Tighter liquidity, Payments in single digits, US GDP and more...

This Week In Data #41

In this edition of This Week In Data we cover:

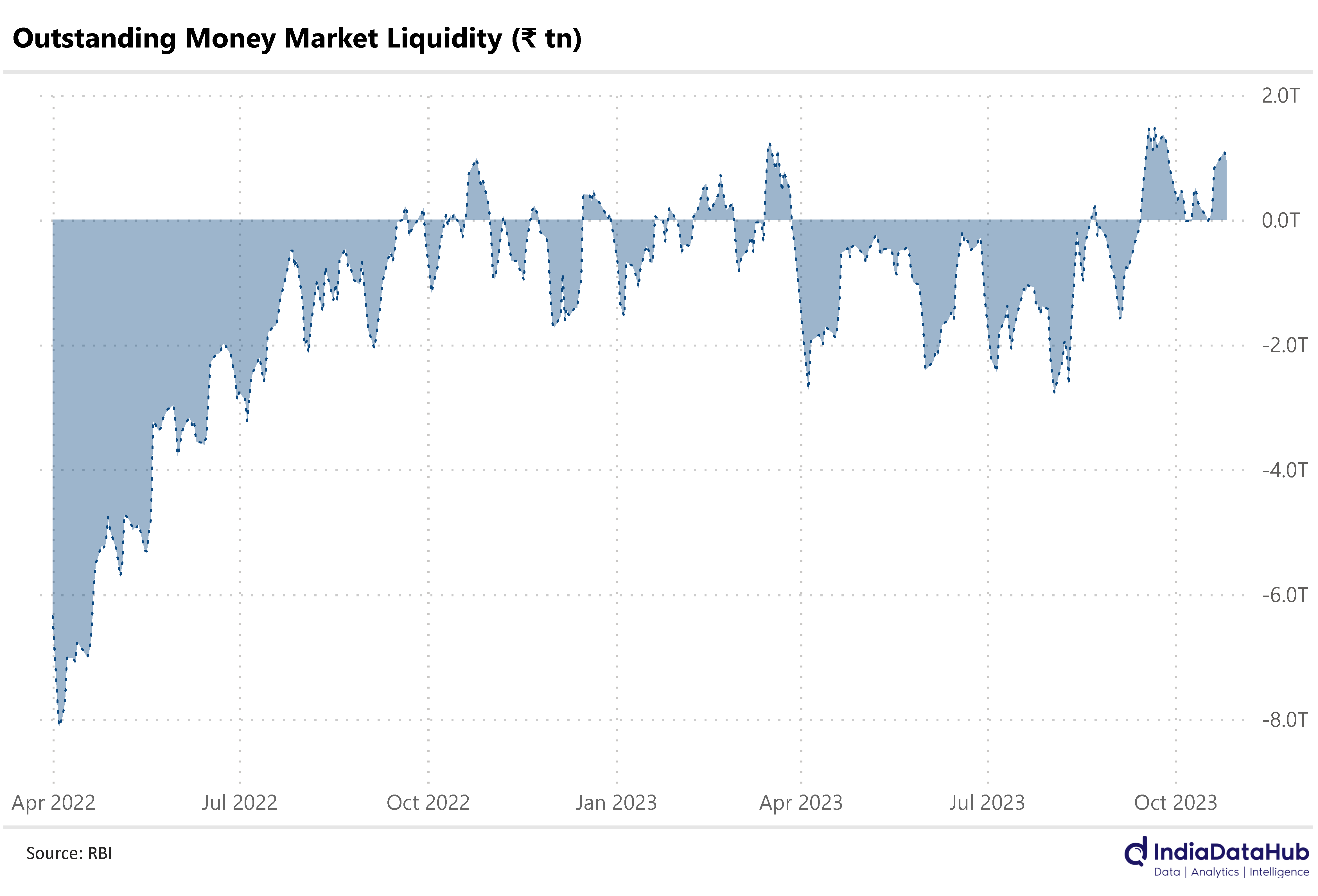

The tight domestic liquidity

Implications of tighter liquidity on interest rates

Sharp deceleration in payments growth in September

The resurgence in Cheques

Strong US 3Q GDP growth

The ECB takes a pause

Negative real interest rates in Turkey at 35%

In case you missed, we introduced Mutual Fund Analytics on IndiaDataHub. We begin with detailed aggregate industry data and individual fund house level data. And we will follow with scheme and portfolio data next month. While we are still in active development mode, this video gives you a look at the beta version that current subscribers can access and test.Domestic money market liquidity is now in a deficit. Which means the RBI has infused liquidity. This week the liquidity deficit averaged ₹1 trillion. This has happened even as liquidity impounded under the incremental CRR was fully released in early October. Effectively, all the excess liquidity generated from the inflow of ₹2k denomination notes has been drained away through a combination of cash withdrawals and banks using that liquidity for lending or investing purposes. With FX volatility, the RBI has had to intervene to support the rupee in August (and almost certainly in September as well) meaning that FX has also acted as a drain on liquidity.

And what this has meant is that the overnight call rate is averaging close to 6.75%, almost 25bps above the policy repo rate. This is out of sync with the RBI’s explicit aim to keep the overnight policy rate close to the policy repo rate. Effectively, monetary policy is tighter than what the current level of the repo rate suggests it is. And perhaps, this is broadly what the RBI desires currently. The RBI has not announced or undertaken any large OMOs to infuse liquidity. Indeed, at the margin, the RBI small OMOs that the RBI has been undertaking are draining liquidity from the market. And as we are amid the festive season (till Diwali), cash holdings generally rise and that is an additional pressure on domestic liquidity. So, unless the RBI steps in, looks like this tight liquidity is likely to persist for at least a few more weeks.

In a sense this is the reverse of what was happening through 2020, 2021 and early 2022 when the effective policy rate was well below even the reverse repo rate due to surplus liquidity. We called it monetary easing by stealth. And what we are seeing now is monetary tightening by stealth. Part of the reason why the RBI prefers this is that it can dial this in on an everyday basis whereas the actual monetary policy is set to bi-monthly review. But this raises the question as to whether the RBI should be effectively bypassing the MPC through liquidity instruments. But that is another discussion. But suffice to say that the longer this persists, this will transmit into the real economy through higher lending rates.

We got the payment data for September earlier this week. And overall payments growth saw a sharp slowdown to just 8% YoY. This is half the growth rate of the preceding few months and is the slowest growth in over two and half years. Growth in the number of transactions however remained strong at over 40% YoY, broadly the same pace as in the preceding few months. It is thus possible that lower inflation is finally flowing through to payments.

As an aside, here’s some trivia that shows how large UPI has become. The growth in UPI payments in September this year, relative to September last year, is more than 2x of the total payments through credit, debit and wallets combined in September. So the growth in UPI payments is now more than the total payments through cards and wallets!

However, Cheques have been an interesting contrast in the last few months. Cheque payments have been on a structural decline due to the rise of digital modes of payments. During the pandemic, cheque payments however declined sharply. In FY21, overall payments through cheques declined almost 30% YoY. However, since then they have seen a revival which is playing out even during the current year. In FY22, cheque payments grew 18% YoY and in FY23 they grew 8% YoY. And so far in 1HFY24, they have grown 1% YoY. Of course, in absolute terms, the total quantum of payments is still below the pre-pandemic level (FY20). But that they have continued to grow well after the economy has moved on from the pandemic is counter-intuitive.

And it is not as if the quantum of payments through cheques is small. The total quantum of payments through cheques in FY23 at ₹72 trillion is almost 3x of Credit and Debit cards put together. So, either a set of payment makers and receivers (payment makers – did we just invent a new phrase?!) cannot migrate to digital modes of payment or do not want to migrate to the newer modes of payment. Why so?

Moving to the global data releases, the Bureau of Labour Statistics in the US released the advance estimate of US GDP for Q3 2023. Real GDP grew by 4.9% QoQ SAAR in the third quarter up from 2.1% growth in the preceding quarter. More importantly, this is the fastest growth in the last seven quarters. Talk of a recession! This strong GDP growth is largely due to the strength in domestic consumption followed by domestic investments. This will once again bring into play the ‘one last rate hike’ from the Fed.

Meanwhile, the ECB took a pause. It kept its key policy rates unchanged this week. The pause comes after 10 consecutive rate hikes beginning July last year that have seen the rate on the main refinancing facility increase from 0% to 4.5% currently. Euro area inflation (4.3% in September) while having fallen remains well above the ECB’s target of 2%.

And while we are talking of inflation at 4% being higher than comfort, Turkey this week saw CPI for September print at 62% YoY which prompted its central bank to raise the policy rate by 5ppt to 35%! And despite nominal interest rates being at 35% they are still negative in real terms and by some margin!

That’s it for this week. Did the South Africans finally shrug off their chokers tag yesterday or is it too soon to say? And the Men in Blue take on England tomorrow. Here’s hoping Bazbball is finally laid to RIP…