Monetary Policy, Capex, Services trade, US Payrolls & more...

This Week In Data #38

In this edition of This Week In Data we cover:

RBI’s decision to rates unchanged

Outlook for manufacturing capex

Strong growth in Services trade surplus

Recovery in petroleum consumption

Moderation in power generation

Strong US non-farm payrolls

US Interest rates

In case you missed we announced the upcoming release of the third in our Data Book series of books titled 'India: The Global Context,' set to launch in December. In this publication, we will delve into the global landscape and contextualize India’s position in the world – its neighbors, other emerging economies as well as the large, developed countries – across a host of indicators, ranging from the Economy to Demographics, from Energy to Infrastructure, from Agriculture to Foreign Trade. Also, next week we will release the second version of our cross-platform Excel plugin that will allow users to download India, State, District and Global data directly into their spreadsheet. And later this year you will also be able to download mutual fund data - AUM trends, daily NAVs and monthly portfolios - using the add-in. Stay tuned for both…So monetary policy. And as expected, the hawkish pause continues. The MPC kept the policy repo rate unchanged at 6.5%. It has remained unchanged since the February policy meeting. The monetary policy was expected to be in a sense, a non-event, and it turned out to be so.

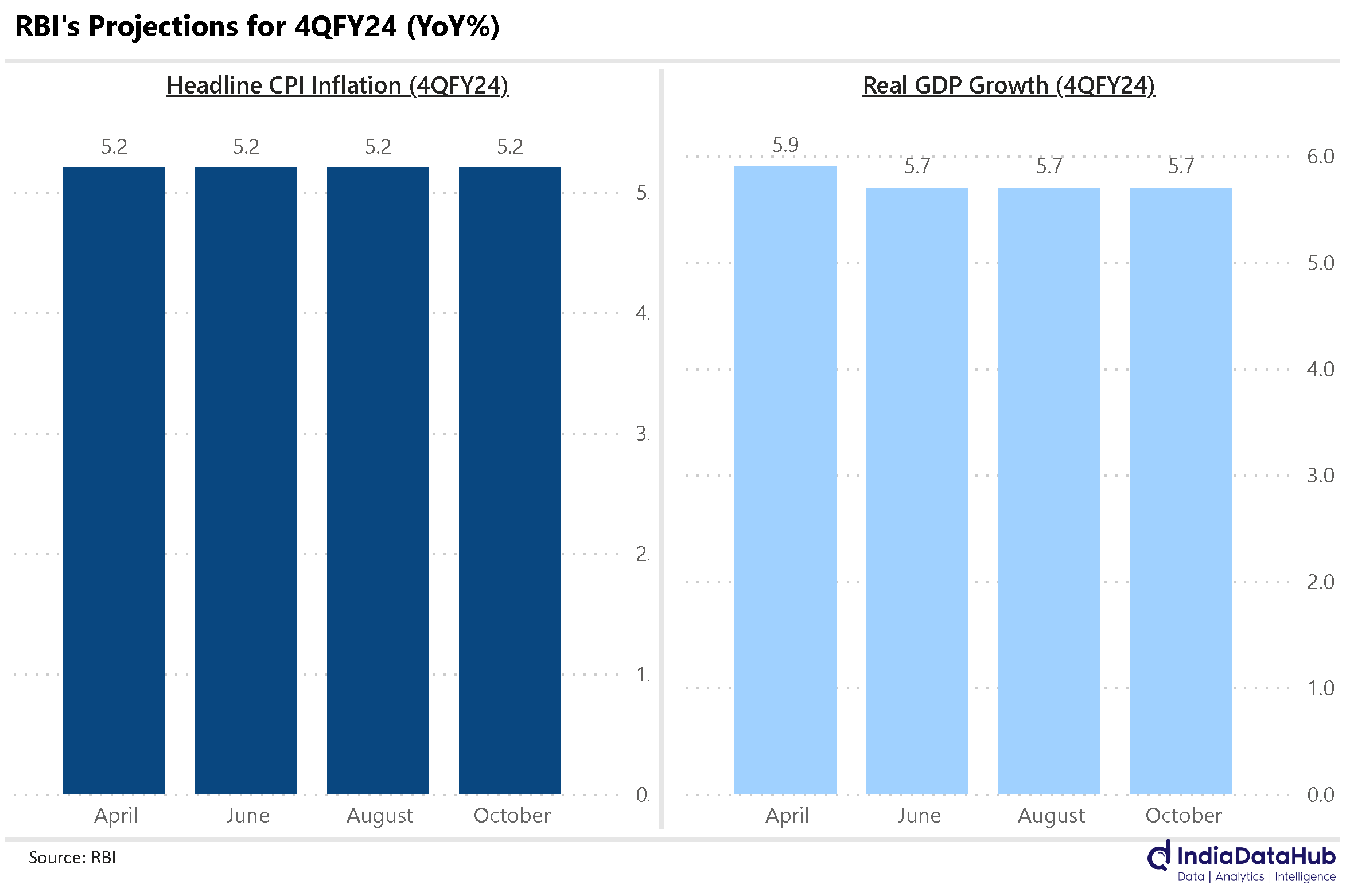

As it did the last time around, the MPC is looking through the spike in headline inflation driven by Vegetables. And like it did in August, it expects this spike to be temporary. Its inflation projection for the March quarter remains unchanged at 5.2% since the April policy. Its GDP growth estimate for the March quarter has also remained unchanged at 5.7% YoY since the June policy. Effectively, amid the ebb and flow of data, the big picture has not changed much in the last couple of quarters in the MPC’s assessment.

We have discussed how the expectations of a rate cut from the Fed have been progressively pushed out as growth has remained resilient in the face of this massive monetary tightening and inflation hasn’t exactly become benign. This story is playing out in India too. Back in June, the consensus estimate was for the first rate cut in February of next year. In August this got pushed out to April and as of today, the first rate cut is expected in the June MPC meeting.

And when it comes to expecting a rate cut, here’s some food for thought. The RBI is currently estimating that CPI inflation will average 5.2% during the June quarter next year. This would mean that over the past 5 years (ending June 2024), headline CPI inflation would have averaged 5.8%. The target set for the MPC is 4%. So, the timing of the rate cut is not just about whether inflation moderates from the current close to 7% but it will be determined by when it starts to align towards the 4% target. If growth remains resilient, as is the consensus expectation, then unless the CPI trajectory trends towards 4%, the RBI could remain on the sidelines through most of 2024 as well.

There is a lot of optimism around capex in the economy currently. And not all of it is supported by data. As per data released by the RBI on Friday, overall capacity utilization in the manufacturing sector rose to 74% during the June quarter, 1.5ppt higher on a YoY basis. Over the past 4 quarters, it has averaged 74.5%, the highest in the last 4 years. More importantly, capacity utilization is still below the long-term average (2009 – 2019) excluding the pandemic period – the pandemic period pulls down the average quite significantly.

Similarly, in the Manufacturing survey conducted by the RBI, over 40% of the respondents said that their current capacity is more than adequate to meet the next two-quarters demand. This is the highest outside the pandemic period. Just 3% of the respondents said that their capacity was inadequate. So, manufacturing firms are not saying that they anticipate any immediate capacity constraints. Of course, capex by existing manufacturing firms is just one part of the story. There is scope for new firms to be setting up capacity, data for which such surveys cannot capture. And of course, there is services capex. So, there are other moving parts to capex.

India’s services exports rose 8% YoY in August while imports declined 1% as per the provisional data released this week. Services imports have been weak for a few months now – they have declined on a YoY basis in 4 of the preceding 5 months. Consequently, the services trade surplus has been growing in double-digit terms in the last few months. Indeed it has grown by 20% YoY in the last 2 months.

As a consequence, India’s total trade deficit (goods + services) has fallen by over a third in the past three months. This is also one of the factors that is supporting the rupee.

Petroleum consumption picked up in September, the second consecutive month of strong growth. The uptick in September was due to strong growth in Petrol consumption (8% YoY) even as Diesel consumption was subdued (4% YoY). Bitumen consumption has been seeing strong growth in the past three months (average growth over 50% YoY). Given its primary use for road construction, it seems the authorities have used the opportunity provided by the weaker monsoon to step up road construction.

Power generation decelerated in September as expected but still grew by a strong 9% YoY as per the provisional data released this week. As we have discussed before, the uptick in the last two months is likely a reflection of erratic monsoon which drives up both residential and agricultural demand. So not something we will extrapolate to subsequent months. Irrespective of the driver, higher power generation will flow through to higher industrial production and will in turn drive higher GDP growth.

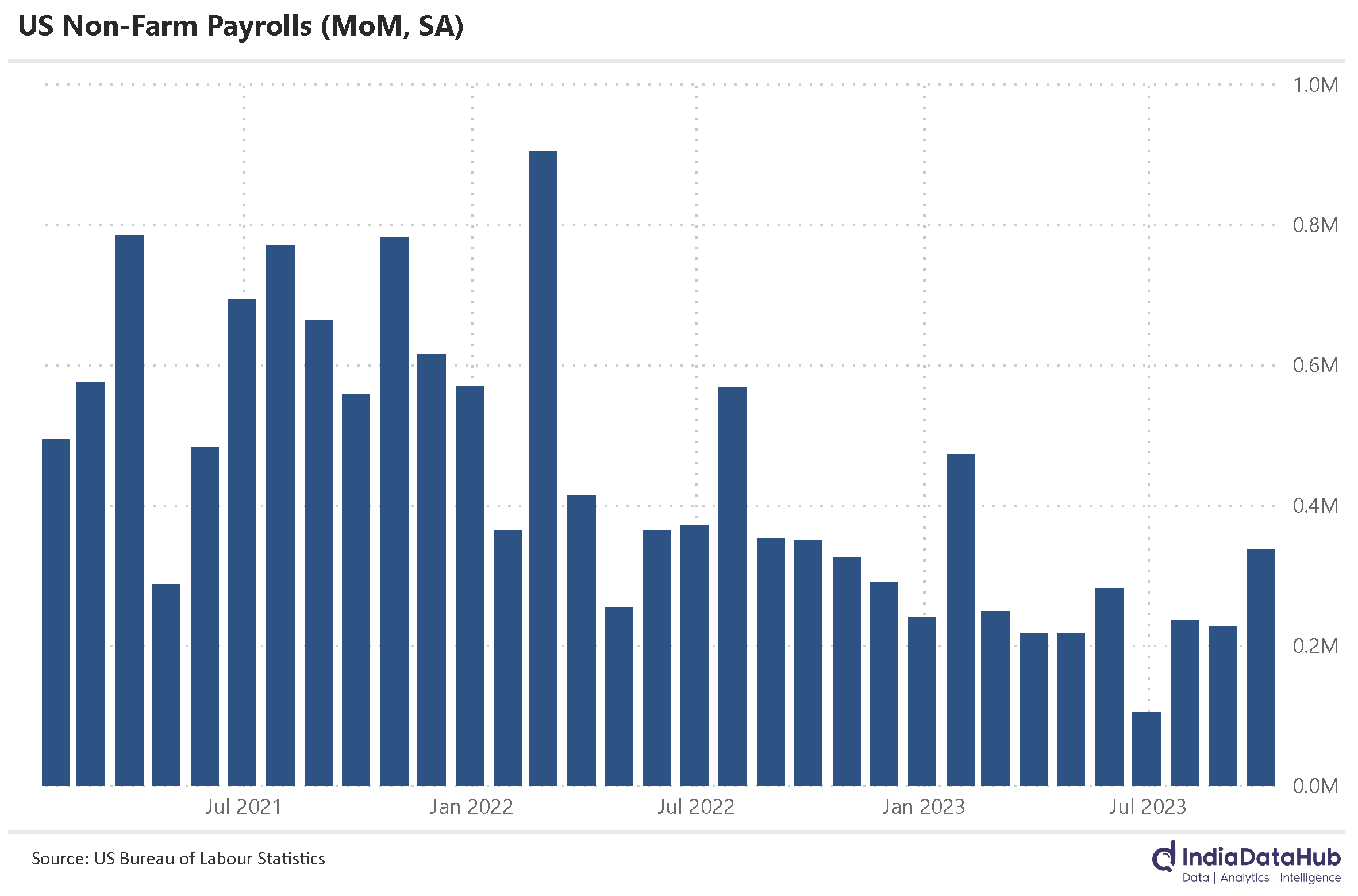

Finally, the US (it isn't over without either the US or China, no?). We got the non-farm payroll data and it was an unusually strong number. The US economy added 336k jobs in September, this is almost 2x the market expectation. More importantly, this is the highest payroll number since January. Furthermore, the payroll growth for the prior two months – July and August – was revised upwards by a cumulative of 120k. The unemployment rate remains unchanged at 3.8%, the lowest since March last year. So pretty much a blowout report.

Not surprisingly, treasury yields edged up with the 10yr now yielding 4.8%. And as we wrote in our State of Markets report yesterday, the 3mth US treasuries are now yielding over 3.6%, the closest anything comes to a risk-free asset, is now yielding over 3.6%. This is the highest since 2000 – almost 25 years!

And with that, we call it stumps. India plays Australia tomorrow at the ICC Cricket World Cup. Fingers crossed…