Slowing migration, Strong services exports, Credit growth and more...

This Week In Data #164

In this edition of This Week In Data, we discuss:

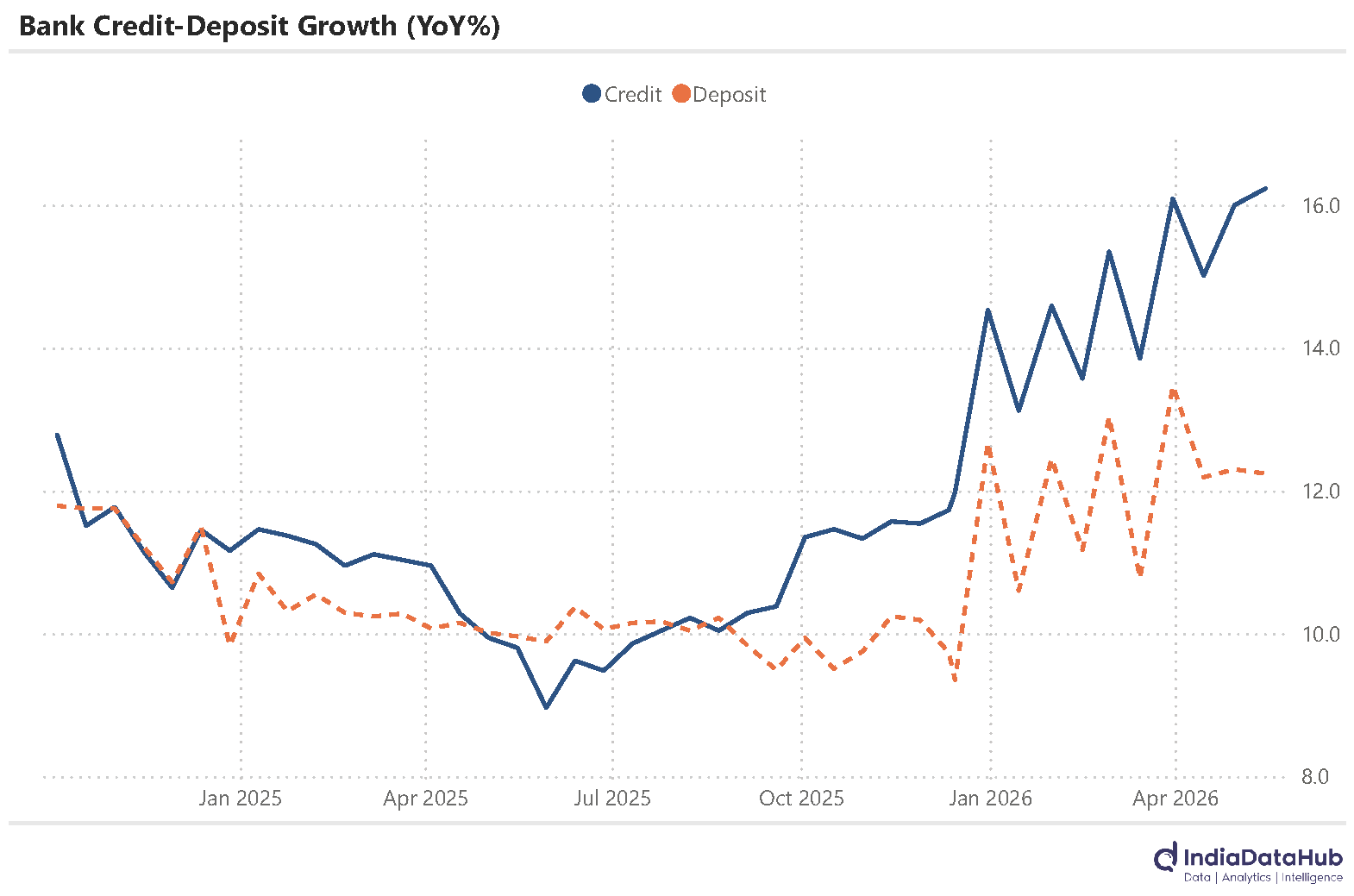

Bank credit growth has continued to accelerate even as deposit remains stable

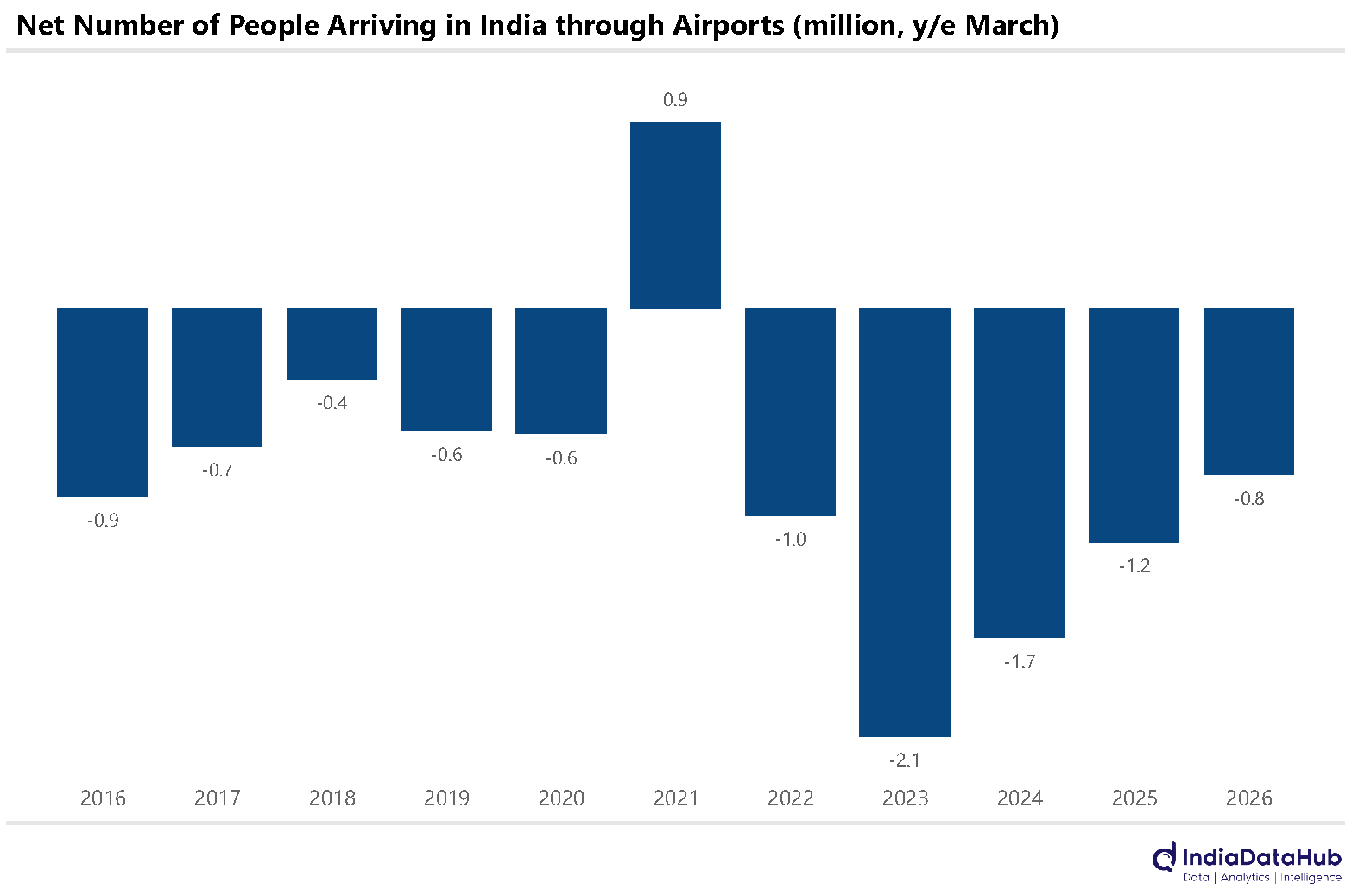

Migration from India has been slowing

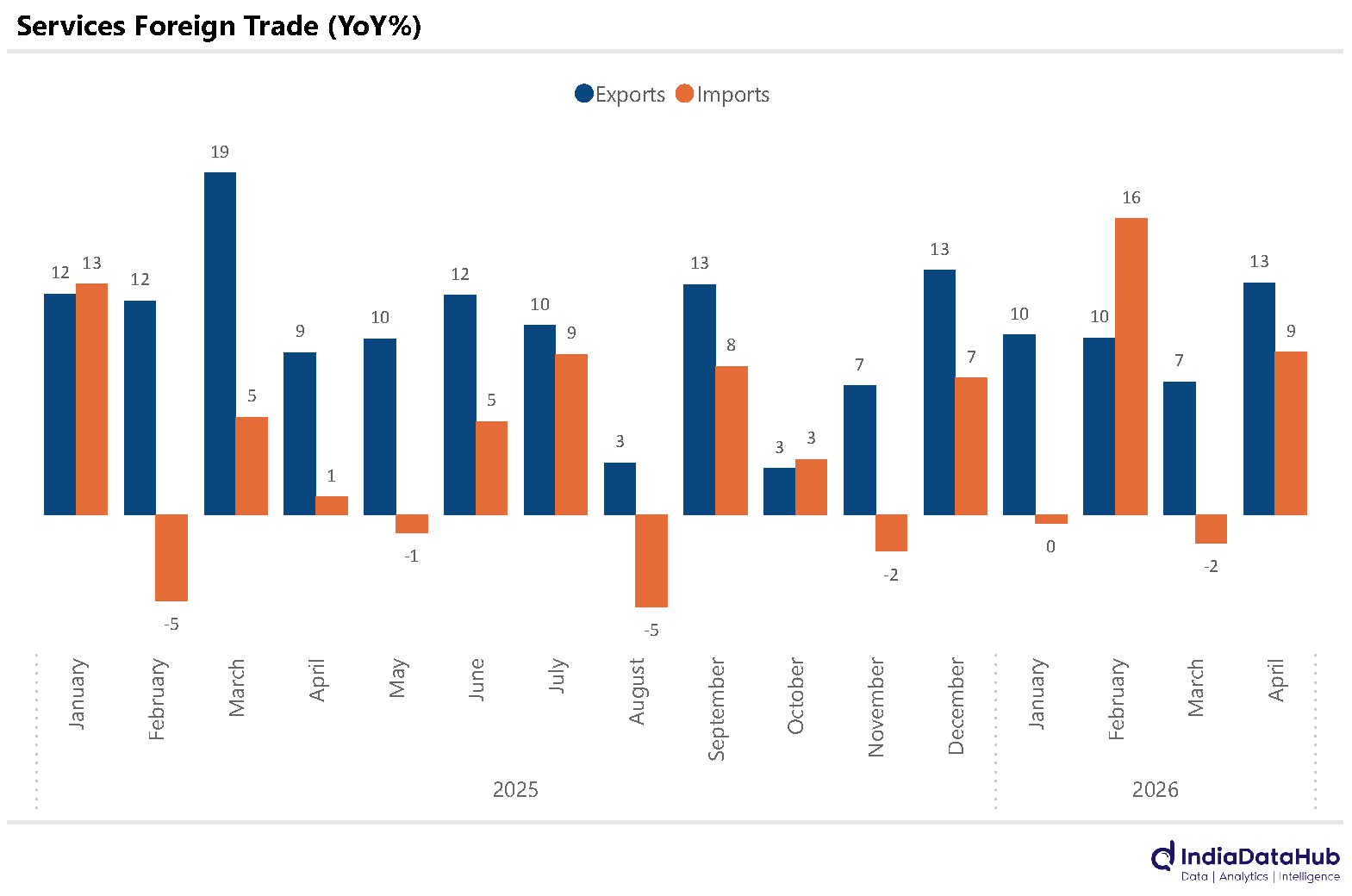

Services export growth remains resilient

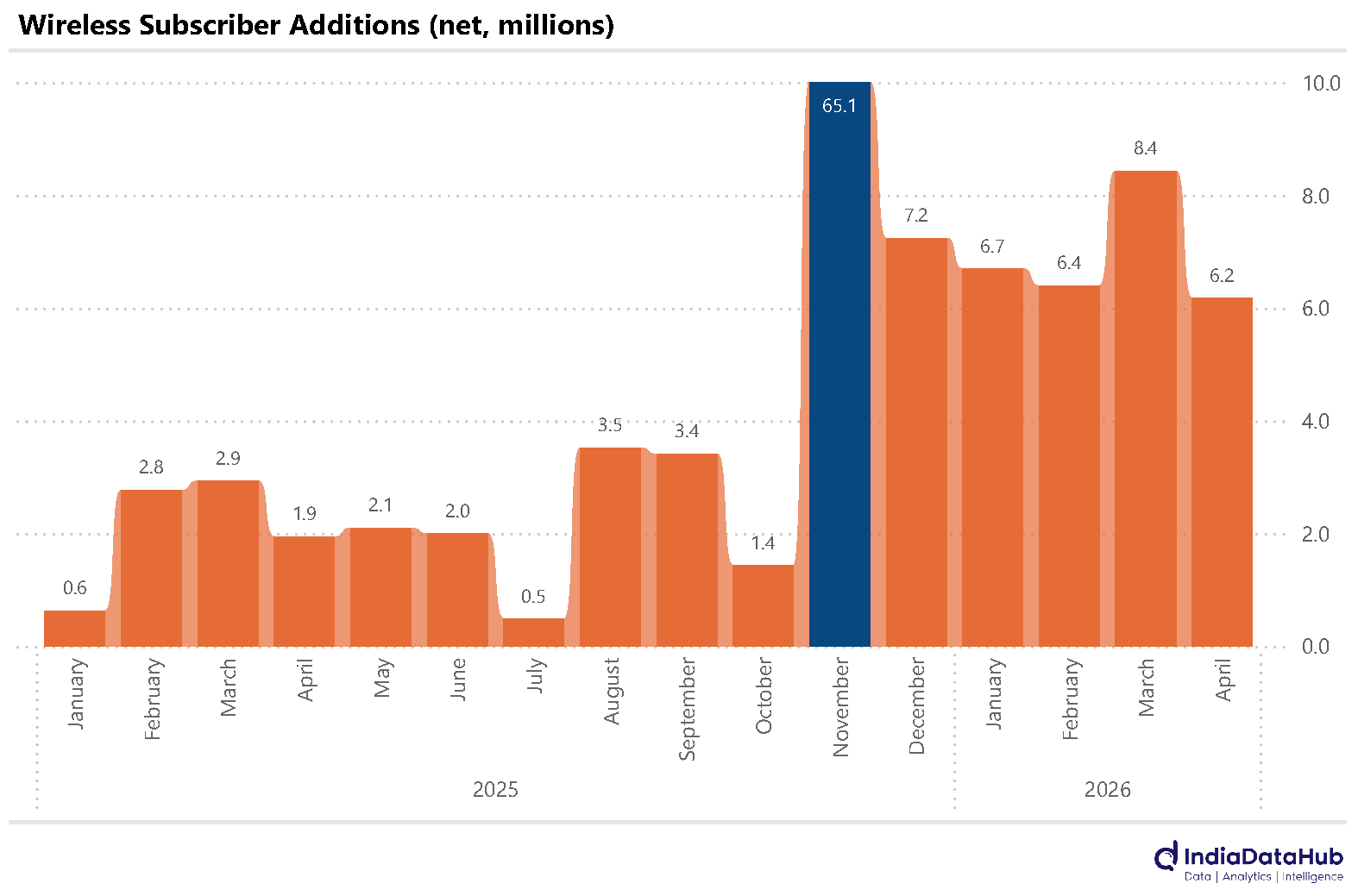

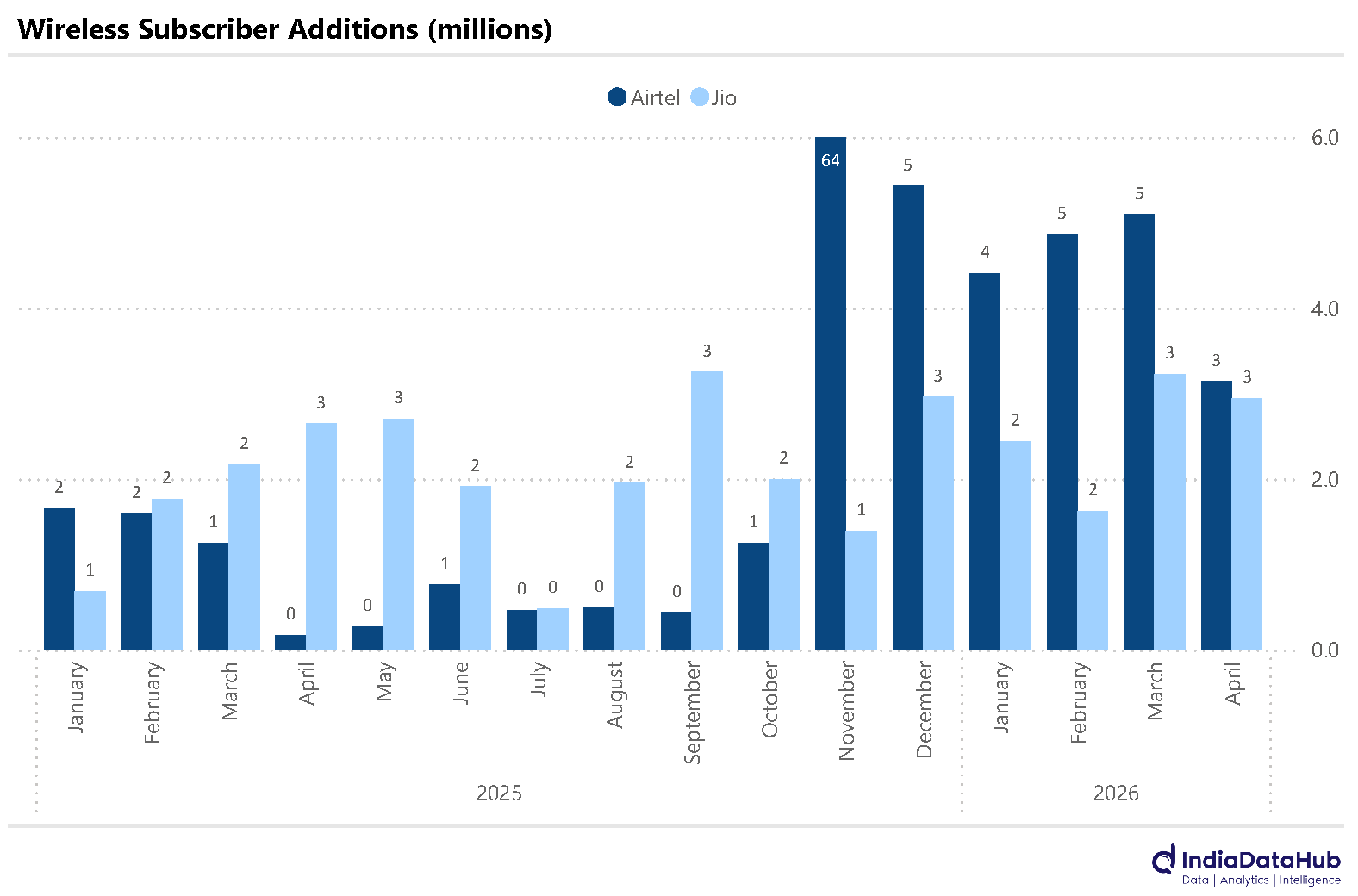

Wireless subscriber growth remains strong; Airtel seeing stronger growth than Jio

Credit growth continues to see an uptick. As of mid-May, overall bank credit growth had ticked up to 16.2% YoY, the highest in the last few years and up from ~14% at the start of the year. Deposit growth has, however, not seen any commensurate uptick, and thus the gap between credit and deposit growth has widened to almost 4ppt. The credit-deposit ratio is now in the 80s, and this is when we are in the lean period for credit growth – credit growth generally tends to be stronger in the second half of the year.

This, coupled with an uptick in inflation and possibly higher fiscal deficit (hint – higher government borrowings) due to lower petroleum tax collections, will make liquidity management challenging for the RBI in the next few months. So monetary policy will not just be about interest rates in the next few months.

There is often talk of migration out of India. There is no official data on the scale of migration of people. But a useful proxy is the net number of people arriving in India at airports (basically arrivals minus departures). Land or sea-based inter-country movement of people is limited, so most of the inter-country movement of people is through airports. So, this is a good proxy if not a precise number.

And by this metric, FY26 saw the lowest migration in recent years. Just over 800 thousand people left India during the year, down from 1.2 million in FY25 and a peak of 2.1 million in FY23. This lower migration possibly reflects a combination of factors – lower onshore movement in IT due to the H1B Visa and other issues, possibly also a lower number of children migrating for education.

Linked to this is the topic of services exports, most of which are IT exports. And last week we got the provisional data for April. And exports don’t seem to be seeing any slowdown. Services exports grew 13% YoY in April, the fastest growth since December last year and above the average monthly growth of 10-11% seen in the last 2-3 years. So far, the data is not showing any adverse impact of AI on India’s IT exports.

And services imports grew 9% YoY, resulting in continued mid-teens growth in services surplus. The first 4 months of the year have seen services trade surplus average just under US$20bn a month, up 14% or ~US$10bn on a YoY basis.

Lastly telecom. And the momentum in wireless subscriber additions continues. April saw over 6 million new subscribers being added by the wireless operators. Even after Airtel’s restatement of subscribers in November (which resulted in a big increase in its subscriber base by over 60 million), the last few months have seen ~7 million net wireless subscribers being added every month. Between January and October 2025, this used to average just over 2 million net subscribers every month. So, a multi-fold increase in subscriber growth.

Jio and Airtel continue to drive this growth in subscribers, but Vi has finally stopped haemorrhaging subscribers. It has seen (modest) subscriber additions in the last 3 months after sustained subscriber loss in the preceding few years. Also worth noting is that Airtel has been gaining market share, and at 38%, its market share in the subscriber base is only marginally lower (~1.5ppt) than that of Jio. At its current rate, Airtel will catch up with Jio in the next 12 months.

That’s it for this week. See you next week…