Underperforming exports, negative FDI, easing WPI and more...

This Week In Data #2

Welcome to the latest issue from This Week In Data. This week, we take a look at;

Underperforming Indian exports

November FDI inflows

WPI inflation and more…

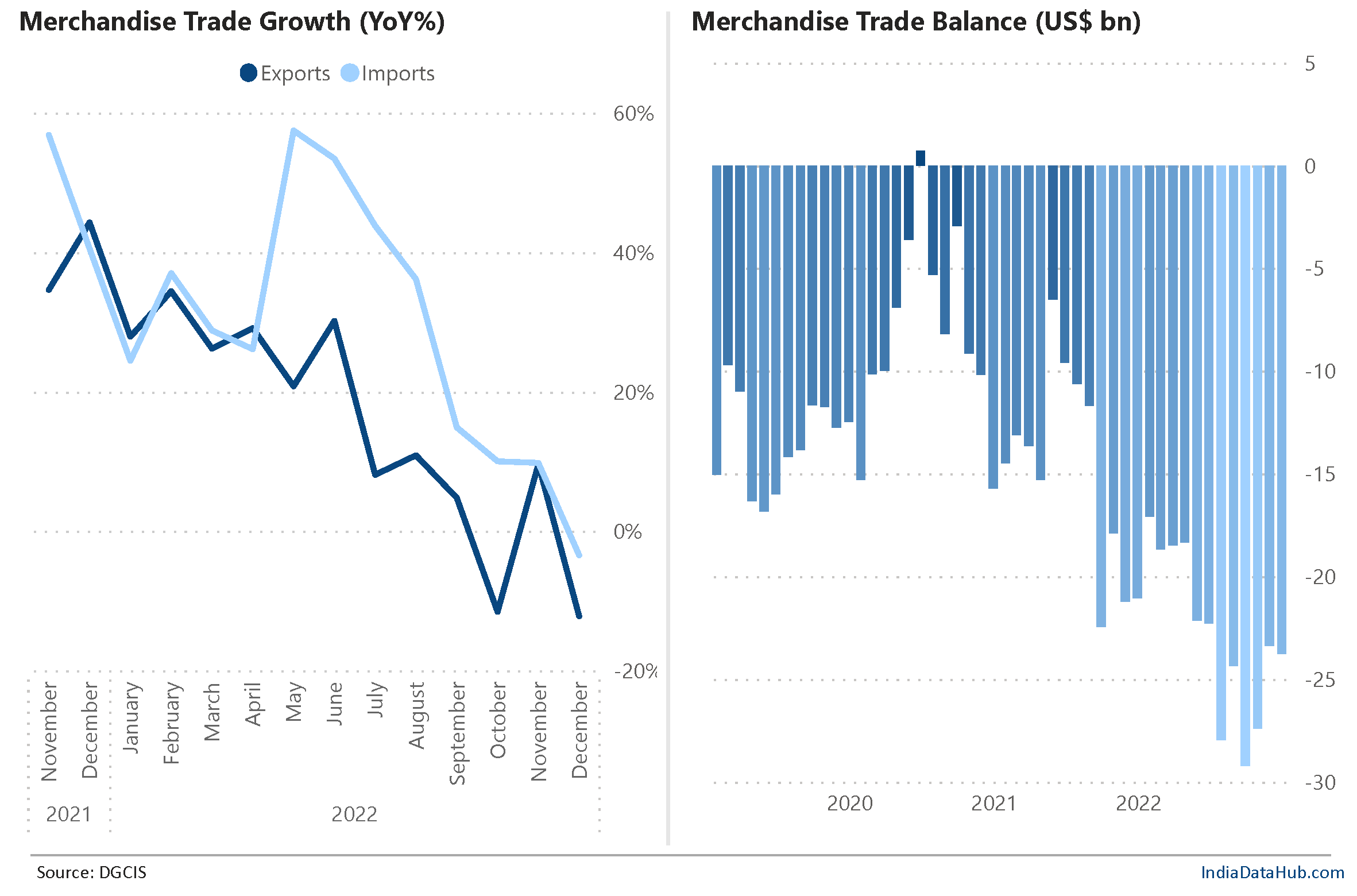

The trade data was released earlier in the week, and it is not positive. India’s exports declined 12% YoY in December. This is the second month in the last three that exports have declined on a YoY basis. The decline is broad-based with 20 of the 30 categories (for which preliminary data is available) seeing a decline in December. And as we discussed here, India’s exports are now underperforming other large countries. The decline in India’s exports is not a part of a global trend of declining exports.

The good news though is that import growth has also moderated sharply in recent months. In December, imports declined on a YoY basis, the first decline since the early days of the pandemic. And consequently, the trade deficit is now moderating. In December, the trade deficit was just under US$24bn, down from a peak of US$28bn in August. This decline is taking some of the pressure off the rupee which has now stabilised at ~81-82 against the USD.

On the topic of the rupee, the RBI released the effective exchange rate data for December. The 40-country Real Effective Exchange Rate (REER) declined by 3% MoM in December and is now the lowest since early 2019. What this means is that while against the USD the rupee has stabilised, against a basket of 40 of India’s trading partners and adjusting for inflation the rupee has depreciated to its lowest in almost 4 years. This should, in theory, make India’s exports more competitive and imports from other countries less competitive. That said, the REER is still above the long-term average and thus it is not the case that the rupee has become overly cheap.

We mentioned in this newsletter last month that after two strong years, the inflow of FDI (Foreign Direct Investments) into India has slowed down during the current year. And data for November released this week has further confirmed this trend. Net FDI in November was negative, implying that the repatriation of FDI from India was higher than the fresh inflow of FDI into the country. This is the first time this has happened in over a decade. And consequently, cumulative FDI in India during the current financial year (till November) is down 25% compared to the same period last year. We will delve into the sectoral trends, once detailed data is available. Stay tuned.

Lastly, we got the CPI (Consumer Price Inflation) data last week. And this week we got the WPI (Wholesale Price Inflation) data. WPI approximates the cost pressures being faced by businesses. And with the fall in global commodity prices, WPI inflation has moderated sharply. In December WPI inflation printed 5% YoY, the lowest since February 2021. And the manufacturing component of WPI saw inflation at just 3.4% YoY and this is the lowest since November 2020. The input cost pressures being faced by domestic businesses are waning. If businesses continue to now raise prices, it will suggest they are doing so because they are enjoying pricing power - a reflection of strong demand. We shall see…

That’s it for this week. Next week will be very light on data. But we shall use that to preview what is certainly one of the most hyped event of the year – the Union Budget.

For more, check out IndiaDataHub and follow @IndiaDataHub on Twitter.