Weak Auto sales, Leap year distortion, Current account surplus and more

This Week In Data #56

In this edition of This Week In Data we discuss:

Review of high frequency data for February

Distortion in YoY data due to leap year

Strong growth in services trade surplus

Mutual Fund inflows

US Employment data

ECB on Pause

A bunch of high-frequency data for Feb has been released. But before we begin to discuss them, we must note that February this year is a leap year so there are 29 days whereas last year it had only 28 days. So that extra day will impact YoY growth of most metrics and it will overstate growth by up to ~3ppt. We will never know the precise overstatement because we will never know whether, for instance, people who bought cars on 29th February would have bought them on 28th February or 1st March if February this year was not a leap year.

This is best manifested in Power generation where one can argue that the extra would flow through a pro-rata extra demand for power. So, power generation in February grew 7.8% YoY, 2.2ppt higher than in January. So adjusted for the leap year the growth rate was unchanged from January. The other area where this manifests itself is Diesel consumption which grew 6.3% YoY in February, almost 3ppt higher than in January. So once again adjusted for the leap year, the growth rate was largely unchanged from January. But petrol consumption was softer in February relative to January even before any adjustment for the leap year.

But when it comes to some of the consumption indicators, things were not that stable in February. Auto sales grew in the low double-digits in February, and this was only modestly slower than the growth in January. But adjusted for the extra day in February, growth in both 2W and Car sales, one can argue was in single digits and 5-6ppt slower than in January. Similarly, port traffic (cargo traffic at the major ports grew just 2.4% YoY in Feb) one can argue would have been flat at best in February but for the extra day.

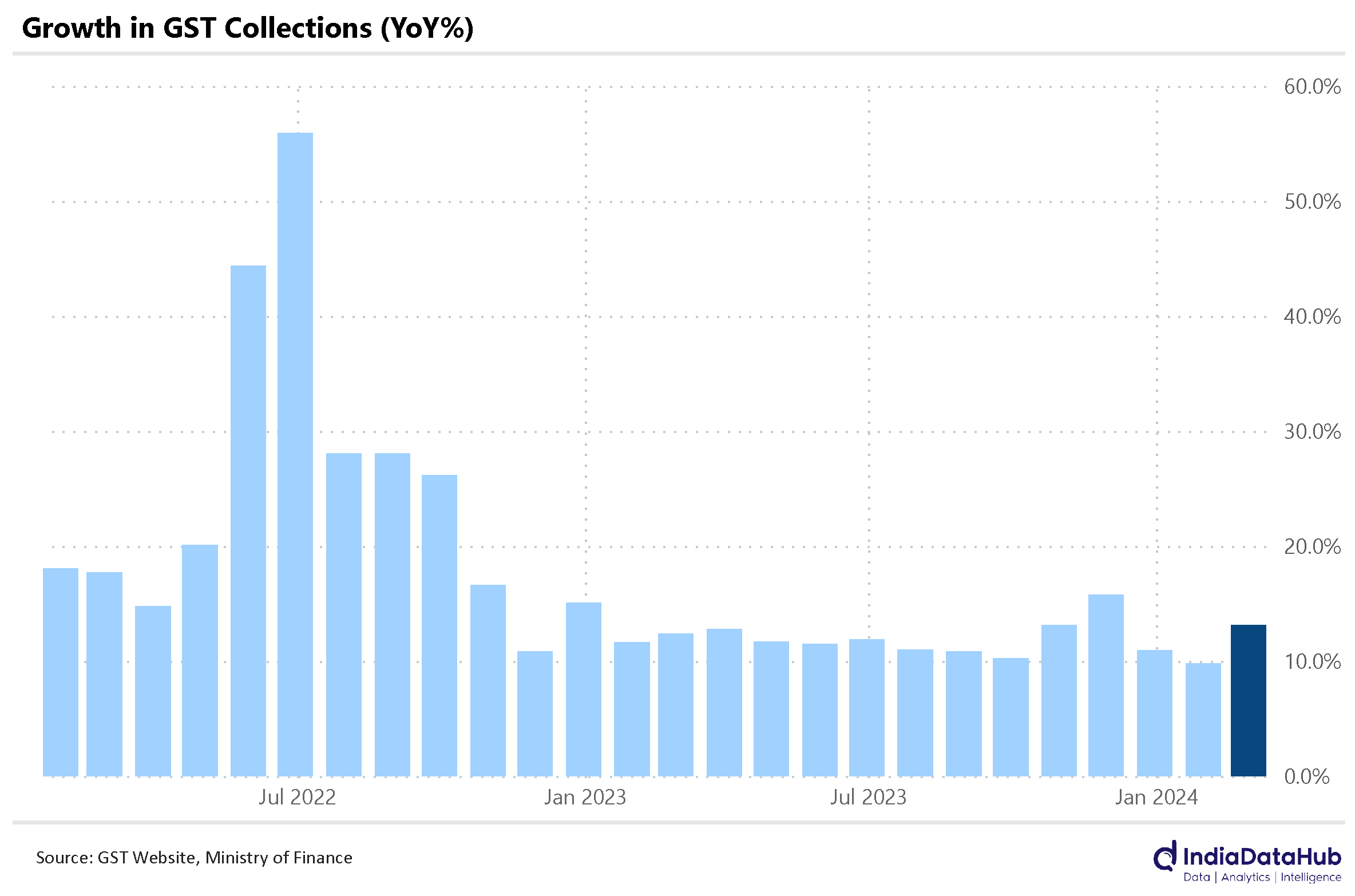

GST Collections grew 13% YoY in February, 4ppt faster than the growth in January. This would prima facie suggest that, given the extra day in Feb, the uptick in growth was only modest. However, the GST Collections in February pertain to economic activity in January and thus are not impacted by the leap year. So the uptick in GST Collections is a clean underlying uptick and the impact of the leap year will be seen in the current month’s data that will be released in early April.

Services exports grew by 11% YoY in January while Imports grew by just 0.2%. Consequently, the services trade surplus grew by over 20% YoY to a record high of over US$16bn.

India’s trade deficit on the goods account was also approximately the same in January which meant that India had close to zero trade deficit. This coupled with the Remittance inflows (which are not included in Services) and adjusted for outflows due to external debt servicing, meant that India most likely had a current account surplus in January! Not something that happens regularly. The strength of the rupee is in large part due to this favourable trade situation.

Mutual funds. And the flows continue to remain robust. Overall, the industry saw net inflows of just under ₹1200bn, the third highest monthly inflows in the last 4 years, the highest being just the preceding month (January). So two months of robust inflows for the industry. And almost all categories saw inflows. Equity funds saw inflows of ₹267bn in February, the highest in almost 2 years. Hybrid funds also saw strong inflows as did Debt and Passive funds. Indeed, over the past three months, Debt funds have seen stronger inflows than Equity funds.

Within equity funds, inflows into small cap funds moderated to a 5-month low of ₹22bn or less than 10% of net inflows into equities. Sectoral or Thematic funds were the star in Feb. Over 40% of the net inflows into Equity funds were into thematic or sectoral funds.

The momentum in SIPs remains strong and that is what is generally discussed. But more interesting is the growth in folios. For the second consecutive month, the industry added more than 4.5 million folios on a net basis. Over the past 12 months, the industry has added almost 30 million folios – that’s almost 3% of the adult Indian population.

Globally, this week the Bureau of Labour Statistics (BLS) in the US released data on payrolls and unemployment. The Non-Farm Payrolls (NFP) increased by 275K in February, up from 229K in the previous month and 75k higher than market expectation. More importantly, though the NFP growth for the previous two months was revised down by a total of 167k. On balance thus, the upside surprise in Feb was either fully or more than fully offset by the downward revisions to the previous two months. The unemployment rate also increased by 20 basis points from the previous month to 3.9% in February.

Lastly, the European Central Bank (ECB) decided to maintain its interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility unchanged at 4.50%, 4.75% and 4.00% respectively. So the pause continues.

That’s it for this week. See you next week!