Telecom, Rupee, Aviation, Rains and more...

This Week In Data #68

In this edition of This Week In Data, we discuss:

Strong subscriber addition for wireless operators

Airtel, Jio continue to grow while Vi and BSNL lose subscribers

Wireless ARPU by Telecom Circle

Strong growth in NRI Deposits

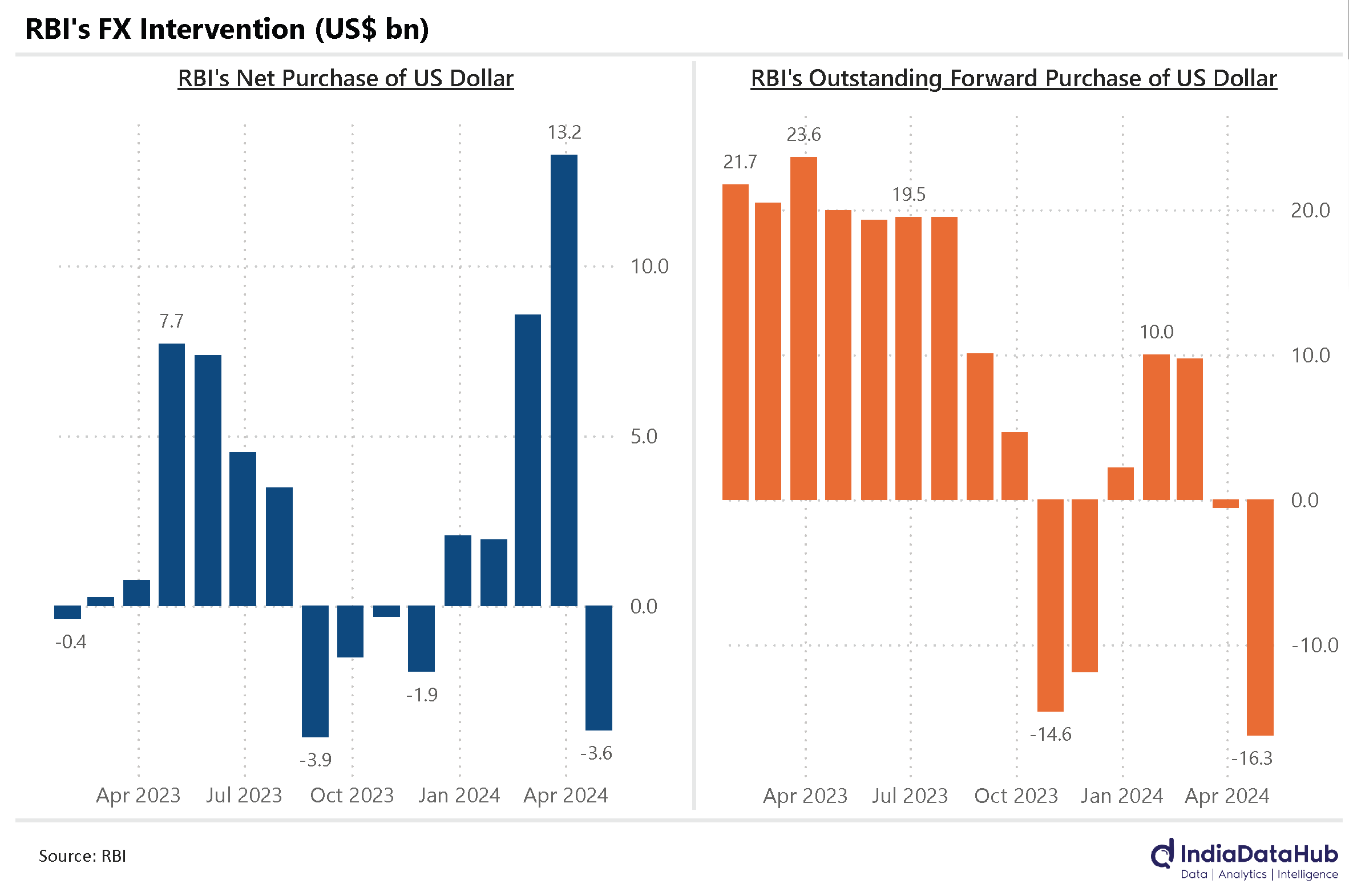

Rupee continues to outperform, helped partly by RBI

Slowdown in Aviation

Weak start to monsoon rains

In case you missed it, we released the first of our sentiment indices this week. These indices extract the meanings from unstructured data (in this case, text from the MPC minutes) and convert it to structured data. The initial findings are that these indicators correlate well with existing structured data sets. You can read more about it here. And as an additional validation, the RBI released the MPC minutes for June yesterday, and while the MPC is overall very optimistic about growth, the two members who dissented in June, have the lowest growth sentiment.Telecom operators have been seeing strong subscriber growth in recent months. April was the 12th consecutive month that the wireless operators have seen subscriber addition. In the first 4 months of 2024, the wireless operators have added 8.4 million subscribers, more than half of the subscriber addition in the full year 2023. At this rate, 2024 will be the strongest year for subscriber growth since 2017.

Both Jio and Airtel continue to add subscribers and gain market share while Vi and BSNL continue to see a decline in subscribers. In the first 4 months of this year, Jio has added almost 13 million subscribers while Airtel has added just under 5 million subscribers. Vi however has lost 4 million subscribers while BSNL has lost almost 5 million subscribers. Vi has lost subscribers every single month for the past 37 consecutive months – a cumulative loss of 64 million or just under 25% of its prior base.

And while we are talking of Telecom, here's a trivia. Users in which telecom circle run up the highest bills? One would expect, it will be the users in metropolitan areas – Mumbai or Delhi – where users would be running the highest bills. Turns out, that is wrong. As of December 2023, the latest period for which we have data, it is the users in the Andhra Pradesh circle (which includes Telangana) who run up the highest mobile bills at ₹181 per month, closely followed by Tamil Nadu and Karnataka. Mumbai and Delhi circles have an ARPU of less than ₹150 which is more than 15% lower than Andhra Pradesh! And the Kolkata circle has the lowest ARPU of all circles – even lower than Bihar or UP…

The trend of strong inflows under the NRI Deposit schemes continues. April was the 3rd consecutive month when net inflows exceeded US$1bn. The last three months have seen cumulative net inflows of US$5.6bn, the highest since the June quarter of 2015! India’s current account deficit is estimated to be just under US$40bn in the current year (FY25) and at this rate, the NRI Deposits themselves would fund almost 60% of it. And Portfolio flows and FDI is on top of it. So, as things stand now, the external account looks comfortable for the foreseeable future.

The stability in the exchange rate continues to manifest this. Over the past month, the rupee has depreciated by a modest 0.3%. The rupee continues to be amongst the best-performing emerging market currencies. For reference, the Indonesian Rupiah has lost almost 3% while the Brazilian Real has lost almost 7% and the Mexican Peso over 10% against the US Dollar.

What will also help the rupee is the willingness on the part of the RBI to defend it when flows get temporarily misaligned. In April for instance, when there were large FPI outflows, the RBI intervened by selling USD worth US$3.6bn and also increased its net short forward position to the highest in 4 years.

The aviation market has slowed down. May was the 5th consecutive month of low single-digit growth in the number of passengers carried by the airlines on domestic routes. Domestic aviation which generally grows faster than the growth in the economy is now growing slower. And the PLF or the passenger load factors have started dropping on a YoY basis. In April, the industry PLF dropped by 1.5ppt and while we do not have aggregate data for May, both Indigo and Vistara have seen PLF drop in May this year compared to last year.

As we have highlighted before, May data in general has been soft across the board and that is a bit disconcerting.

Lastly, rainfall. We are three weeks into the official monsoon season and while the forecast is for above-normal rains for the full season, so far, we are running a deficit of 17% relative to normal. Rains over Northwest India have been especially poor at just 40% of normal while even Central India has also seen only 70% of normal rains so far. South India is the only region that has so far seen above-normal rainfall. But these are still early days. Normal rains in July and August hold the key from a Kharif crop perspective.

That’s it for this week. Have a good weekend!

Hello. Thank you for the newsletter. Are yo sure about the Airlinr passenger traffic yoy numbers in the chart, I looked at teh DGCA reports and the growth numbers look off to me. Thanks.