Strong corporate tax collections, Recovering GST growth, Weak services exports and more

This Week In Data #168

In this edition of This Week In Data we discuss:

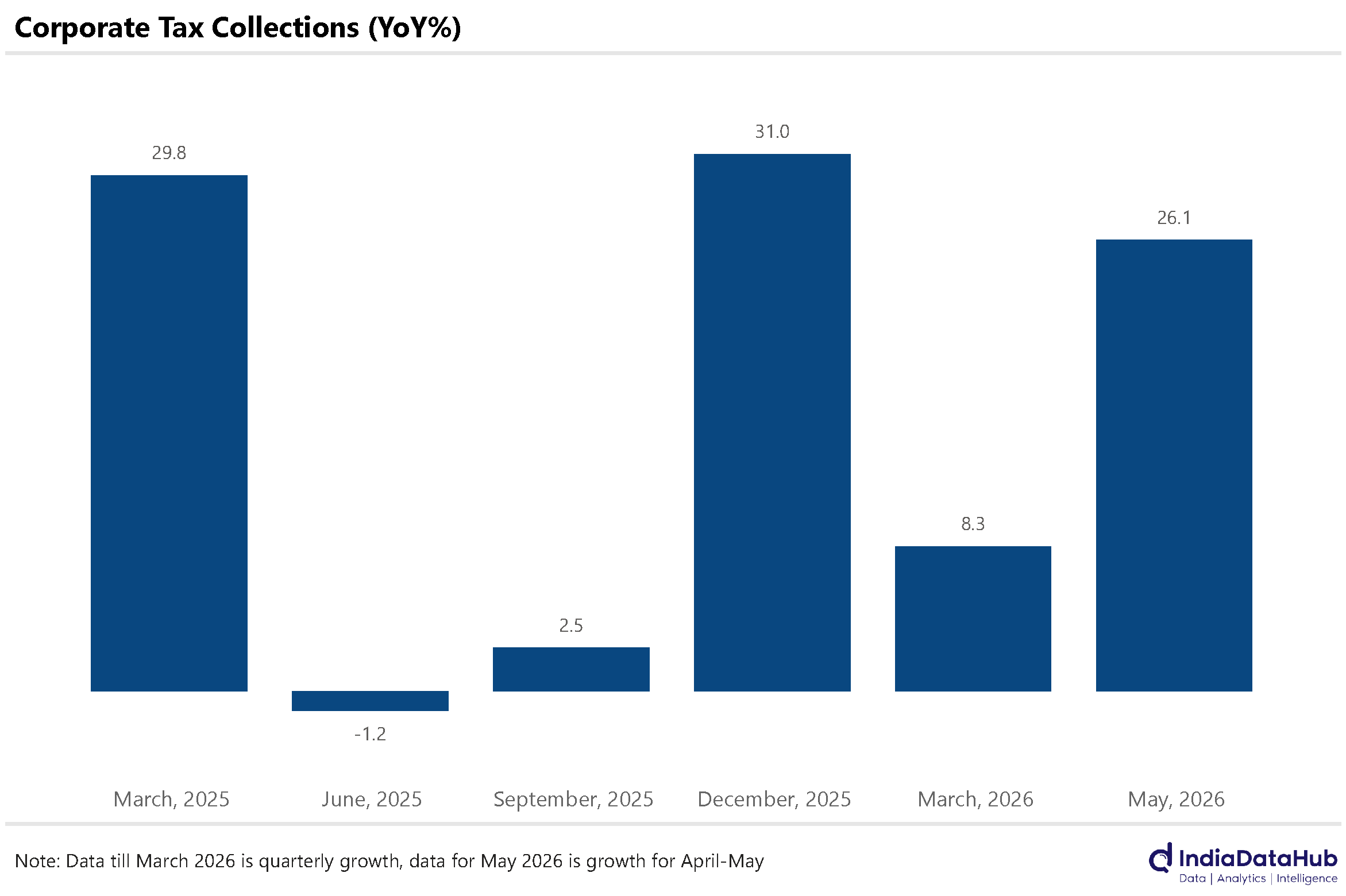

Corporate Tax collections see strong growth during the June quarter

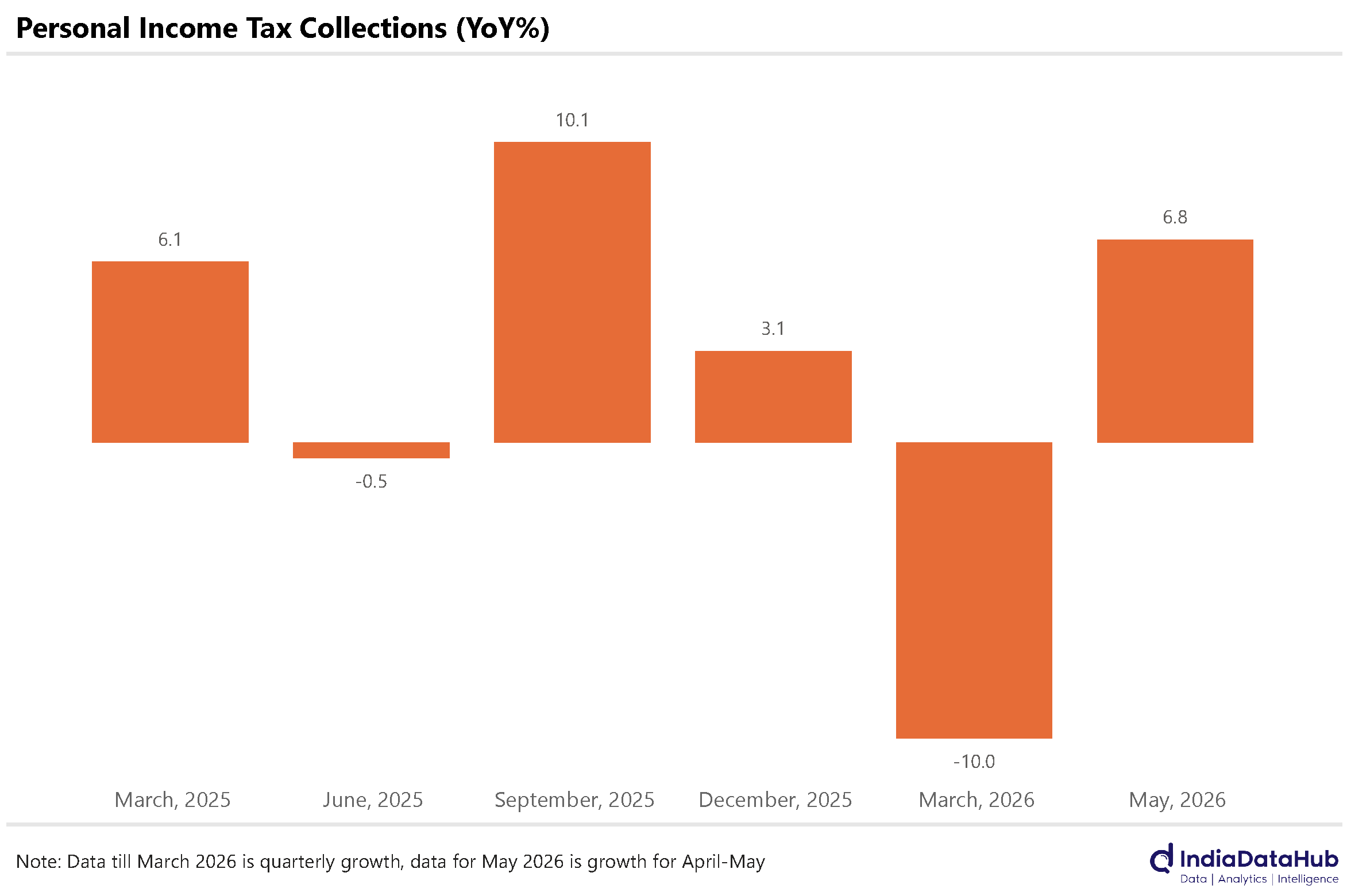

Personal Income tax collections recover but remain modest

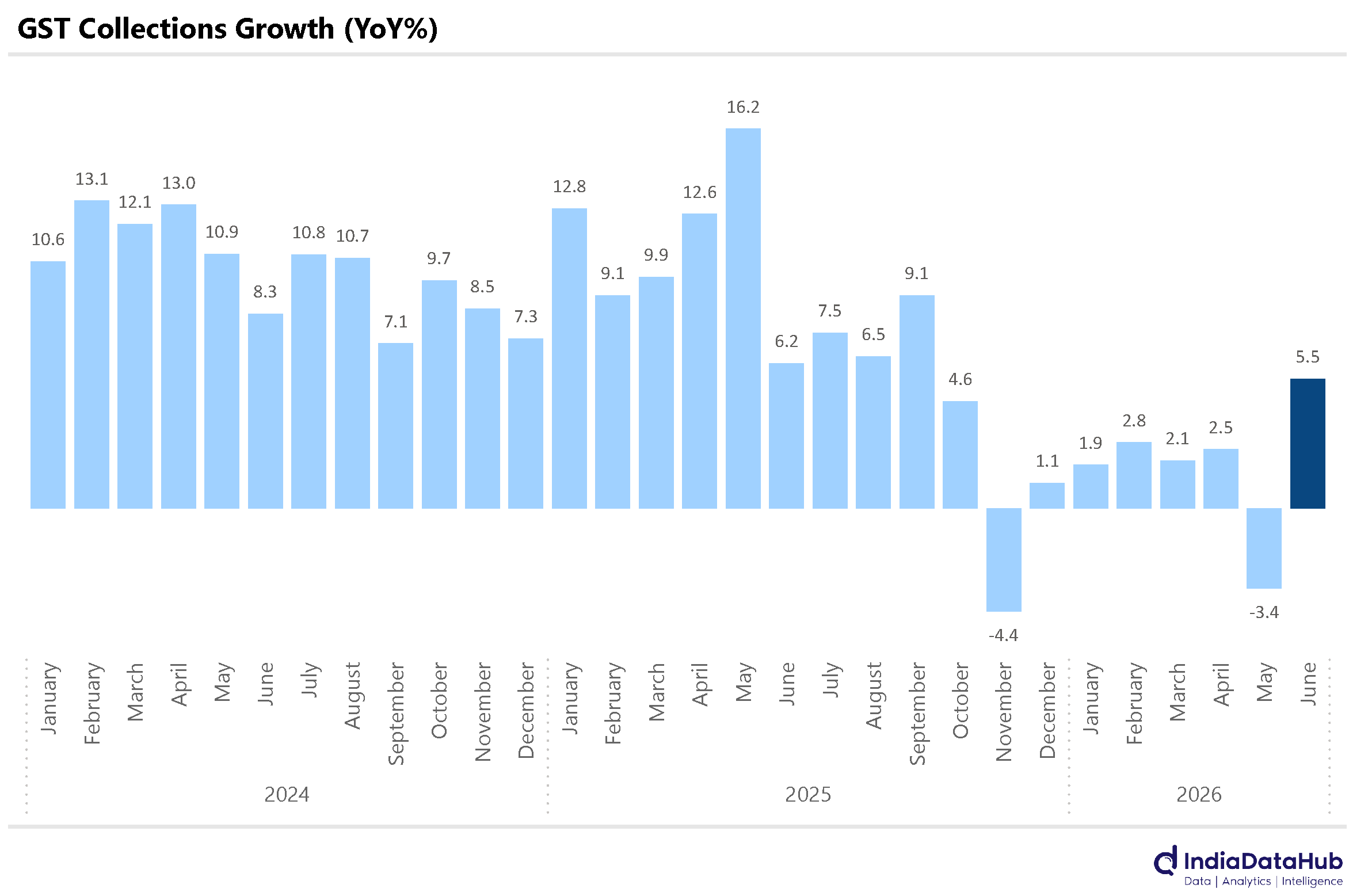

GST collections growth at highest since September last year

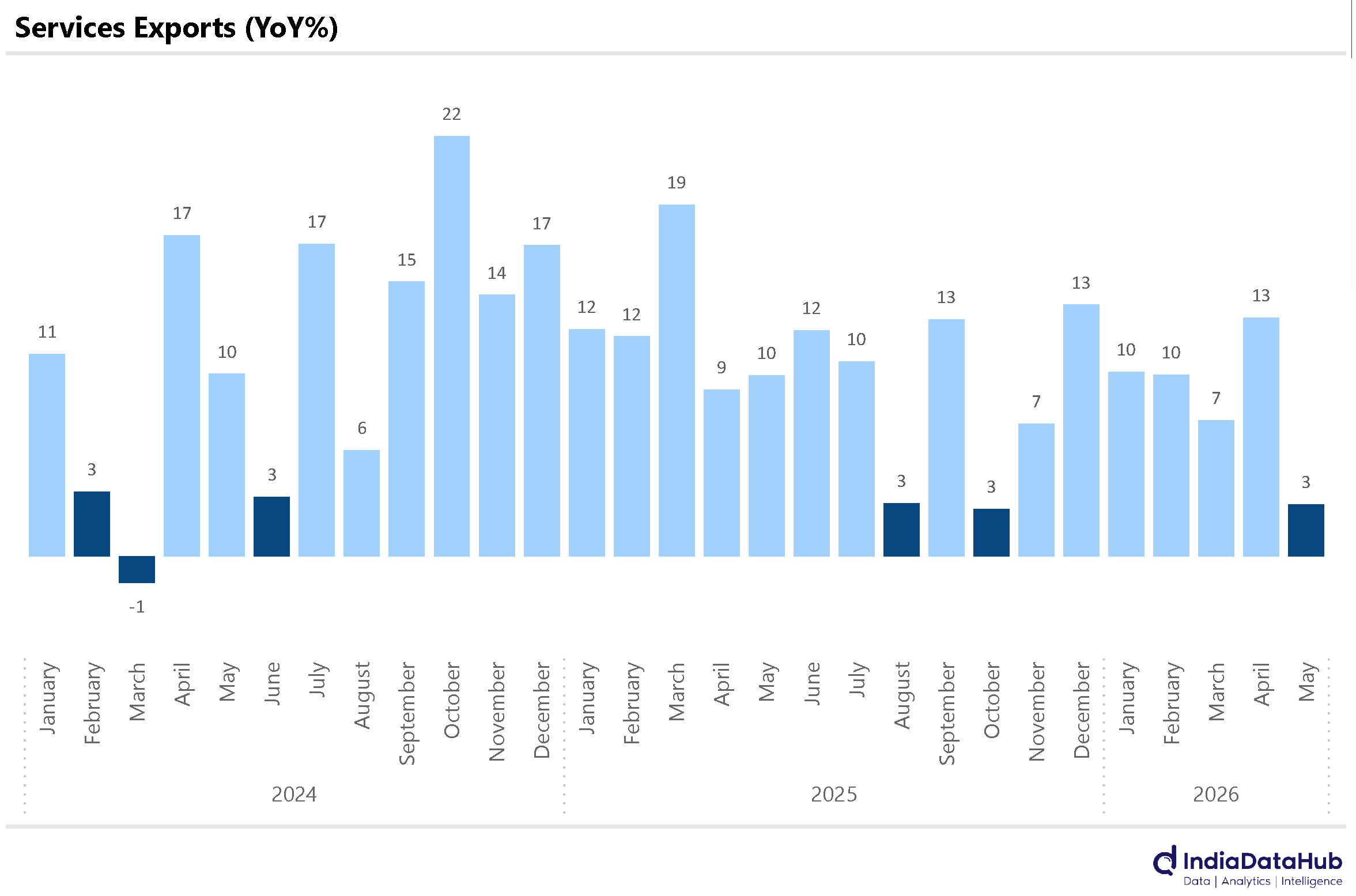

Services exports decelerate sharply in May

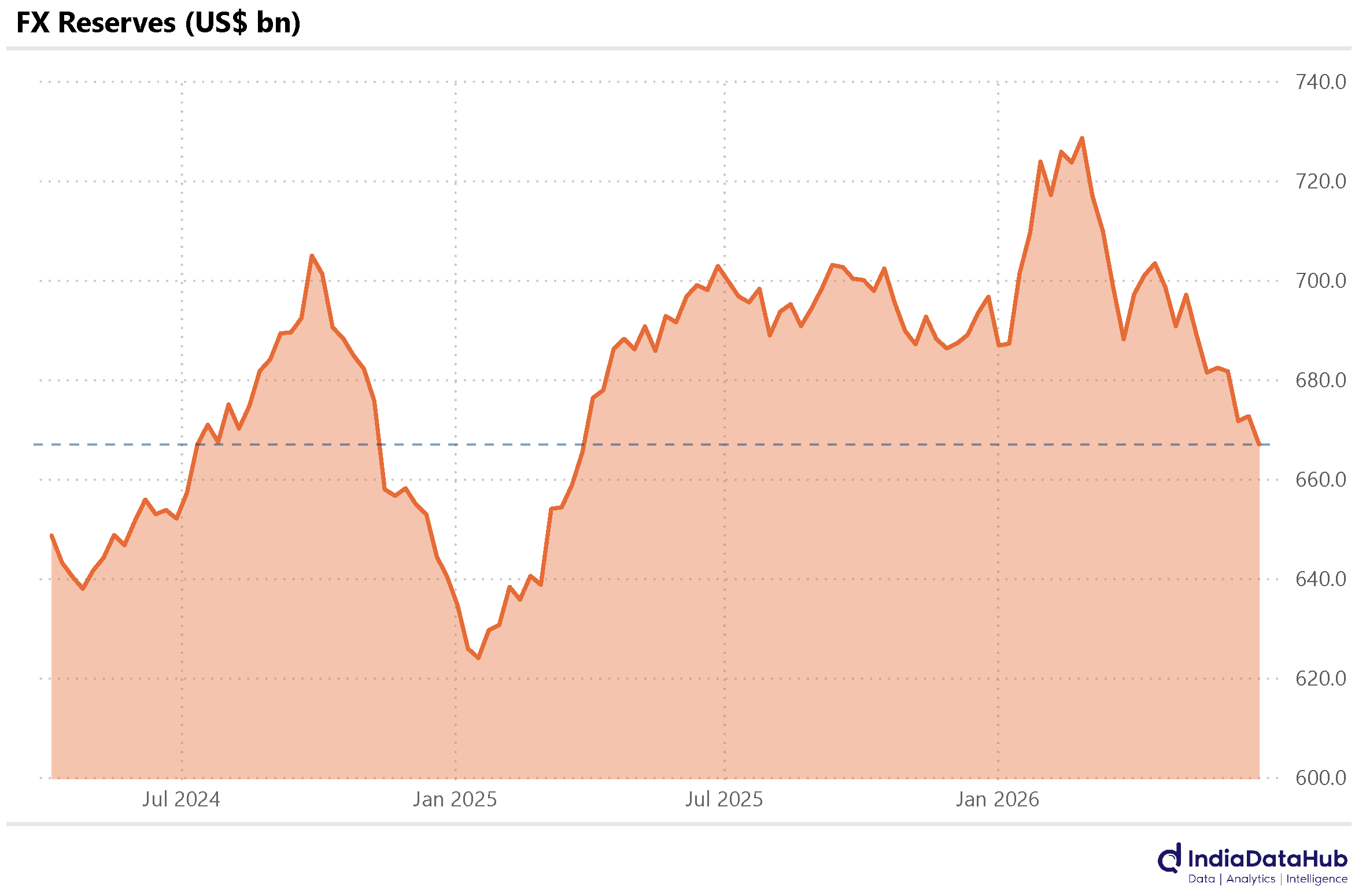

FX reserves have steadily declined to 15-month low

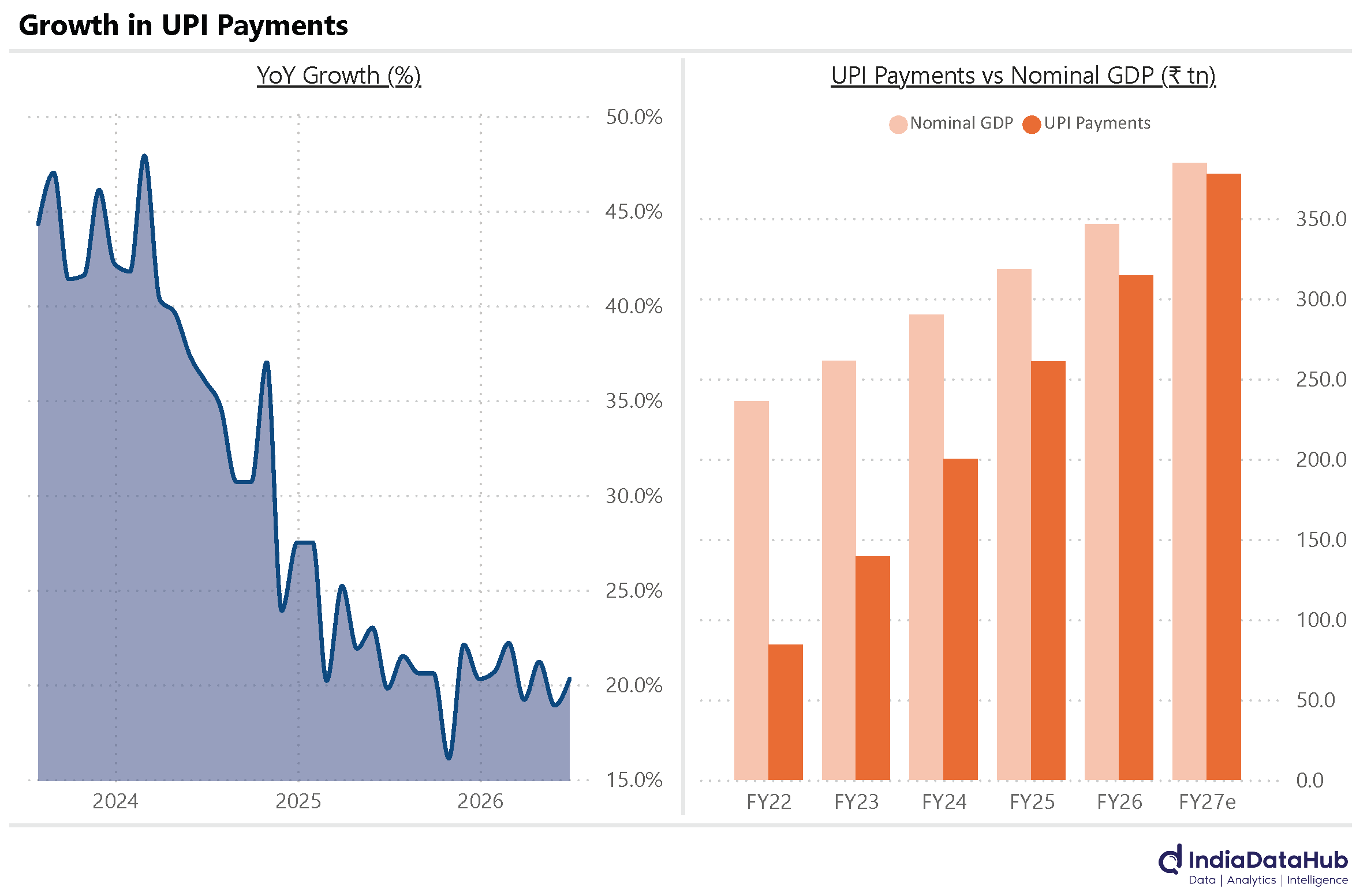

UPI payments will equal India’s nominal GDP in the current year

Corporate tax collections have seen strong growth in the first two months of this financial year. While April saw high-teens growth in corporate tax collections, May saw over 30% growth in collections. Cumulatively, thus, the first two months have seen 25% growth in corporate tax collections. And these two months had seen significant macro headwinds with higher oil prices and a falling rupee. So strong growth in corporate tax collections despite these headwinds suggests resilient underlying corporate profitability growth.

In contrast, personal income tax collections remain weak. They have seen a modest 7% growth in collections so far this year, implying they are even undershooting the nominal GDP growth, which is likely to have been in the low double digits during this period. However, this is an improvement from the almost 10% decline seen during the March quarter. So, while growth is modest, it is still an improvement.

GST collections, however, ticked up. After a decline in May, overall GST collections grew 5.5% YoY in June. This is the highest growth since September last year. Recall that the government had rationalised and cut the GST rates effective September last year. And since then, GST collections had understandably been subdued – even declining in a couple of months. That they are now seeing an uptick even before the rate cuts are in the base suggests improving underlying momentum.

May was a bad month for services exports. They grew a modest 3% YoY, which is the slowest growth in the last few months. The previous few months had seen ~10% growth each month. So, this is a fairly sharp deceleration in growth.

More importantly, imports grew faster than exports at 6% YoY, which led to the services surplus declining YoY for the first time in over 2 years. A lower services surplus when the merchandise deficit was high due to higher oil prices and negative portfolio flows would have been a contributory factor to the pressure on the rupee.

FX reserves have been declining in recent weeks. As of the last Friday of June, India’s FX reserves stood at US$667bn, the lowest since March last year. From its peak in February this year, reserves are down by over US$60bn. And it is not just Gold which is contributing to the fall in reserves. While the decline in the price of Gold is dragging down reserves, foreign currency assets have also fallen.

Of the US$61bn decline in reserves since February this year, roughly half is due to lower foreign currency assets and another half is due to the decline in value of Gold holdings – RBI’s physical gold holdings having remained unchanged (latest data as of end of May).

Lastly, the remarkable growth in UPI payments continues. While the growth rate has slowed down from the 40-50% growth of 2023-24, it has stabilised at ~20% for the last few quarters now. June itself saw 20% YoY growth in payment value.

At this rate for the full year FY27, the value of UPI payments will be equal to India’s GDP. A decade ago, in FY16, UPI payments were basically zero. And just 5 years back, in FY22, UPI payments were just about a third of India’s GDP. And it is on this base (~US$300bn of spend a month) that UPI is still seeing 20% growth every single month.

That’s it for this week. See you next week…