In this edition of This Week In Data, we discuss:

Capital flows are a problem and not just portfolio flows

Bank credit has seen a sharp uptick

Incremental Credit-Deposit ratio is close to 100%

Rupee continues to depreciate against the USD and other currencies

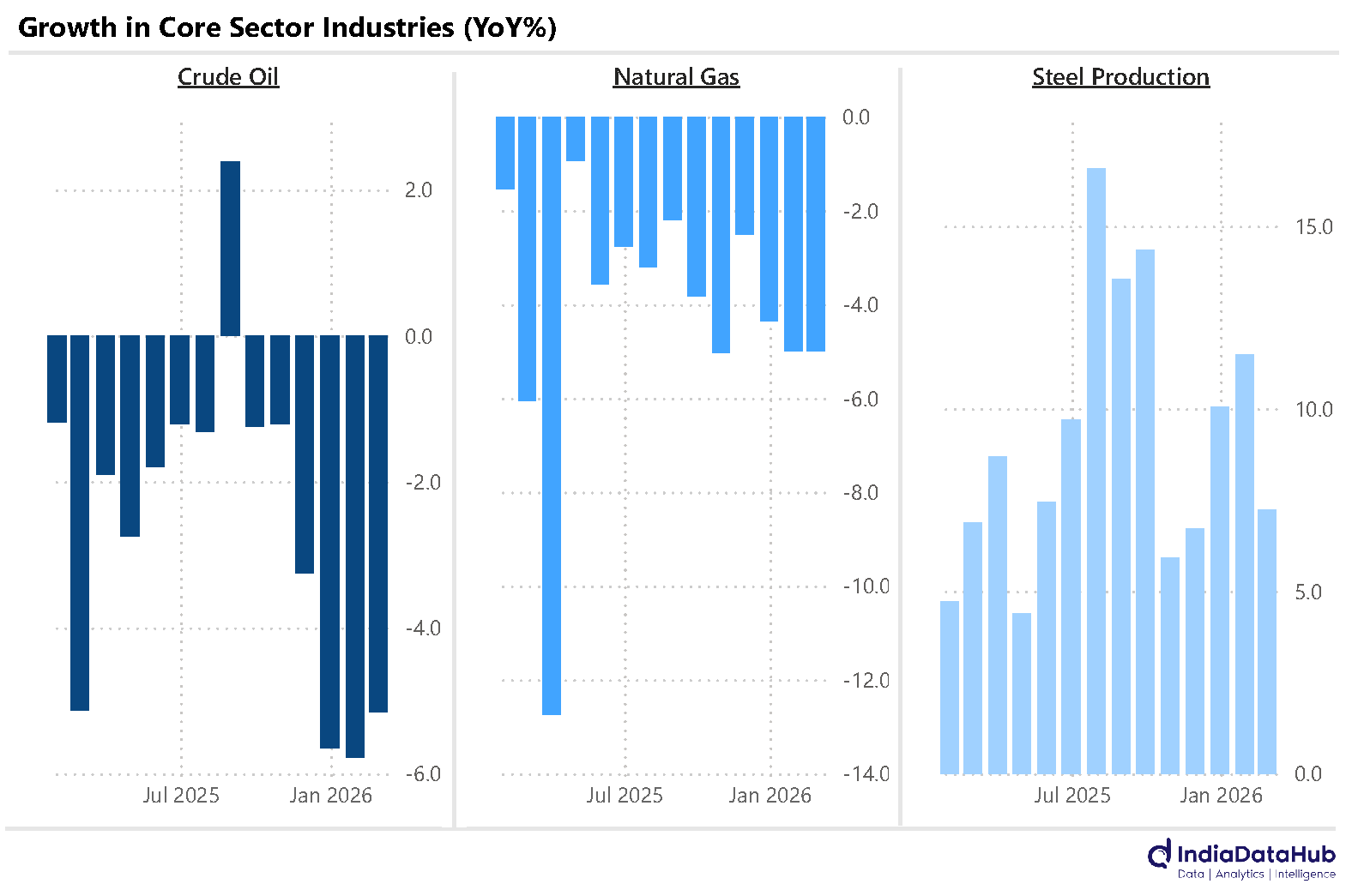

Core sector growth remains sluggish with petroleum being the key drag

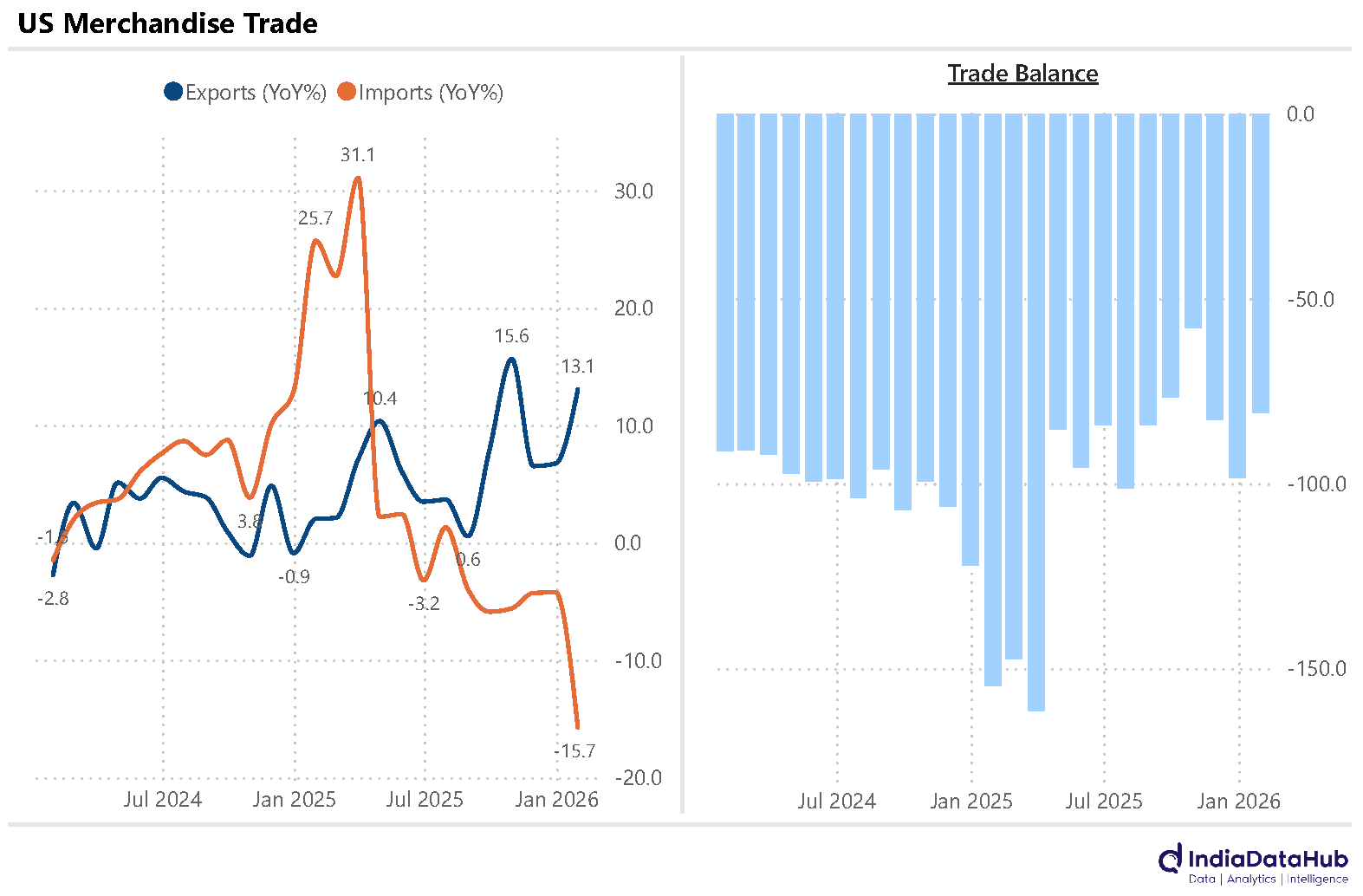

US trade deficit narrows sharply in January as exports rise and imports decline

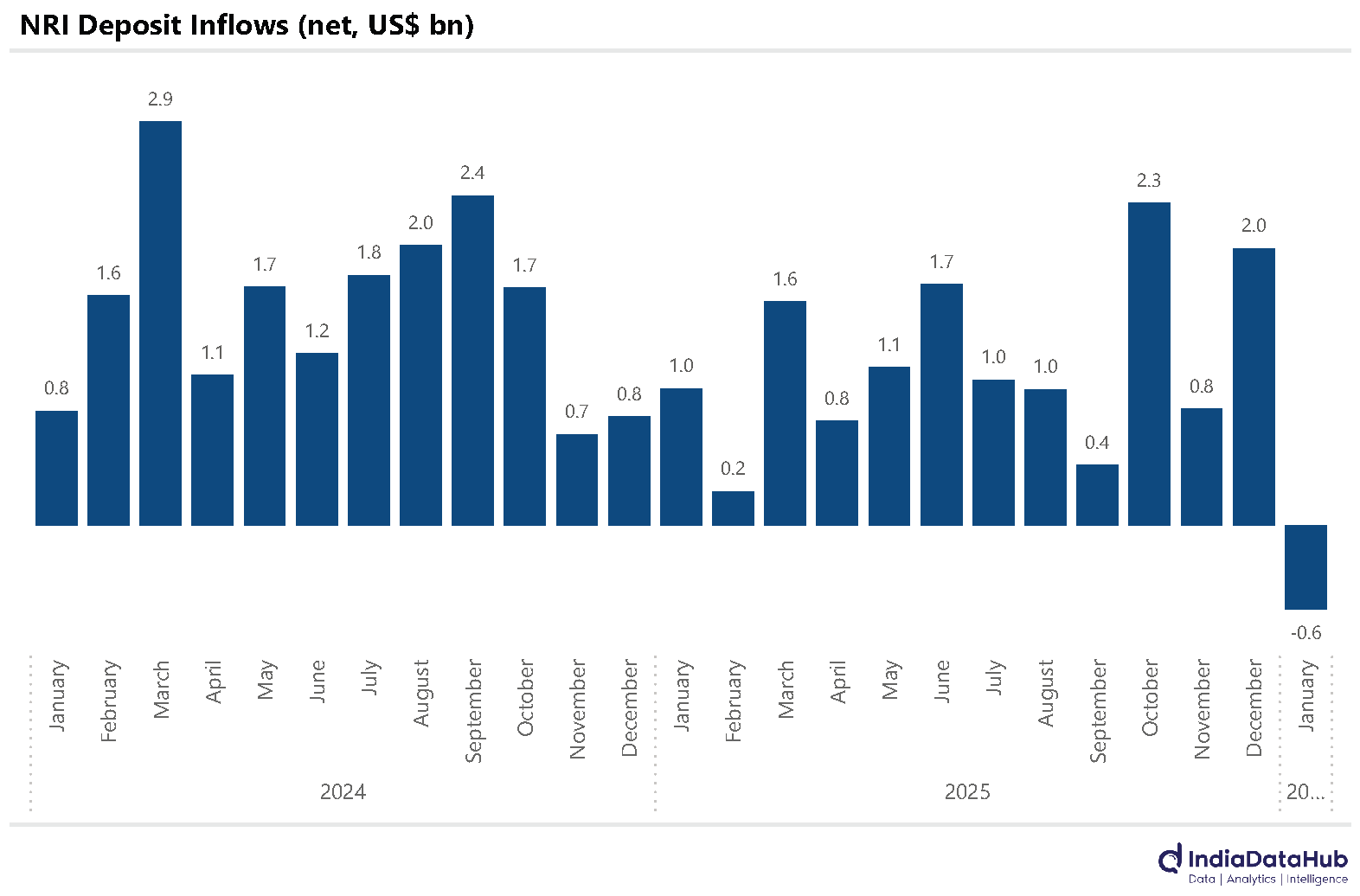

The rupee is under pressure as capital flows have turned adverse. And while we are aware of the selling by FPIs, the challenges in capital flows are much more than just FPIs. NRI deposits, for example, which used to be a steady source of inflows, turned negative in January – there were net withdrawals of US$ 600 million. For reference, the last quarter of 2025 had seen inflows average US$1.7bn, so a delta of over US$2bn in January. Outward remittances have also, not surprisingly, increased. January saw US$2.7bn outflows under the LRS, up US$500mn compared to the preceding few months.

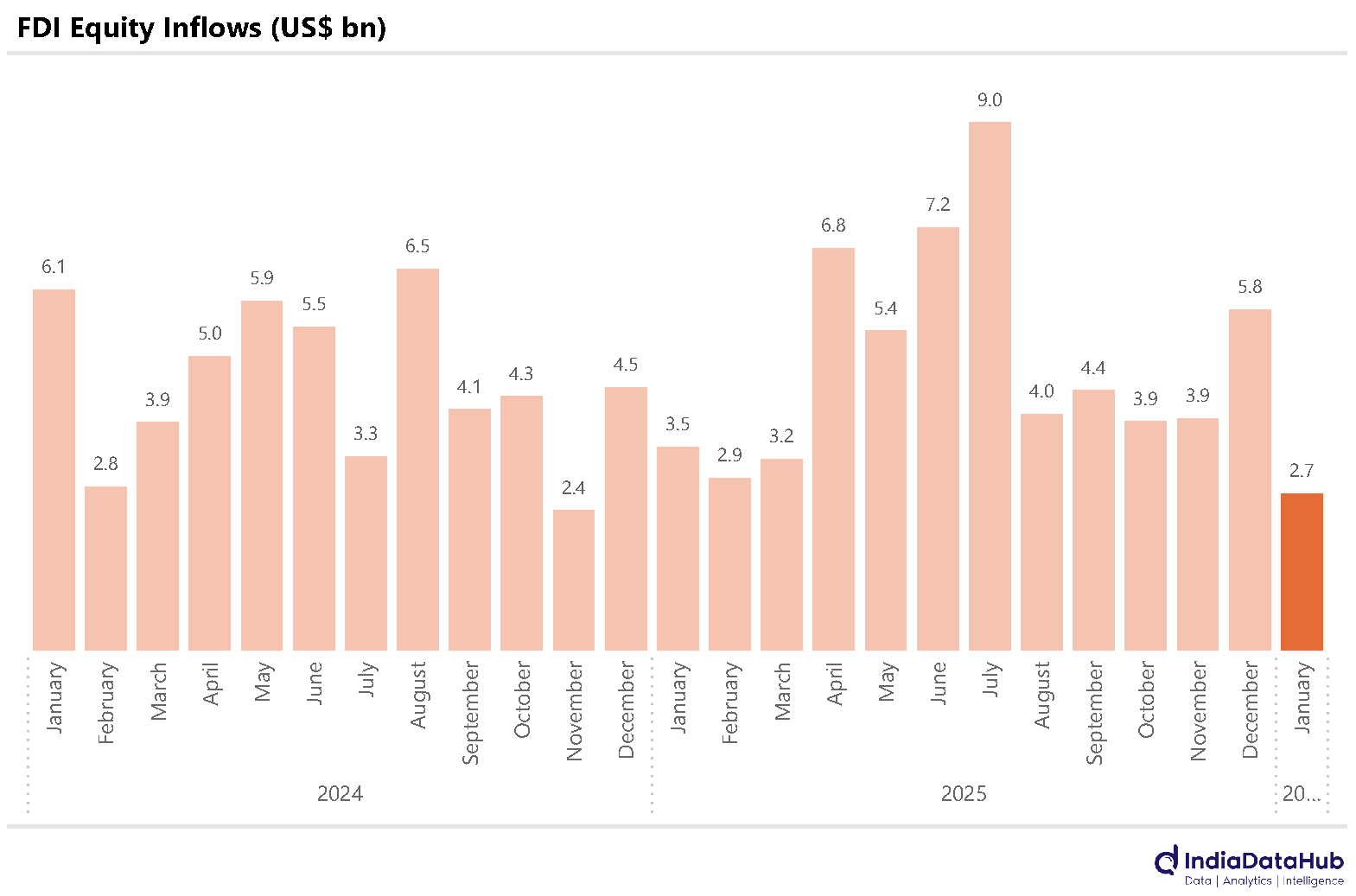

And FDI continues to struggle. January was the sixth consecutive month of negative net FDI. January saw a negative net FDI of US$1.4bn, the highest in the last 3 months. And this is in large part because the actual equity FDI received by India in January was at a 14-month low of US$2.7bn. For reference, the preceding 3 months saw India receive an average equity FDI of US$4.5bn, almost US$2bn higher.

The only component of capital flows that has improved in recent months is the ECBs. January saw ECBs totalling US$5.3bn being approved by the RBI, the highest since March last year. Some corporates are being brave (or contrarian?) raising overseas debt with the rupee is seeing sharp depreciation!

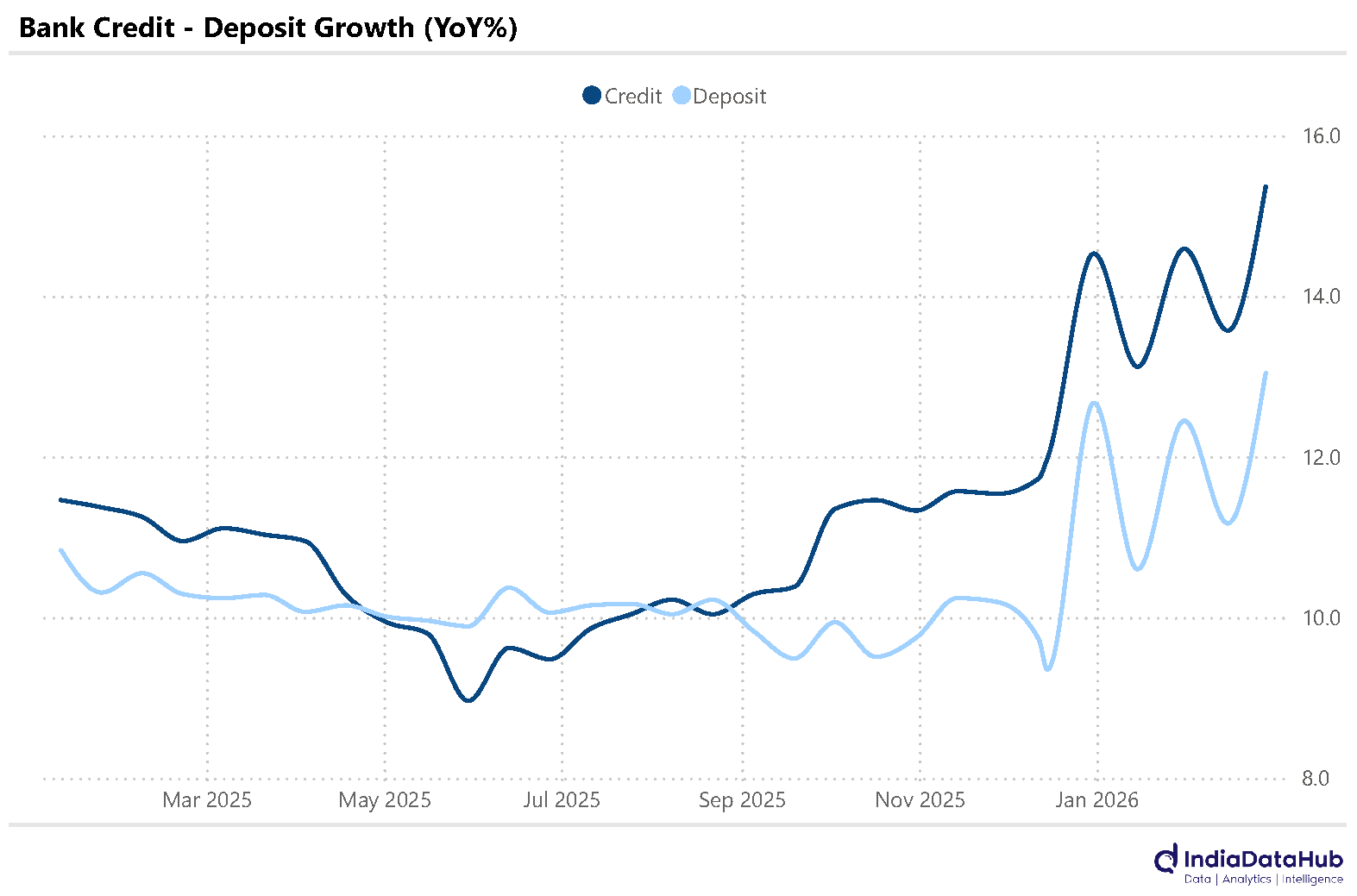

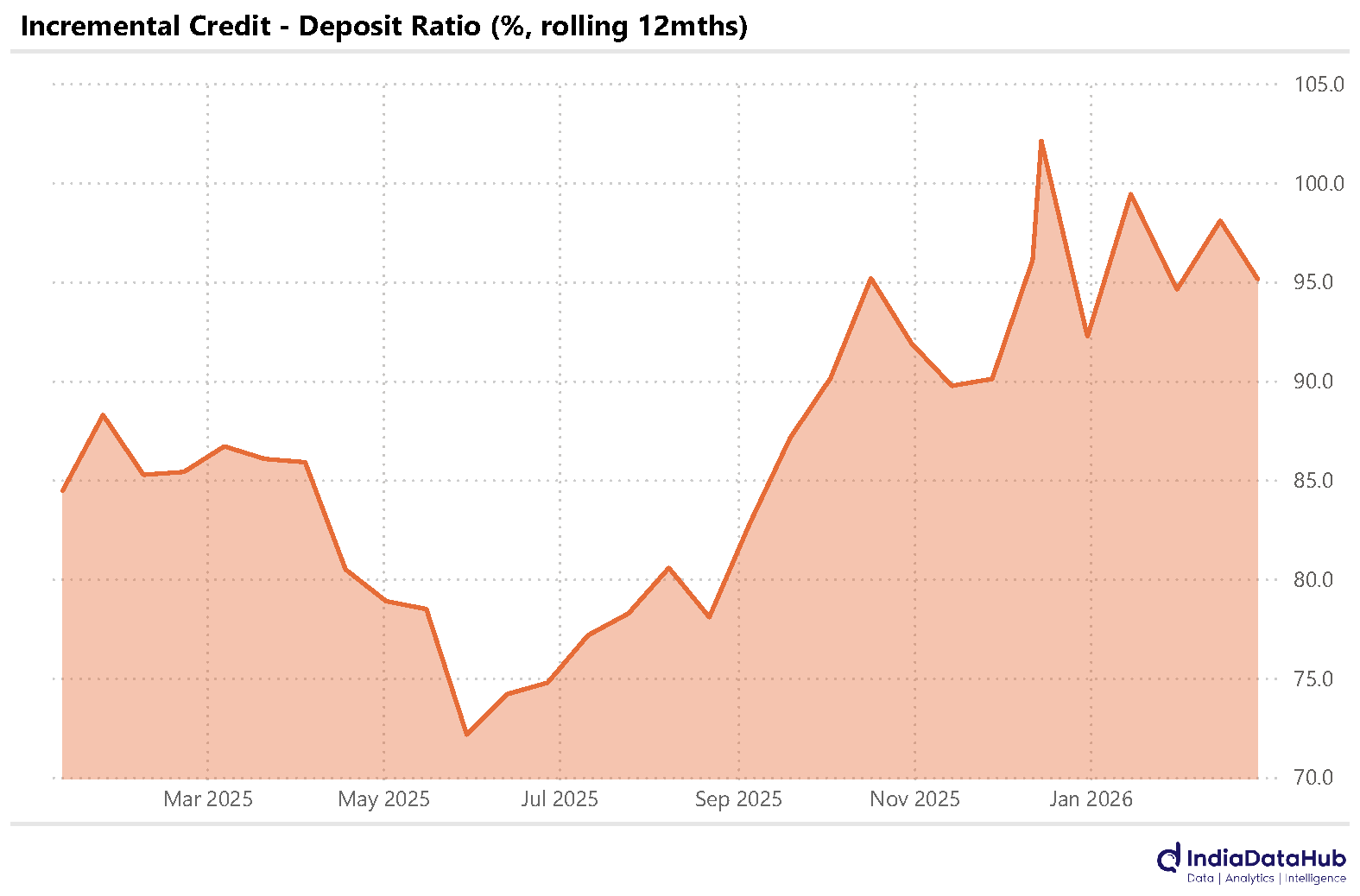

Credit growth has accelerated sharply in recent months. As of the end of February, overall credit growth had accelerated to over 15% YoY, almost 4ppt higher since November. Deposit growth has also similarly picked up, and at 13% it has similarly increased by ~4ppt in the last few months. The credit-deposit ratio is now running over 82%, and the incremental credit-deposit ratio is now running close to 100%. While it does not appear so, the banking sector is running red hot.

The rupee continues to depreciate against the US Dollar. However, as we have highlighted before, the big picture is of the rupee’s depreciation against most major currencies, not just the USD and the sheer quantum of decline. Thus, over the past year, while the USD Index fell by ~4%, the INR Index fell by 11%. The INR has thus fallen by over 10% against most major currencies.

What is surprising is that despite this, we have not seen a material increase in inflation. And this has allowed interest rates to continue to remain low. The recent rise in oil prices will complicate this picture, but at least in the short-term, the RBI is likely to see through any increase in inflation attributable to the rise in oil and gas prices.

The Core Sector grew by 2.3% YoY in February, slowing from the 4.7% growth recorded in each of the previous two months. Out of the eight industries that comprise the core sector index, three sectors registered a decline in growth. Natural gas production contracted by 5% YoY in February, marking the 20th consecutive month of decline. Similarly, crude oil production fell for the sixth straight month. In contrast, steel production showed strong performance, recording a 7.2% YoY growth in February.

Lastly, the US goods trade deficit narrowed sharply in January, declining by US$17.7 billion to US$80.8 billion on a seasonally adjusted basis. Exports grew by 13% year-on-year in January, up from a 6.8% YoY increase in the previous month. Imports declined for the sixth consecutive month in January, with the pace of decline rising to 16% YoY. US exports to China declined for the thirteenth consecutive month. Imports from China declined for 12 straight months.