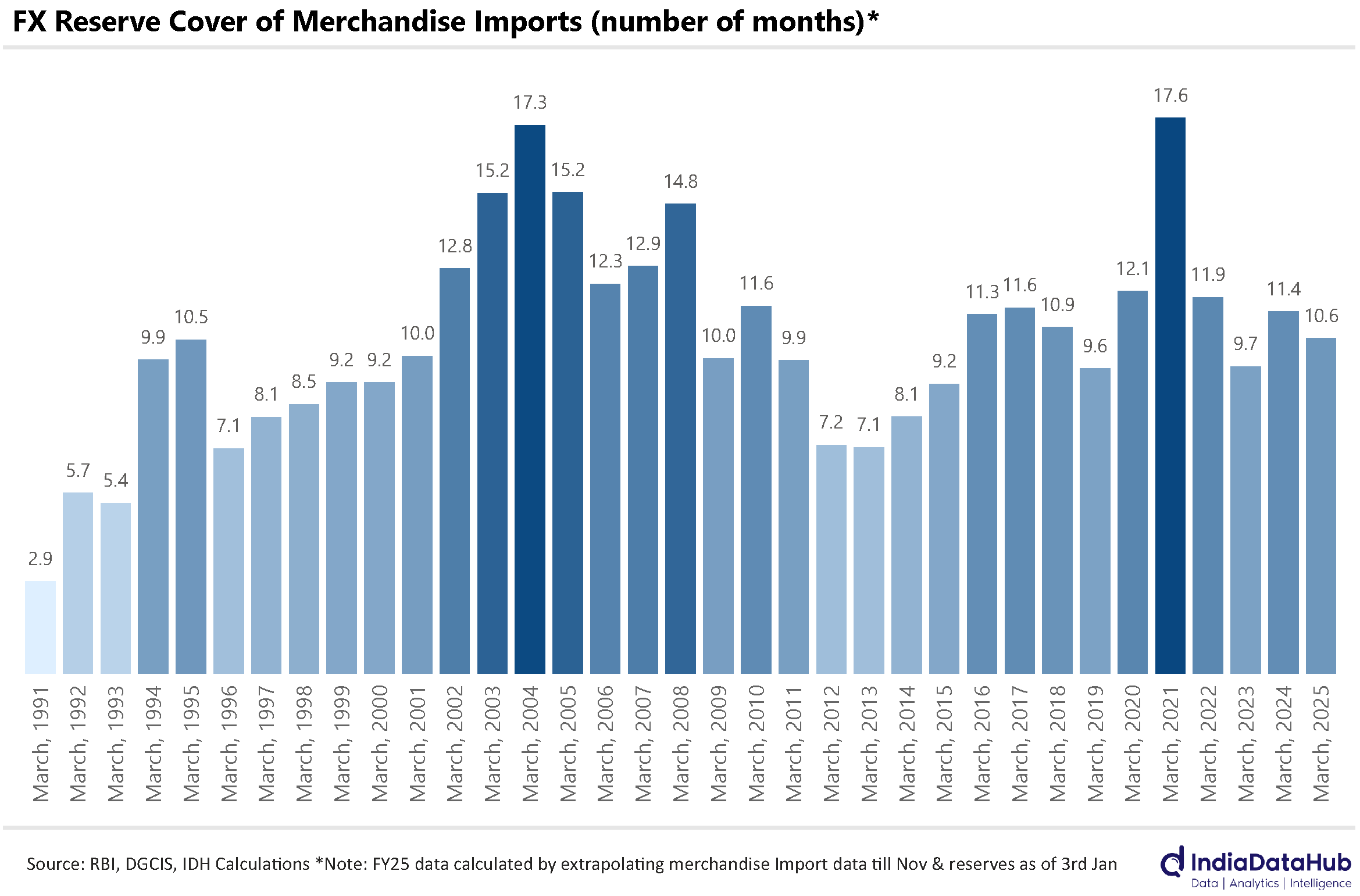

The RBI’s defence of the rupee has meant that India’s FX reserves continue to fall. FX reserves have declined 13 of the last 14 weeks with a cumulative decline of US$70bn(!) since September 2024. There has been some discussion about what the adequate level of reserves is. In that context, it is worth noting that at US$635bn as of 3rd January 2025, reserves have fallen below 11 months of merchandise imports. And FX reserves now cover ~85% of the external debt.

By the traditional metrics of adequacy, the current level of reserves is still adequate but not at a level that can be characterized as ‘excess’. Of course, one can argue that it is extremely unlikely that India will see outsized capital flows running into a few 100 billion dollars such that the adequacy of reserves will be tested. But then again, the whole point of maintaining reserves is to serve as insurance against potentially unforeseen external sector developments.

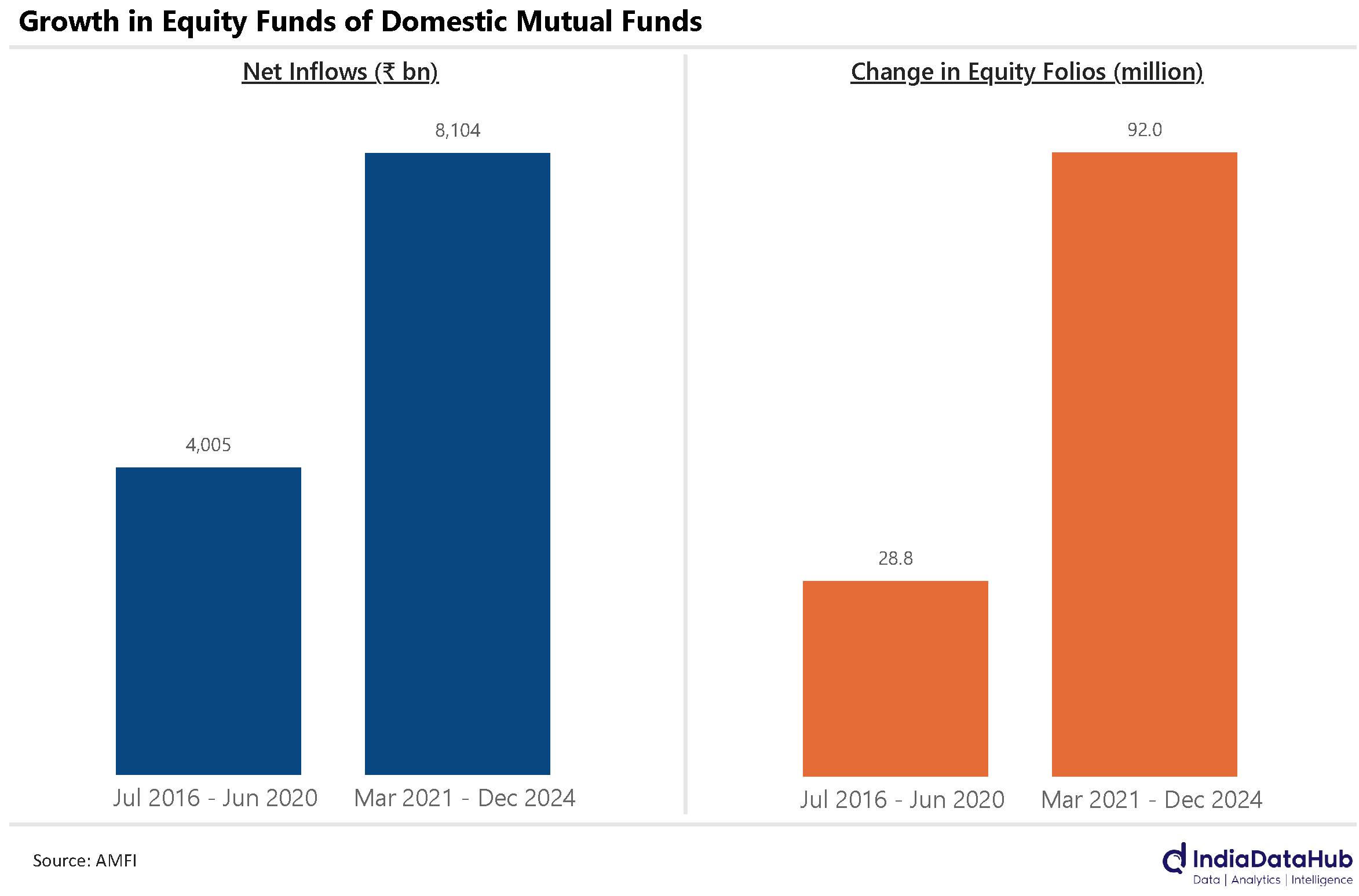

Equity funds saw another strong month of net inflows. December saw a net inflow total of ₹411bn, the second-highest net monthly inflow ever. We have now seen 46 consecutive months of net inflows into the domestic equity schemes. In another couple of months, the current streak of uninterrupted net inflows will be the longest ever – the previous longest streak of net inflows was 48 months starting in July 2016 and ending in June 2020. For reference, the current streak started in March 2021.

And while the current streak is 2 months shorter, it has already seen significantly bigger inflows. In the last 46 months (March 2021 to December 2024) net inflows into equity funds have totaled ₹8100bn whereas the previous 48-month cycle of uninterrupted inflows had seen net inflows of just over ₹4000bn or half as much as the current cycle.

And not only have inflows been much stronger, but the investor base has also widened much more in the last few years. For example, between June 2016 and July 2020, the number of folios in equity schemes increased by just under 30 million. In the last few years however (March 2021 till December 2024), the number of folios in equity schemes has increased by over 90 million or more than 3x as much. As of December 2024, there were a total of 158 million folios in the equity schemes, an increase of more than 5x in the last 10 years!

And on this positive note, let us turn towards what’s been happening in the rest of the world. Starting with the US where we got the December non-farm payroll data. And we had another month of strong job growth. As per the provisional estimate, the US economy added 256k jobs in December, the highest growth in nine months. And the second consecutive month of over 200k job growth. Average hourly earnings also grew by a strong 3.9% YoY in December and the unemployment rate held steady at 4.1%.

And in the Euro area, the flash HICP for December suggests that inflation picked up from 2.2% in November to 2.4% in December with the services sector being the key driver of inflation at almost 4% YoY. So, we start the year with a not-so-benign data from a rates perspective. Not surprisingly then, the markets are now expecting no rate cut from the Fed in the two meetings in this quarter (Jan and Mar) and only a 25bps rate cut in the second quarter of this year.

That’s it for this week. See you next week…