Declining corp taxes, Small savings, Bank spreads and more...

This Week In Data #69

In this edition of This Week In Data, we discuss:

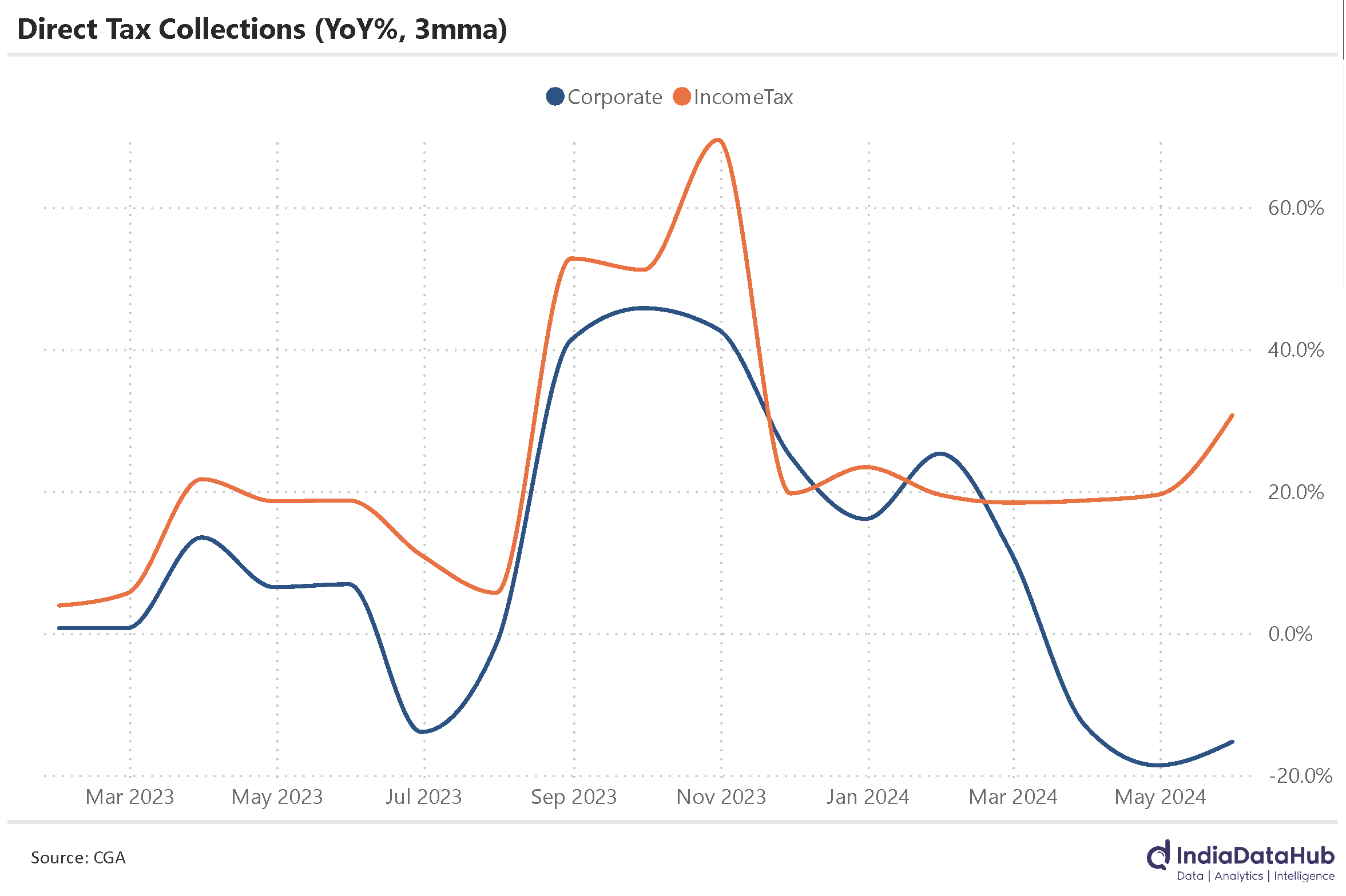

4th consecutive month of decline in corporate tax collections even as personal tax collections remain robust

Sharp decline in small savings collections during Apr-May and implications on liquidity

Bank spreads continue to narrow as credit growth continues to outpace deposit growth

Current account back into surplus, but only temporarily

We had discussed last month that corporate tax collections had declined for 3 consecutive months (Feb – Apr). The data for May was released yesterday and May also saw a decline. And a very sharp one at that – almost 50% YoY. Over the past three months, corporate tax collections have declined by 15%, the first time they have declined in 3 years.

On the flipside though, personal income tax collections have continued to see strong growth. In May, they almost doubled YoY and over the past three months, they have grown by 30% YoY. There is thus a large divergence between the two and this extent of divergence was last seen just before the pandemic (early 2020) and that was when the economy was seeing a sharp slowdown in growth. But that does not seem to be the case now. So what’s happening?

The first instalment of advance tax for FY25 was due earlier this month and that is when businesses (especially corporates) are expected to estimate their full-year tax liability and pay a percentage of that. June accounts for 11% of total corporate taxes during the year, more than April and May put together. So, June data will give us a fair idea of what corporates are currently expecting and what that might mean for corporate profitability and the broader economy.

We wrote about how small savings collections have become large and how they are important from an overall liquidity and fiscal standpoint. However, the first two months have started on a very weak note. Net Small Savings inflows declined 20% YoY in April and in May they declined by 40% YoY.

For reference, the net market borrowings of the Centre and States combined in FY24 was just over ₹18,000bn. The net mobilisation under small savings was just over ₹4,200bn or more than 20% of the government borrowings. So, a sharp decline in inflows under small savings will, ipso facto, result in higher government borrowings, which will impact money market liquidity and interest rates.

Speaking of liquidity and interest rates, the fight for deposits among banks and the bigger fight for savings between banks and capital markets has meant that deposit rates continue to increase even as lending rates have remained stable. In the last two months (Apr-May) the weighted average interest rate on all term deposits of banks has crossed 6.9%, the highest of this tightening cycle. Interest rate on all loans has however remained stable at 9.8% since the middle of last year. Consequently, the spread (interest rate on loans minus interest rate on term deposits) has declined to 2.9% as of May, down 50bps on a YoY basis and 10bps since the start of the year.

The loan-deposit ratio for banks has only increased in recent weeks as the gap between credit growth and deposit growth has also widened in the last couple of fortnights. And capital markets continue to remain buoyant and thus attract household savings. So, there does not appear to be any respite for Banks on the horizon, unless the RBI changes its stance on liquidity and rates.

Lastly, India’s current account turned into a surplus during the March quarter. This was broadly expected given the partial data that was already available. The reason this is still significant is because this is the first surplus since 2007 (excluding the pandemic period). And because capital flows remained strong, India had a BoP surplus of over 3% of GDP during the quarter. This again is one of the highest in recent years. Both of these are markers of very strong external account fundamentals.

The current account surplus was almost entirely due to a sharp decline in the trade deficit. So far in 1QFY25, the trade deficit is running modestly higher on a YoY basis and thus the current account is likely to return to a modest deficit (~1% of GDP) during the current quarter. So, the status quo ante will be restored as far as India’s external account is concerned.

That’s it for this week. The Bharat Army takes on the Proteas today. Time to make up for last year’s miss, although the team is different. Sadda haq, ithe rakh…

Insightful