In this edition of This Week In Data, we discuss:

FDI Inflows into India are very low, but this has been the case for 3 years

FDI is being dragged not so much by lower inflows but higher repatriation and outward FDI

Retail fuel prices have increased ~4% in last few days, modestly pushing up CPI

While FX reserves have fallen, they remain fairly close to long-term average

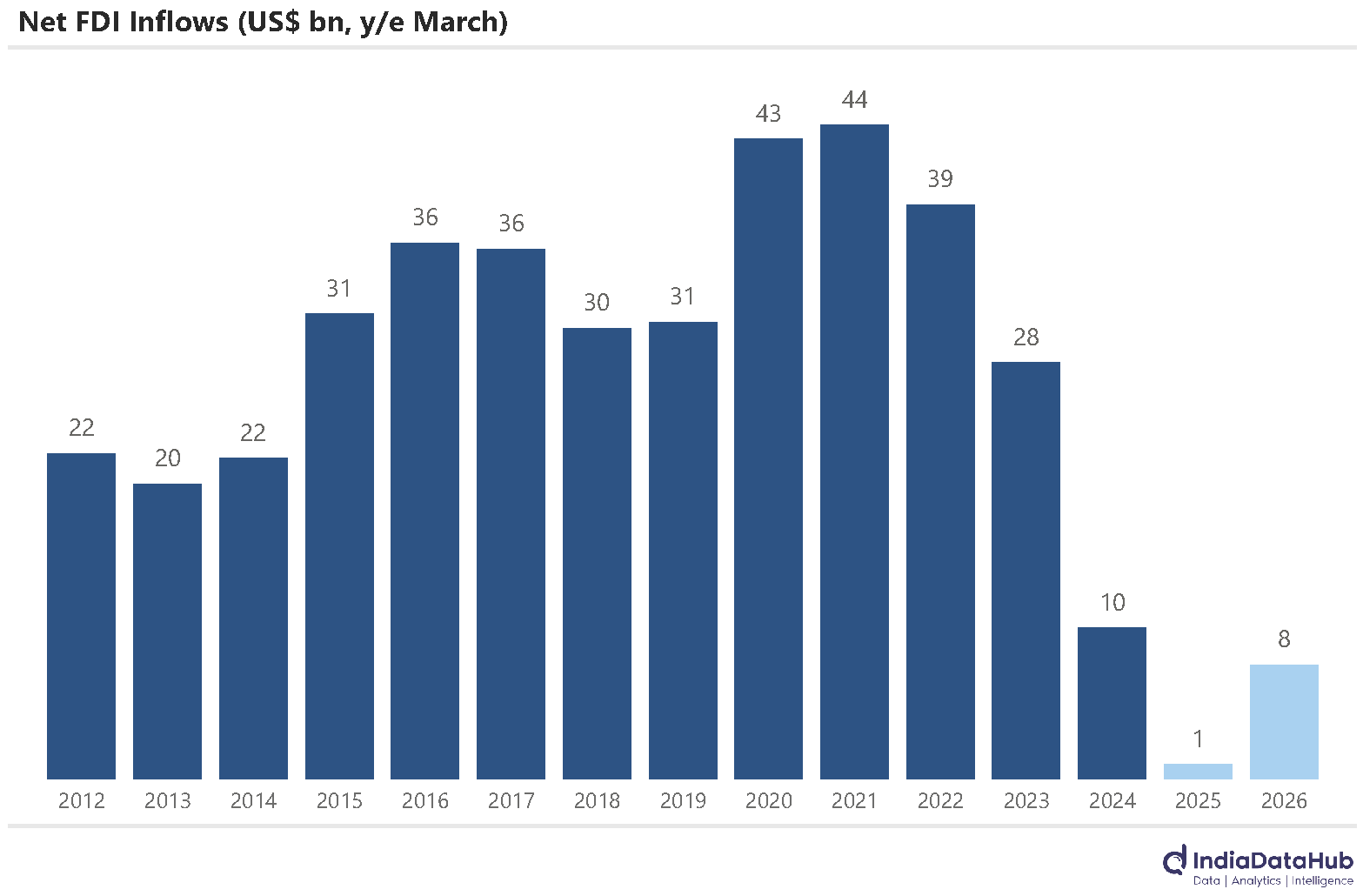

Let us start with FDI. There has been a lot of discussion about how FDI in India has fallen, and the absence of this buffer against FPI outflows is a key contributor to the rupee’s sharp depreciation. This is largely a fair argument. In FY26, for instance, the net FDI inflow was a modest US$8bn. That’s just 0.2% of GDP. Five years back, in FY21 – the peak year for FDI, the net FDI was US$44bn. A decline of 80%!

But this is not a new development. Regular readers of this newsletter would recall multiple occasions over the past couple of years. Indeed, one of the earliest comments on weak FDI that we had made was way back in June 2023, almost 3 years ago. The reason we need to bring this up is not to self-gloat, but because we are now discussing weak FDI when FDI has started to recover.

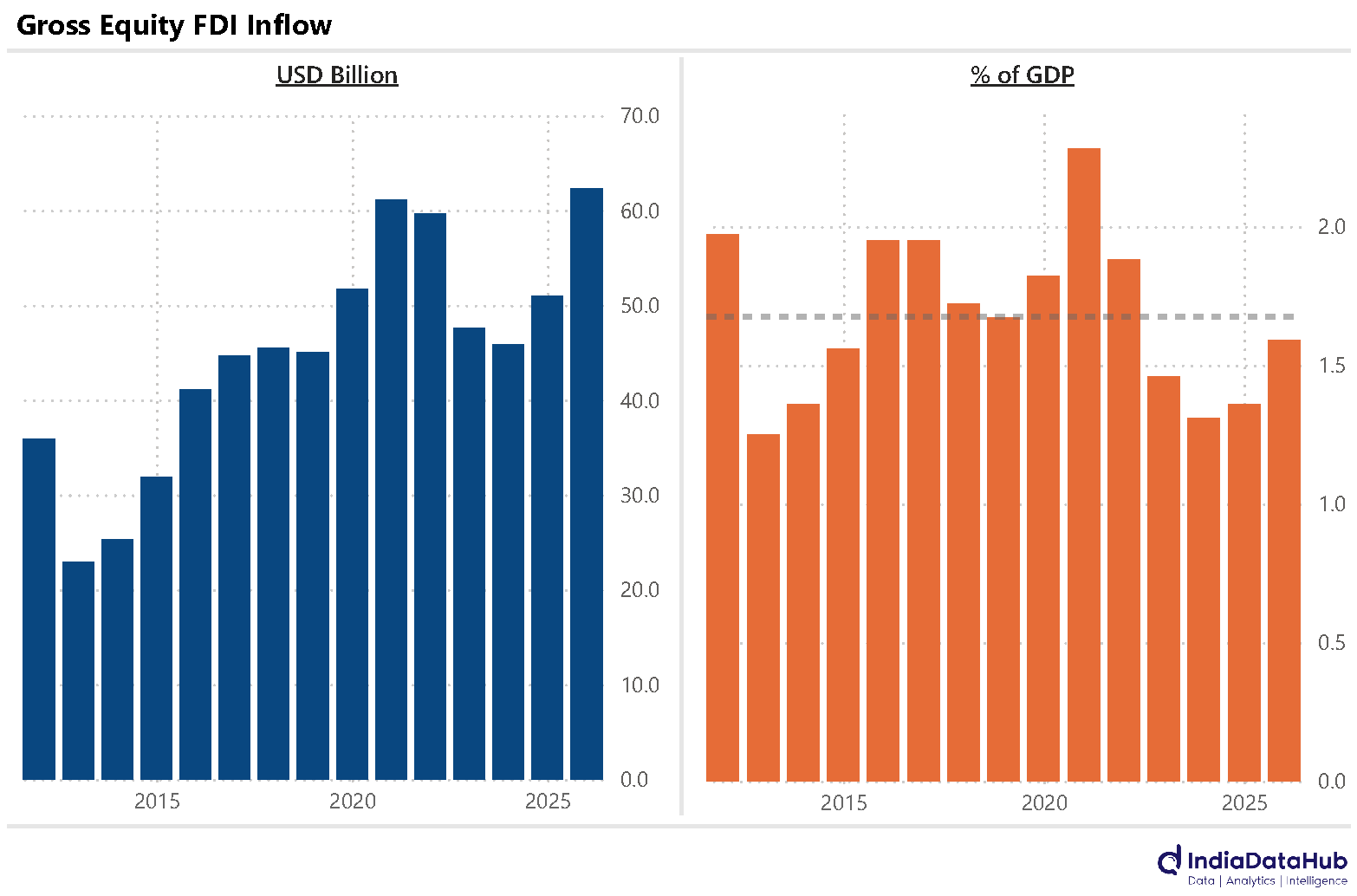

FDI inflows rose in FY25 after a few years of decline. And in FY26, the financial year that just ended, they rose over 20% and reached the highest ever. In FY26, the actual inflow of FDI into India (without counting reinvested earnings, which is a contra entry) was US$62bn – a 33% jump in 2 years and higher than the FY21 peak of US$61bn. Over the past 15 years, the FDI equity inflows, relative to GDP, averaged 1.7% of GDP. And in FY26, it totalled 1.6% of GDP. Only a shade lower. Of course, there were years when FDI was substantially higher than this (most notably FY21 – the year that saw the large capital raising by Jio Platforms). But equally, there were years when FDI was lower than this.

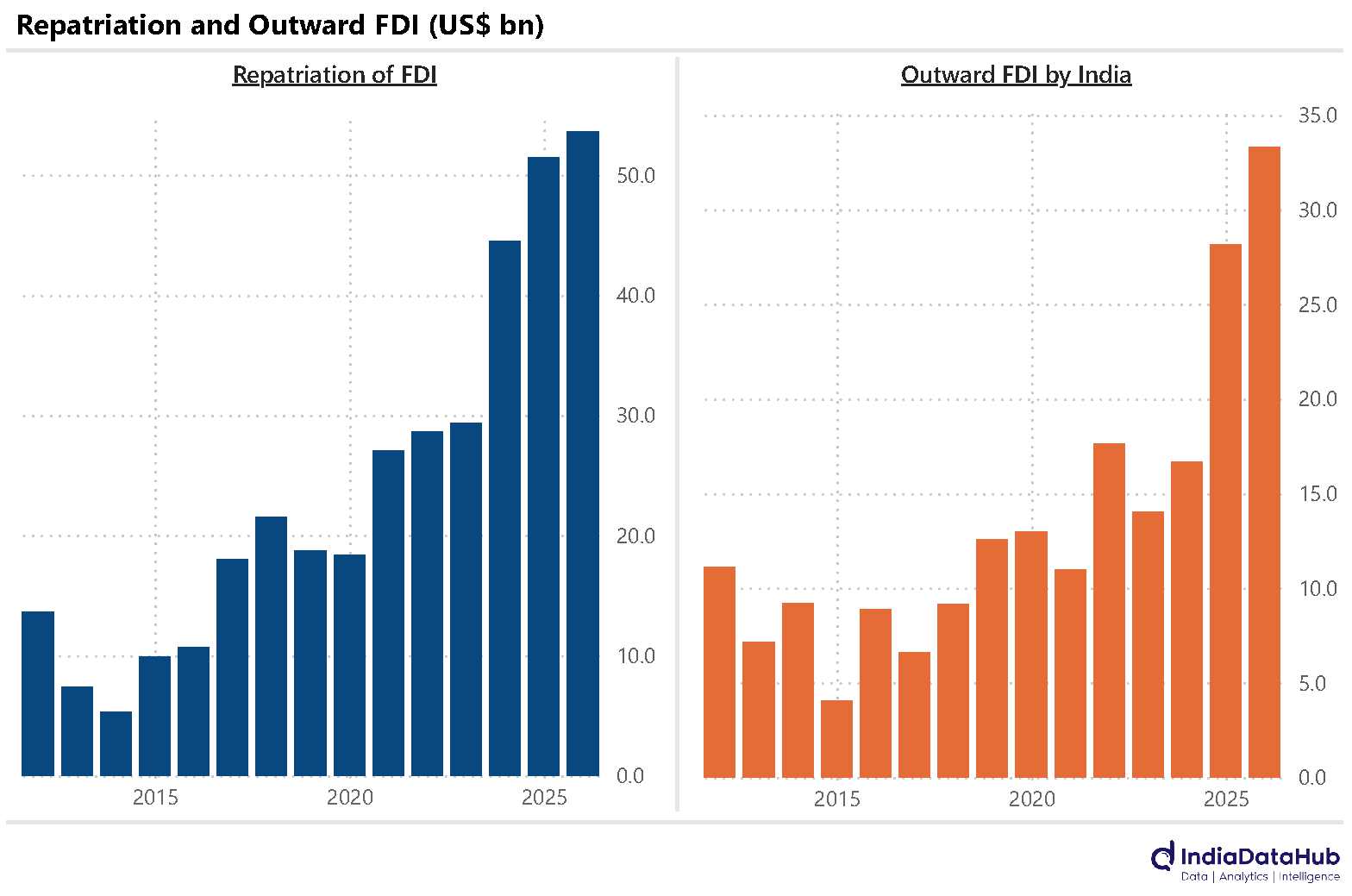

The real problem in the last few years, and one that has persisted through FY26, has been outflows of FDI – both repatriation of existing FDI and outward FDI by Indian businesses. FY26 saw over US$50bn of FDI being repatriated out of India. This was on top of US$50bn of FDI being repatriated in FY25. In the last 5 years, repatriation of FDI has doubled and now accounts for almost 85% of equity FDI that we receive.

Some of this was the large IPOs with an outsized OFS component, with global corporations listing their subsidiaries as well as VC and PE firms exiting through IPOs. But repatriation is slowing down. In FY26, repatriation grew by less than 5%. But what is now hurting is outward FDI by Indian corporates. Outward FDI by Indians increased almost 20% in FY26, reaching US$33bn and is now over half of the actual equity FDI received. And in the last 5 years, outward FDI has more than tripled. Indian corporates investing billions overseas. Now that is something that is not part of the discourse so far.

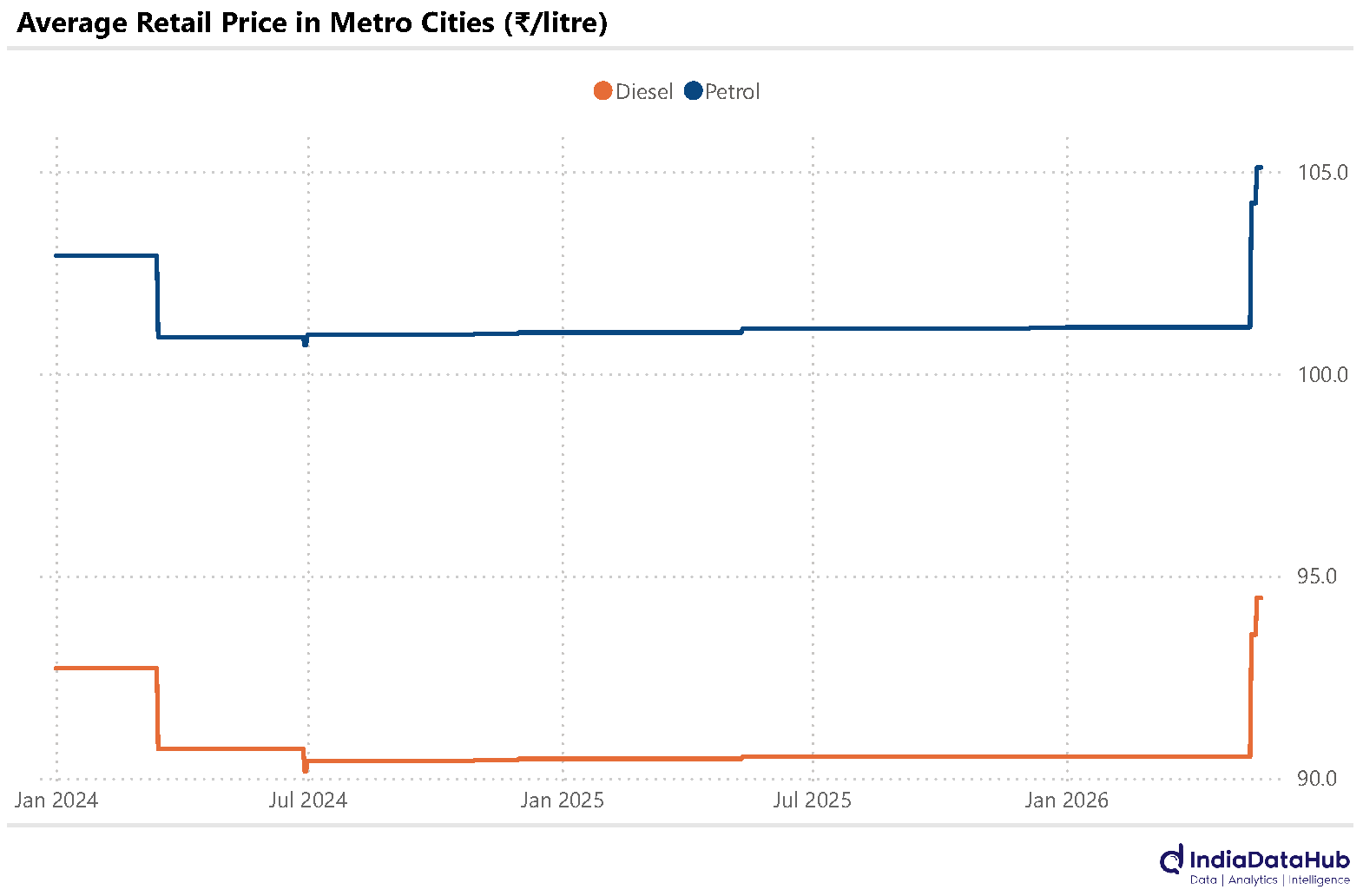

Retail fuel prices have finally seen an increase in the last couple of weeks. The price of both petrol and diesel has increased by ~4%, which is still an incomplete pass-through of higher international crude oil prices. The direct impact of this increase on CPI inflation will be modest. Petrol and Diesel together have a ~5% weight in the new CPI, and a ~4% increase in prices implies a roughly 20bps increase in headline CPI inflation.

However, as we mentioned last week, the longer Oil prices stay elevated, the more the domestic pass-through, not just for retail fuels but also for industrial fuels, petrochemicals and other petroleum-derived products. Last month’s WPI increase is an important pointer towards it. So as we approach the next monetary policy meeting in early June, the environment before the MPC is dramatically different. While a rate hike is unlikely, if oil prices remain elevated, it will be on the table by the next policy meeting.

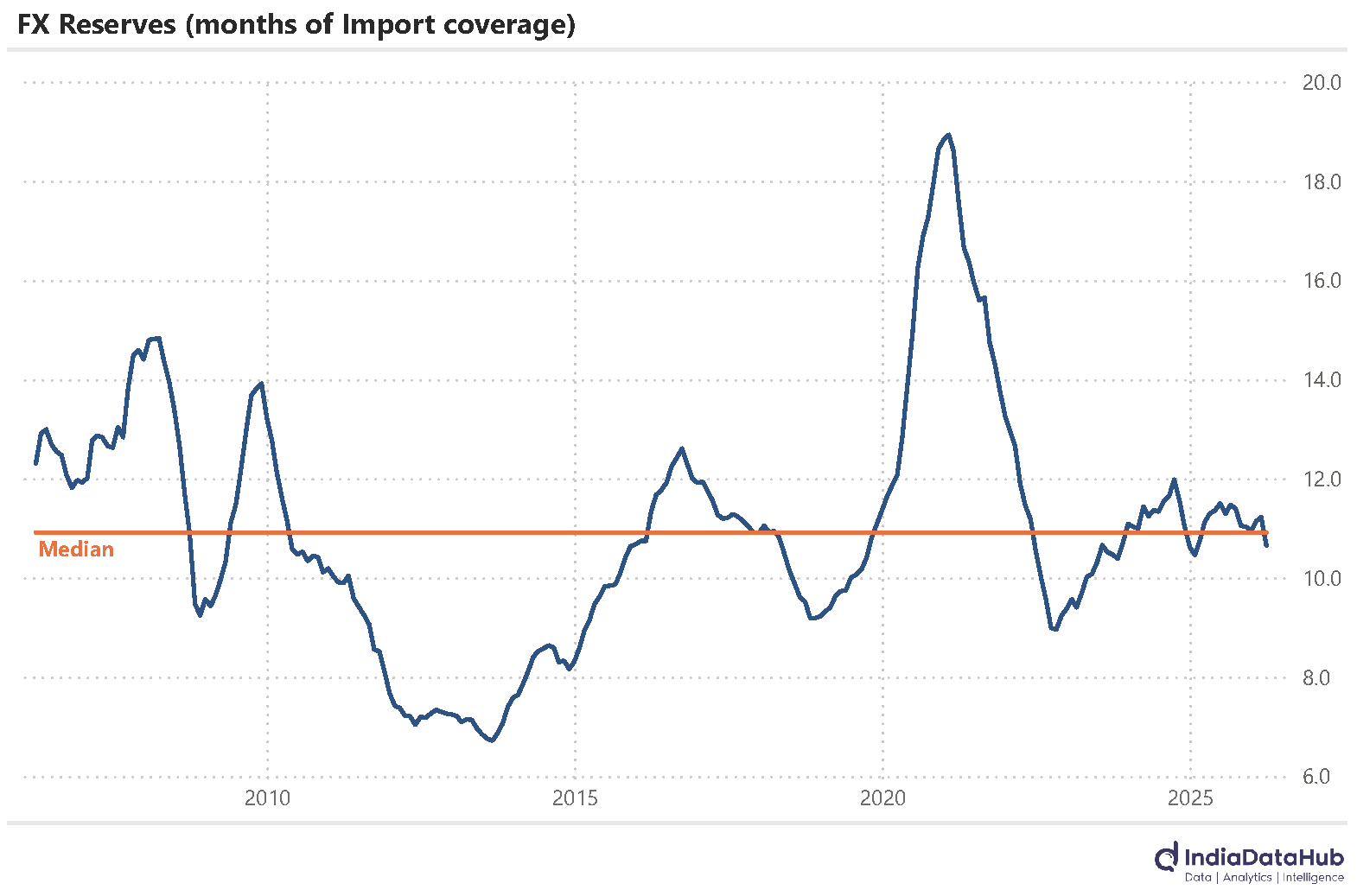

Lastly, FX reserves. They continue to remain just under US$700bn. And while they have fallen due to RBI’s intervention to defend the rupee (and partially offset by the increase in value of gold holdings), they are not low. As of March 2026, for instance, FX reserves totalled just over 10.5 months of imports (on a rolling 12-month basis). This is slightly below the last 20-year average of 11 months. Indeed, back in 2013, during the taper tantrum, when the rupee had seen a very sharp decline, FX reserves were just ~7 months of imports.

That’s it for this week. See you next week…