Sluggish Exports, Rising Crude, China's Exports still growing and more...

This Week In Data #129

In case you missed, we published the first edition of our annual publication - Fiscal Matters Handbook. Spanning over 120 pages, this is a concise reference book to understand India’s public finances better. From the way the government collects its revenues to how it spends and how much deficit it runs. How the revenue and expenditure pattern of Central government differs from that of the State governments and how the different states differ from each other in terms of their revenue and expenditure profiles. Clients can download a copy from here, others can drop us a line and we can send a copy.In this edition of This Week In Data, we discuss:

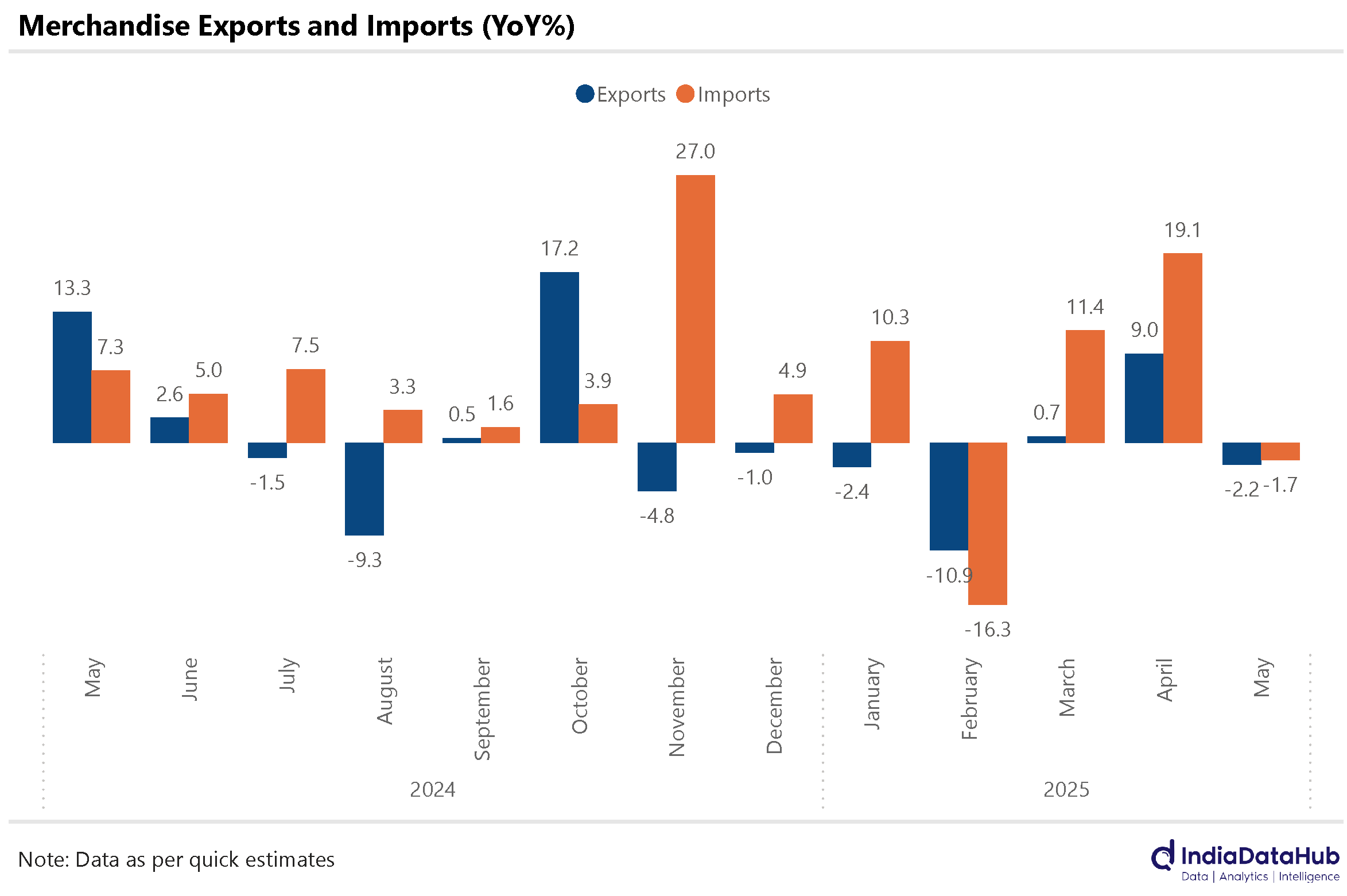

Merchandise exports and imports declined in May, largely due to lower Petroleum exports and imports

WPI Inflation remains modest suggesting muted cost pressures

Crude Oil prices have surged, but may not impact inflation immediately

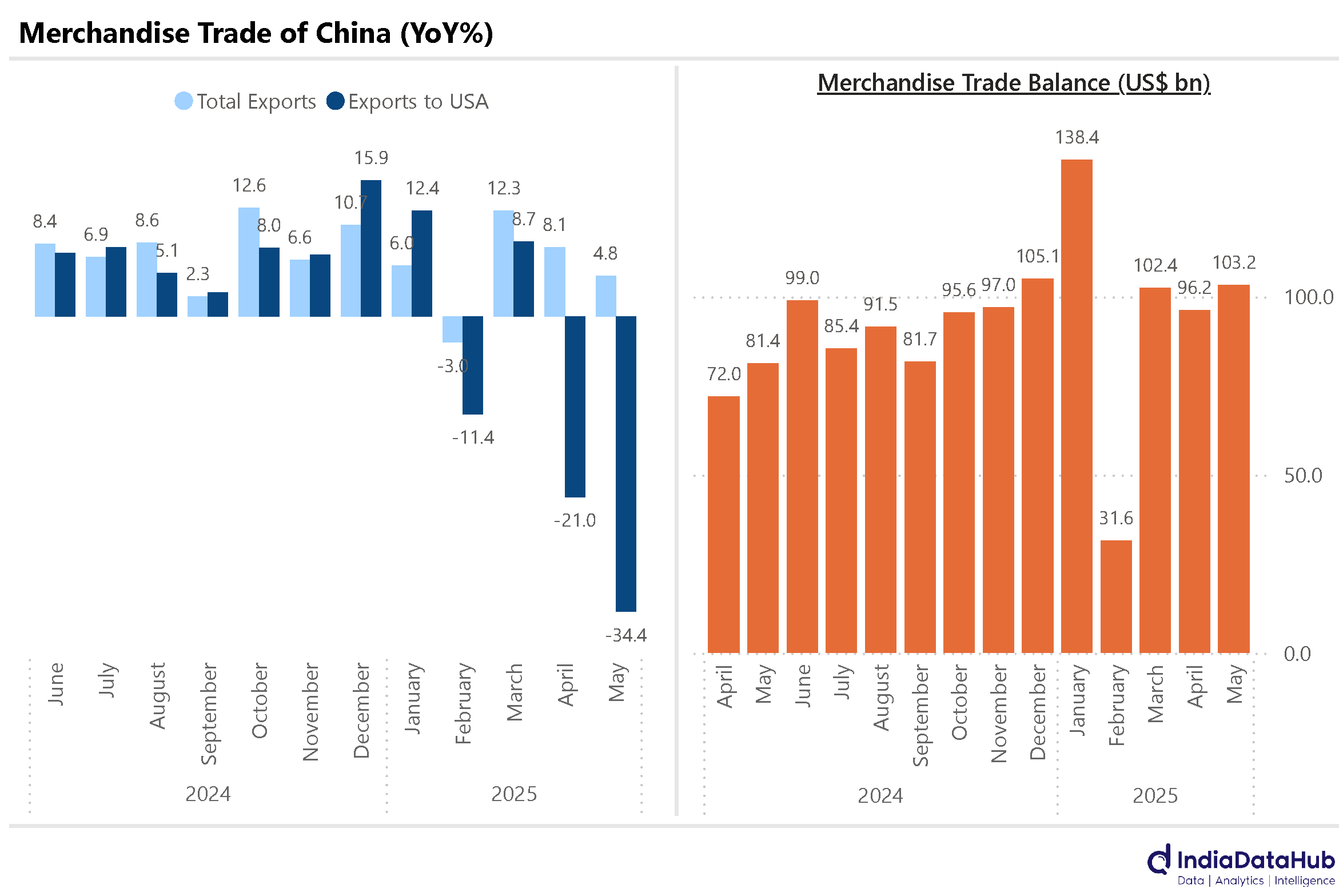

Despite a sharp 34% fall in exports to USA, China’s total exports rose in May

Fed keeps policy rates on hold with a rate cut likely only in September

Most other central banks also remain on hold with Brazil a key exception

India’s merchandise exports declined by 2.2% YoY in May, reversing the growth recorded in April. Petroleum products saw a 30% decline in exports and were the key driver of the decline. Excluding petroleum products exports rose 5%. Exports of Gems & Jewellery also declined 14% and were a large drag. On the flipside, exports of Electronics rose 50% YoY, the strongest growth in recent months. This follows 40% growth in April.

Merchandise imports declined by 1.7% YoY, after recording strong double-digit growth in the previous two months. Imports of Crude and Petroleum products declined 26% YoY and were the principal drag on imports. Excluding petroleum, imports rose 10% YoY driven by Chemicals, Metals, Machinery and Electronic goods.

Modest decline in both exports and imports resulted in the merchandise trade deficit narrowing sequentially to US$22bn in May from a 5-month high of US$26bn in April. On a YoY basis the trade deficit was largely unchanged.

WPI Inflation eased to 0.4% YoY in May, down 50bps from April. It is the lowest since March last year. Given that WPI inflation captures wholesale or factory gate prices, it is in a sense a leading indicator of goods inflation. And WPI manufacturing inflation fell to 2% YoY in May and it is lowest since October 2024.

So, the manufacturing sector in aggregate, is not seeing significant price pressures and this increases the confidence that core CPI (at least the goods component of it) will remain contained.

That said, Oil prices have increased in recent days due to the conflict in the Middle East. Crude Oil prices have risen almost 20% since the start of June and are inching towards US$80/bbl. While this should ordinarily be a drag on inflation, there is an offset.

The PSU OMCs have not really cut fuel prices in the last few months when Crude oil prices fell sharply. And thus it is very likely that despite the increase in crude oil prices, domestic prices of retail fuels will not see any material increase. So this increase in crude oil prices will not, at least in the short term, cause an increase in CPI.

China’s merchandise exports increased by 4.8% YoY in May. This was despite a sharp 34% decline in exports to the USA. In contrast, exports to Qatar surged by 143% during the same period. Machinery and Electrical Equipment exports increasing by 6.9%, and Transport Equipment exports rising by 10.2%.

Merchandise imports declined by 3.4% YoY in May with imports from the USA declining 17% on a YoY basis. Imports of Machinery and Electrical Equipment increased by 10%, reflecting strong industrial demand while imports of mineral products dropped sharply by 14.2%. Increase in exports and decline in imports meant that merchandise trade balance increased sharply and remained around US$100bn for the third consecutive month, almost 25% increase on a YoY basis.

Lastly, we had a host of central bank rate decisions last week. And generally, they maintained status quo. The US Federal Reserve decided to maintain the target range for the federal funds rate at 4.25% to 4.5%. This decision comes amid continued reasonable strength in labour market, despite fluctuations in net exports. The US Fed has remained on hold since the start of the year. Futures markets are implying that the Fed will next cut interest rates in its September policy meeting.

The Bank of England also kept policy rate unchanged at 4.25% as did the Bank of Japan which left the policy rate unchanged at 0.5%. China’s PBoC also kept its policy rates unchanged last week. Consequently, the 1-Year and 5-Year Loan Prime Rates (LPR) remain steady at 3% and 3.5%, respectively. In Turkey, the Central Bank has also kept its repo rate unchanged at 46%, marking the second consecutive time this rate has remained unchanged. The one exception was Brazil where the Central bank raised the Selic rate by 25bps to 15%.

That’s it for this week. See you next week at the end of what looks like will be a choppy week for the markets given the developments over the weekend.